Mortgage Rates Puzzle Is a Worry for Housing and the Fed

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThere’s a puzzle developing in the housing market — mortgage rates have fallen rapidly to their lowest level since early 2023, but would-be homebuyers don’t seem to care. It’s possible this is just a timing issue with rates falling during the slow season for transactions and election jitters giving buyers additional reason to hold off. But the unique path of mortgage rates in recent years raises the possibility of something more ominous at work.

The 30-year mortgage rate was circling 7.5% in the final quarter of last year, making the drop to about 6.1% a welcome sight — but not welcome enough for most buyers. The decline so far may have led many to believe that there’s more to come once the Federal Reserve’s widely expected policy easing begins. This “deflationary” mindset would help explain why transactions have barely picked up.

We have become used to seeing mortgage rates, both for individuals and across households, respond quickly to Fed easing: Looser policy has in the past translated to lower home loan rates for new buyers (fueling transactions) as well as homeowners overall as refinancing lowered monthly payments. This provided a double stimulus to the economy in the early 2000s, after the 2008 financial crisis and during the pandemic. We’re in a very different environment today.

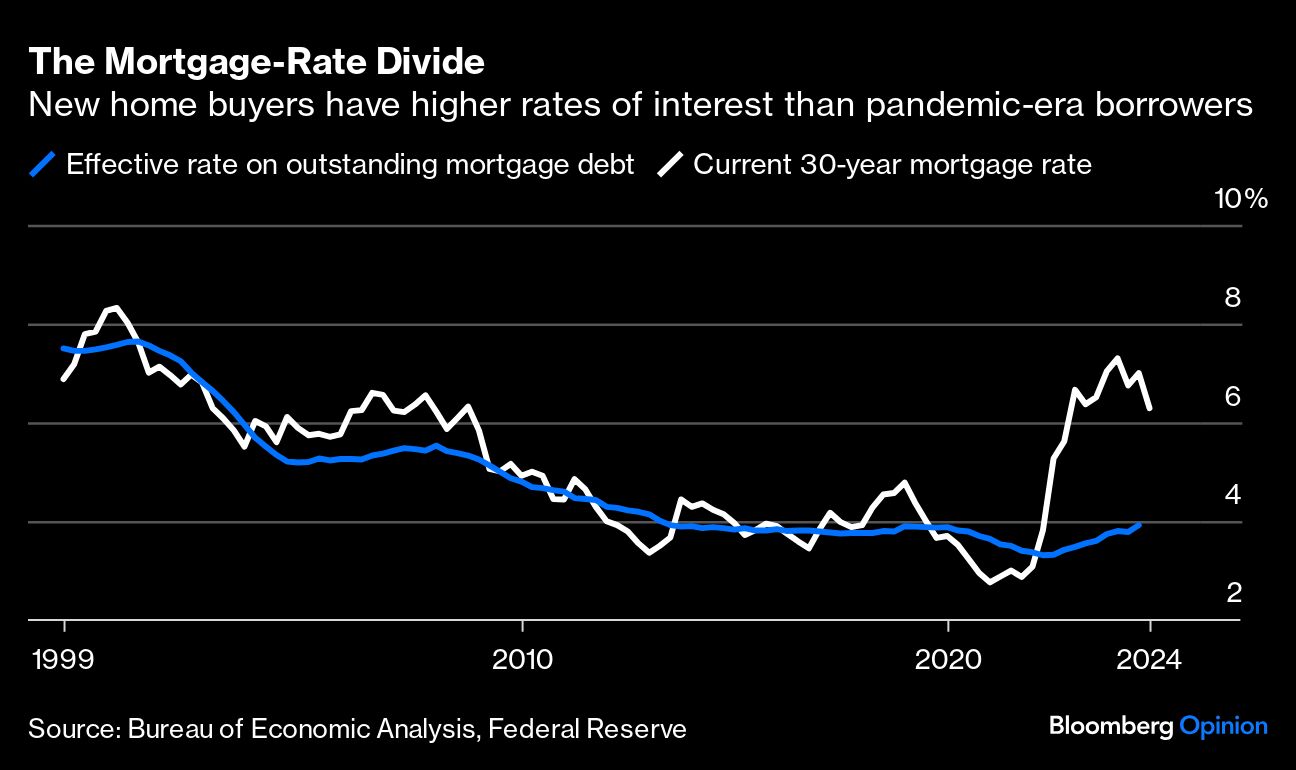

One way of understanding this is by comparing prevailing mortgage rates with those experienced by the sum total of homeowners. Since the first half of 2022, the relationship between borrowing costs for new buyers and the effective mortgage rate for the economy has weakened.

Prevailing mortgage rates more than doubled between the end of 2021 and the end of 2022, from the low 3s to the high 6s, yet the average rate paid across those with a mortgage barely rose at all, going from 3.37% to 3.48%. At most, a couple of million new homebuyers were paying those new nosebleed rates while tens of millions of homeowners still locked into their low pandemic-era rate were unaffected.

Now as the prevailing rate falls in anticipation of Fed rate cuts, the effective rate paid on all mortgages outstanding is actually moving higher. And the pace of that increase should accelerate through next year as new buyers commit to current rates and as existing borrowers continue to pay down their low-rate mortgages and some swap into new houses at higher rates.

There are a few implications to consider here as we think about what Fed easing will mean for housing and the economy in 2025.

First, the deflationary psychology I talked about before with respect to mortgage rates means it is taking longer for would-be homebuyers to respond. Policymakers may find that they need to deliver significant reductions before buyers, especially those seeking to upgrade or downsize, find the math compelling. It’s hard to say what the magic number is — 6%? 5.5%? 5%?

Second, the reality that the effective overall mortgage rate will continue to rise throughout 2025 will restrain how stimulative lower borrowing costs will be. If a homeowner with a 3.50% rate decides that they’re willing to sell their current house and buy a new one at 5.50%, does that boost or negatively affect economic activity since it leaves them with less money to spend on everything else?

The wild card here is the high levels of home equity that existing homeowners can access if they choose to. The amount of equity that Americans have in their homes increased by 80%, or nearly $16 trillion, from the end of 2019 through the second quarter of this year. Swapping into a higher mortgage rate to move homes is expensive, but a lot of incremental consumption may result if that move involves taking tens of thousands of dollars of equity out in the process.

Ultimately, the extent to which rate cuts by the Fed and lower mortgage rates boost the economy will likely come down to how much Americans are willing to tap their equity to keep spending. Balancing that out will be a slowing labor market and interest rate dynamics that act as a drag on household balance sheets as the low fixed-rate debt that Americans took out during the pandemic is replaced by new higher-cost debt — even if prevailing rates are lower than what we experienced over most of 2023 and 2024. If Americans don’t feel confident enough to spend some of that equity, it’s going to take a very aggressive rate-cutting cycle to provide the support that the economy needs.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All