Four Easy Steps to Build a TIPS Ladder

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits About two years ago, I built my million dollar 30-year TIPS ladder. I described why The TIPS ladder provided over a four percent safe withdrawal rate. I started with $100,000 to test the process. It worked so well that I increased it to well over a million dollars even before the article published. It was clunky to build and took me days. Today, it takes about an hour. But before I walk you through the steps, let’s first describe why.

About two years ago, I built my million dollar 30-year TIPS ladder. I described why The TIPS ladder provided over a four percent safe withdrawal rate. I started with $100,000 to test the process. It worked so well that I increased it to well over a million dollars even before the article published. It was clunky to build and took me days. Today, it takes about an hour. But before I walk you through the steps, let’s first describe why.

Why build a TIPS ladder?

I’m a pessimist and most of my clients are as well. We save money because we fear a future scenario where we might not have enough of it to live a desired lifestyle. If the government does not cut Social Security, we will all have some money coming in − but that’s not enough for most of our clients to live on. The world is and always has been risky and it’s feeling riskier than usual. What if stocks have a real and protracted plunge rather than the teddy bears we have had this century? What if all of this government debt causes hyperinflation?

Building a TIPS ladder gives us a license to spend and creates a spending floor. My TIPS ladder combined with Social Security provides a $10,000 monthly inflation-adjusted cash flow, though I’m delaying taking Social Security until age 70, of course.

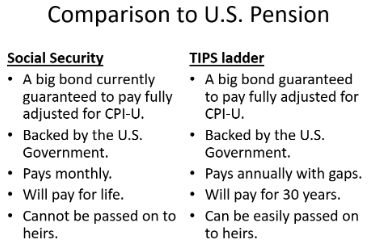

Below is a comparison of a 30-year TIPS ladder to Social Security or most U.S. Government pensions. While the TIPS ladder can only pay for 30 years, it does have a 100 percent survivor benefit for the heirs.

How to build a TIPS ladder

It’s so much easier to build a TIPS ladder today than when I built my own. It now takes me roughly an hour once the client has decided on the amount and the number of years in the ladder. In addition, there are now only five years missing on the ladder where no TIPS mature.

My tool of choice today is tipsladder.com/spa. Created by Kevin Esler, it’s a free tool that he designed to help people. I’m also grateful to Bob Hinkley for his eyebonds.info tool, which I used to create my first ladder.

Here’s a step-by-step example of building and buying a 30-year TIPS ladder to generate as close as possible to a $40,000 annual inflation adjusted cash flow.

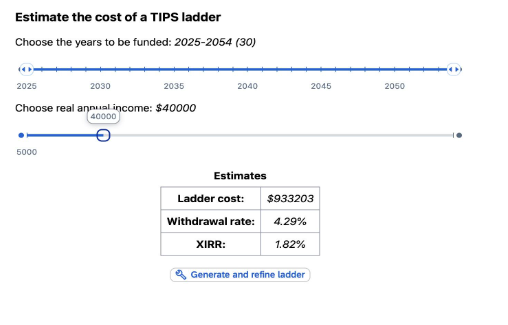

Step one: Estimate the cost of the proposed ladder. First, I want to make sure the client can raise enough cash to purchase a ladder providing the desired annual real income for the time period between 2025 and 2054. To do so, navigate to the “Estimate” page at http://tipsladder.com/spa/estimate and set the slider accordingly. Then move the second slider to the desired annual real income: $40,000.

The table above shows that such a ladder will cost about $933,203. This page can also be used to answer a question like, “How much real annual cash flow can I create with a certain amount of money?” Simply move the income slider until the ladder cost reaches this amount.

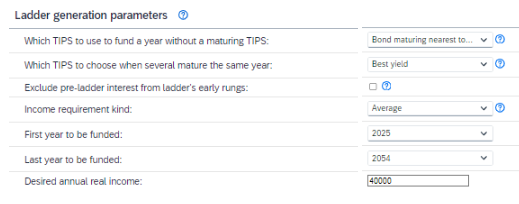

Step two: Create the ladder. Press the “Generate and refine” button at the bottom to navigate to the “Generate” page, https://www.tipsladder.com/spa/generate, which will be pre-set with your chosen year-range and income parameters. The input here is simple and requires only seven parameters. These inputs are as shown in the graphic below:

I typically leave the first five inputs in the default selections so I only change the last two in this example.

- You would see in the actual site the full text that reads “bonds maturing nearest to start of rung year.” This refers to the gap years between 2035 and 2039 where the Treasury has not yet issued any TIPS that mature in those years.

- When there are multiple TIPS maturing in the same year, I use the default of the TIPS with the highest yield.

- You have the option of excluding any interest being paid before the year your ladder begins. If I’m having the ladder start in the next year, I keep the default which is to include the pre-ladder interest. It makes very little difference for a ladder starting in the next year but this option could be selected for a ladder that wouldn’t start for a few years. For example, a ladder starting in 2029 would have five years of coupon payments that could be excluded.

- I have always selected the default “average” income requirement. The program calculates the number of bonds needed in each rung to come as close as possible to the desired annual real income. You can’t buy fractional TIPS so there will always be variation.

- So far, I’ve always built ladders starting in the next year so 2025 is the default. One can start later on, however.

- The default on the last year to be funded is 2034 though I typically build a much longer ladder. That’s because the TIPS ladder provides far more inflation protection in the later years if we have many years of prices compounding due to higher-than-expected inflation. I’m using 2054 in this example for a 30-year ladder.

- Input the desired real annual income. It’s actually a desired real cash flow since some of the cash flow is return of principal.

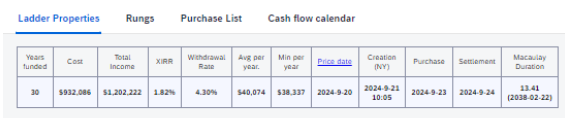

In essence, all that needed to be changed was the last year to be funded (to 2054) and the desired income (to $40,000), and that’s only if I didn’t start with the step one estimate. The summary of the solution appears at the bottom of the web page as follows, using prices as of September 20, 2024.

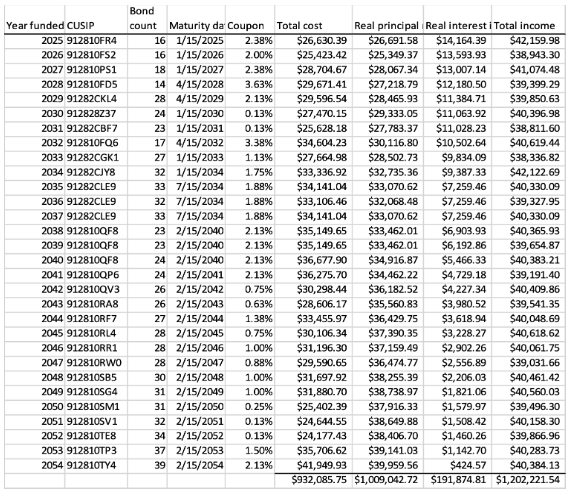

This ladder will cost approximately $932,086 to build and generate a 1.82 percent annual return above inflation. It provides a certain 4.30 percent annual real withdrawal rate for 30 years. Note the three other links “Rungs,” “Purchase list,” and “Cash flow calendar.” Click on the “Rungs” button to see a list that can be downloaded to an MS Excel spreadsheet as follows:

The bond CUSIPs are the same for years funded between 2035 and 2037 and again the same for years funded 2038 to 2040. That’s because of the gap where the Treasury hasn’t yet issued TIPS maturing between 2035 and 2039. Some bonds will mature in 2034 to fund the next three years and some maturing in 2040 must be sold to fund 2038 and 2039. This was the option chosen in the first input field.

The ladder funded an average of $40,074 real cash flow annually. The highest annual cash flow is $42,160 in 2025 while the lowest is $38,337 in 2033. Again, it’s impossible to get the same cash flow each year because fractional TIPS cannot be purchased at this time.

Step three: Review with client. Review the results with the client, explaining that the cash is coming from a combination of coupon payments and maturities. Make sure the client understands two things:

- The market value of the ladder will be quite volatile. The longer-term TIPS will be especially volatile but, held to maturity, the real spending power is certain. The client must have the courage to do nothing – which isn’t as easy as it sounds.

- If in a taxable account, explain “phantom income tax.” I tell clients that it’s similar to letting interest compound in a CD where the IRS taxes us each year but not a second time when the CD matures. I also explain that all of the interest is state tax-exempt which is especially important if they live in a high tax state.

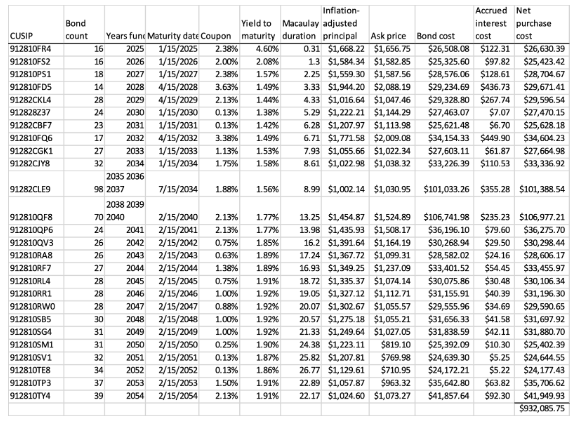

Step four: Buy the TIPS. Return to tipsladder.com and click on the “Purchase List” button and download to MS Excel as shown below. You should re-run the ladder if you suspect prices have changed significantly between the time you created the ladder and actually buying the TIPS.

Note that the TIPS are combined during the gap years when there are no TIPS that mature. So there are a total of 26 TIPS that must be purchased with varying quantities.

I thought it would be child’s play to make these purchases online. However, even though the current ask price is accepted, I found that sometimes the trade doesn’t execute and later was cancelled. The bond desk explains that this is because the prices are constantly changing and even a few seconds can cause the seller to reject the ask price.

Instead of doing it online, the client or I email the list to the bond desk and review it over the phone. The bond desk has the CUSIPs and quantities and confirms each purchase with the client and then buys. Mistakes happen, so make sure they have the right bonds and quantities. If the trade doesn’t execute, the bond desk will know in seconds and initiate a new purchase at the current price.

Usually, buying the bonds in the ladder takes no more than a half hour. Sometimes when the bond desk is used, there can be a fee of roughly $20 for each trade (which would amount to $520 in this case). However, in my experience, the bond desk has always waived the fee. There are no commissions on trading TIPS.

Summary

In roughly an hour, this client would now have a supplemental inflation-adjusted cash flow to their Social Security. They know the spending power it has created, assuming their inflation is similar to the CPI. Though much simpler than when I built my TIPS ladder, it’s still admittedly more complex than buying one ETF or mutual fund but, thanks to tipsladder.com and eyebonds.info, it’s not nearly as complex as it once was.

Going forward, the client can return to simplicity and do nothing other than collect the cash and use it to enjoy life. The TIPS ladder is the only thing I’ve found in investing that both feels good and makes great economic sense. Typically, in investing, moves that feel good are actually bad, such as selling stocks after a plunge versus buying to rebalance.

The emotional value of the TIPS ladder is that it creates virtual certainty of spending power in a worst-case scenario where either stocks tank 90 percent, inflation stays at double digits, or both. This sense of well-being is a license to spend and enjoy the money that the client has worked so hard for.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All