Suddenly Asia Is Place to Be as Stocks, Currencies Outperform

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAsian assets swung violently over the past three months, rocked by a succession of epochal events that culminated in a giant stimulus boost for China and propelled the region’s equities to world beaters.

Having gained momentum, they’re now a focal point for global investors preparing for lower US interest rates and a presidential election likely to further shake up financial markets.

It all points to an extended period of volatility after stock, bond, credit, currency and commodity markets were roiled by Japan’s interest-rate hike, the start of Federal Reserve easing and the unleashing of that long-delayed economic stimulus in China. The final results — healthy gains for most regional equities and foreign exchange, a bounceback in emerging markets, and the torpedoing of the yen carry trade — only tell part of the story.

Stocks

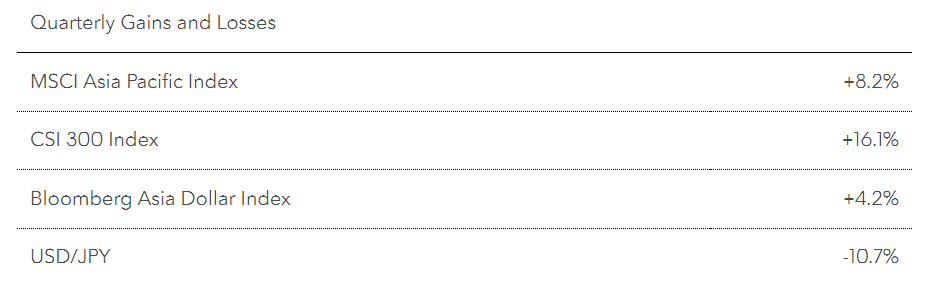

MSCI’s gauge of Asian shares beat both its US and European peers in the same quarter for the first time since 2022. The regional index was powered by a late September surge in equities in China, where the benchmark CSI 300 Index rallied after the authorities announced steps to boost bank lending, lower borrowing costs and ease housing curbs.

The measures from Beijing will compel global investors to rethink light China allocations, said Kevin You, a fund manager at Allianz Global Investors in Hong Kong. “A key issue will be to see an improved outlook for corporate earnings. We expect this will happen over time, especially when headwinds from the property sector start to ease.”

So far, there are few signs that the euphoria from China has spread to other Asian equity markets. Given the region’s close trading links, stocks elsewhere may get a boost once investors are convinced of the effectiveness of the latest stimulus.

The Fed’s decision to start rate cuts with a 50 basis-point move on Sept. 18 helped power a rally in many of the region’s emerging markets. Benchmark gauges in the Philippines and Thailand both gained more than 10% over the quarter.

Japanese Stocks

Not all Asian stock markets prospered.

Japan’s Topix had its first quarterly loss in two years after the Bank of Japan unexpectedly hiked rates in July. The decision saw Japanese share prices plummet by the most since 1987. The rate increase boosted the yen and led to an unwinding of the yen carry trade — where investors had borrowed in the Japanese currency to fund purchases of higher-yielding assets elsewhere.

“Uncertainty about the US economy, the adjustment of tech stocks, and the yen rally happened all at once, triggering the big drop in stocks,” said Masahiro Ichikawa, chief market strategist at Sumitomo Mitsui DS Asset Management in Tokyo. Still, the underlying appeal for Japanese shares remains broadly intact, and would be bolstered further if developed-market central banks tame inflation without causing a recession, he said.

Looking ahead, investors in Japan also face some uncertainty surrounding the likely policies of Shigeru Ishiba, who is set to be confirmed as the nation’s new prime minister on Tuesday.

Bonds and currencies

The yen strengthened against all its Group-of-10 peers over the quarter as it benefited from the narrowing interest-rate differentials between the US and Japan. Strategists see the currency holding onto those gains to end the year around current levels at 142 per dollar.

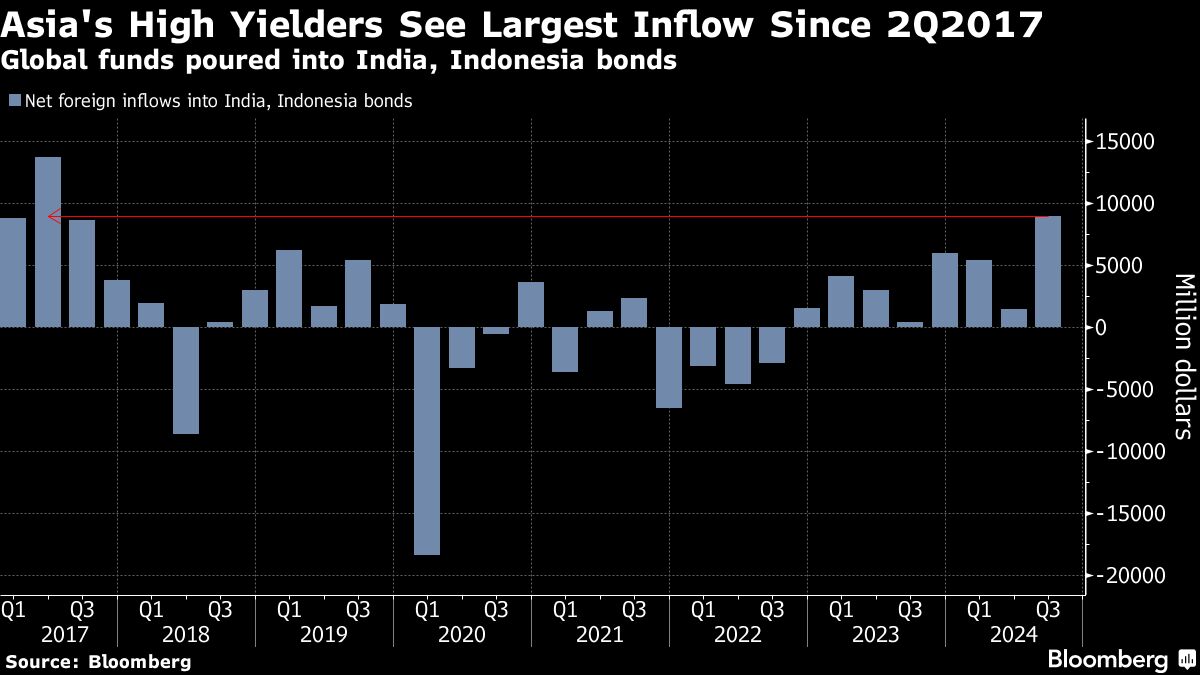

The Fed’s rate cut bolstered higher-yielding bonds. Overseas funds poured around $9 billion into local-currency Indian and Indonesian debt in the quarter. Meanwhile, Malaysia’s ringgit jumped by more than 14%, a record quarterly gain based on data compiled by Bloomberg.

Economies in Asia that are late to the global easing cycle, such as India or South Korea, may offer some of the best relative returns in the near term as their central banks pivot to dovish policy settings, Goldman Sachs Group Inc. strategists including Kamakshya Trivedi and Danny Suwanapruti wrote in a research note last week.

Credit

The start of the Fed’s easing cycle also helped support appetite for Asia’s corporate debt.

“You ease financial conditions further and it should extend the credit cycle,” said Sheldon Chan, a portfolio manager for Asia credit at T. Rowe Price Group in Hong Kong. “That should be constructive for emerging-markets credit spreads and Asia credit spreads.”

Moreover, China’s support measures will help risk assets, including corporate debt, Chan said. “It does underpin Chinese risk assets in the near term,” but “will take time to really convince the market further out.”

Commodities

The stimulus announced by China also had an outsized impact on some commodity markets. Iron ore spiked more than 11% on Sept. 30 alone after three of the nation’s biggest cities eased curbs on home buying, bolstering the outlook for demand. Prior to that, the metal had been one of the year’s worst-performing major commodities.

The prospect of heightened tensions between the US and China if Donald Trump wins the US presidential election in November may add further volatility to the region.

“The most immediate concern on the negative side is going to be the case of a Trump victory, given the report of a likely 60% tariff on all the Chinese goods and its impact on China’s economic growth,” said Frank Benzimra, head of equity strategy at Societe Generale SA in Hong Kong.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All