Help Clients Save Money on Property and Casualty Insurance

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Property and casualty insurance rates continue to skyrocket. Insurance Newsnet attributes the large increases to the following:

Property and casualty insurance rates continue to skyrocket. Insurance Newsnet attributes the large increases to the following:

- Inflation costs being passed to consumers

- More cost and time involved with auto insurance claims

- Reinsurance costs being passed to consumers

- Climate change causing increased risk

- Insurance carriers leaving the state or market

- More claims and/or litigation from consumers

- Changes in consumer behavior

Double-digit increases in rates are common. I’m definitely feeling the pain, as I suspect you are. So here are a few things I do to help my clients save some money.

Determine the types of insurance you need

Let me start with the obvious type many people seem to overlook. Insurance companies expect to cover their costs, pay commissions, and make a profit. Translation: You should expect to lose money on every property and casualty insurance policy you buy. This is true whether it’s a home, renter’s, auto, umbrella, or any other policy. While I’ve heard many times that one should fully insure against losses, I say one should only insure for losses that would be catastrophic. In other words, the purpose of insurance is to protect wealth.

Let’s start with an extreme example. I have a smartphone for which I could pay $10-20 a month to insure. Now, if I lose or break my phone, I will have wished I had bought the insurance, but it will have no consequences to my family’s lifestyle. We wouldn’t have to cut spending on anything else. It’s an easy decision to self-insure. By that I mean, I can afford to take the loss as it’s not insurance I need.

On the opposite extreme, I have a pretty large umbrella insurance policy. Should I accidentally severely injure someone (or worse), that would be a financial loss that would have a catastrophic impact to my family’s lifestyle. It’s insurance I hope and expect I will never need, and it’s fairly inexpensive for the same reason: Claims are few – though the size of claims are typically huge. As I put it to my clients, the probability of needing to use umbrella insurance is low but the consequences are enormous. Like me, the vast majority of my clients need an umbrella policy.

Now, I surprise many clients when I tell them I have no collision or comprehensive insurance on our two cars and, in many cases, I tell clients they should consider dropping theirs as well. My clients, and likely yours, tend to be wealthy. Totaling a $40,000 car is certainly a large loss, but when you frame it against the total net worth, it’s a whole lot smaller now than when we were young and starting out.

I note how many single days their portfolio goes up or down by that amount and suddenly this risk doesn’t seem so large. Further, I explain that if I did something dumb like back into a tree and cause $4,000 in damage to my car, I wouldn’t even file a claim. That’s because the insurance company would likely raise my rates and I’d end up paying at least as much as the amount I’d receive from the claim above my deductible.

Determine the right amount of insurance to buy

So let’s say that after the analysis in the previous section, the client needs the following property and casualty insurance:

- Automobile

- Homeowners

- Umbrella

It’s important to understand that umbrella insurance interacts with both auto and homeowners insurance, and there are levers within each of these that trade off the coverage versus the price.

I typically recommend increasing the deductibles on insurance, which is essentially partially self-insuring. Assuming the insurance company is acting rationally, they will lower the premium when you increase deductibles, for two reasons. First, their potential liability is reduced; and, second, their administrative costs will also likely decrease with fewer claims filed.

Using auto insurance as an example, say the client isn’t comfortable dropping collision and comprehensive insurance, but perhaps is OK with increasing the deductible from $500 to $2,500. That might decrease the premiums by $300 a year, so the client is really only taking on an additional $1,700 of exposure that first year. And, as previously mentioned, I wouldn’t advise filing a claim for a $4,000 fender bender irrespective of the deductible I had.

As far as how much automobile liability insurance you need, typically, I recommend the minimum required by law, since it’s generally less expensive to buy umbrella insurance to cover any excess liability.

Homeowners insurance is a bit more complex to analyze. Increasing deductibles is one lever, but decreasing the amount of insurance typically isn’t. For example, if a client had a $1 million home with an $800, structure and a $200,000 lot, they may want to buy $600,000 in insurance and self-insure for the $200,. Unfortunately, the insurance company typically won’t allow this. That’s because they would be on the hook for the first tier of damages. In other words, a fire causing $400,000 in damages would fall on the insurance company, but they wouldn’t have received the same level of premiums they would have if it were fully insured.

There are other levers to reduce fees within homeowners insurance, such as riders on the policy. This could include a jewelry rider or other specific items or guarantees. Also, if you live in an area prone to floods or earthquakes, you may need separate insurance for these events as well. With the rapid increase in climate disasters, many insurance companies are dropping coverage or raising rates to virtually unaffordable levels.

As mentioned, umbrella insurance is critical to protect wealth. It typically is linked to auto or homeowners insurance and pays out above those limits. The rule of thumb I’ve heard countless times as to how much coverage to have is, “you need to have your net worth in umbrella insurance.” I’ve researched this rule and find no logic in it. The client could have a $50 million net worth and get sued for $100 million. Furthermore, certain assets are more protected than others. For example, 401(k) plans have additional ERISA protection, and many states exempt part or all of the value of one’s home from lawsuits. Other wrappers such as irrevocable trusts or insurance investments have additional protections, though they come at a cost.

With all that said, I’ve never developed a simple calculation to advise a client on umbrella insurance. Certainly, the greater the net worth outside of protected assets increases the need for umbrella insurance, but that doesn’t mean it should be in the full amount of those unprotected assets.

Shop before you pay next year’s premium

People will spend hours getting the best deal on inexpensive things and then not think twice about paying those large insurance renewals with hefty rate increases. I suspect many insurance companies count on this inertia. I tell clients to gather those insurance policies and get quotes based on the analysis discussed above. For better or worse, I’ve found that every insurance company bundles multiple policies with discounts, meaning it never seems to be cost-effective to buy auto from one company and homeowners from another. In fact, it may even pay to buy a policy you don’t need if the discount on the other policies is greater than the premium.

Get quotes from at least a few companies, including your current insurance company. Don’t just pick one company that advertises it saves customers who switched an average of $500. It’s fine to include that insurance company, but remember, they aren’t telling you how many people didn’t switch because it was more expensive.

Some insurance companies use independent insurance agents who can get quotes from multiple insurers – though not all. That’s because other insurance companies use what are called captive insurance agents, and will only work with those agents. Example of these include Allstate, State Farm, and Geico. Progressive, Liberty Mutual, and Travelers are examples of companies that work with independent agents.

I tell clients to contact both an independent insurance agent as well as two or three insurers using captive agents. Then compare the quotes and choose the two or three that have the lowest rates. Go a step further and see if there are additional levers to be pulled, as I’ll discuss shortly. Be sure to look up customer satisfaction in places such as the J.D. Power auto insurance customer satisfaction survey.

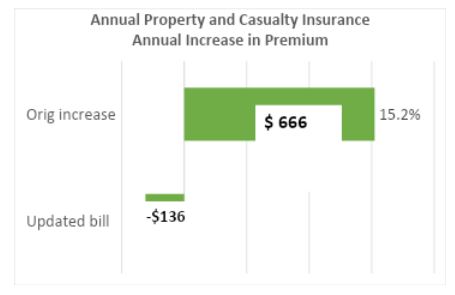

A personal case study: Turning a 15.2% increase into a 3.1% decrease

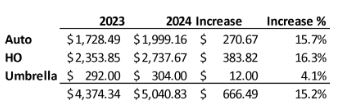

My own personal property and casualty insurance is with Auto Owners. We’ve been with them for many years and have never filed a claim other than a cracked windshield after being assured it wouldn’t increase our rates. The cost to repair was less than $100. Still, like everyone else, our renewal bills showed up a few months ago, and we’d been hit with a 15.2% increase.

companies, but they were even more expensive. The Auto Owner’s insurance company I use is said to cherry-pick clients with high credit scores and a history of not filing claims, so I wasn’t shocked. Higher credit scores are correlated to fewer claims, so it’s legal to give discounts based on FICO scores.

Luckily, I was assigned a new agent at my independent insurance agency. I explained to her that my philosophy was to insure only for what I couldn’t afford to lose, and I asked her to look at any additional levers available to lower rates and still allow my wife and I to sleep at night. She came up with the following:

- Change Personal Property from $567,350 to $405,250 (50% of Dwelling coverage – the minimum required, which is included in the premium) – savings: $90.11 per year.

- Delete Homeowners Plus Endorsement – savings: $13.90 per year.

- Delete Guaranteed Home Replacement Cost Coverage and add 25% Increased Cost Endorsement – savings: $273.44 per year.

- Delete Special Personal Property Coverage – savings: $202.59 per year.

- Delete Other Structures off Premises Replacement Cost – savings: $4.13 per year.

- Lower Bodily Injury Coverage & Uninsured/Underinsured Motorist to $300,000/$300,000 from $500,000/$500,000 – savings: $274.97 per year. It increased the cost of the umbrella policy by $57, so the net savings is $217.90. The net impact was to change our liability coverage from $3.3 million in coverage with our umbrella, rather than $3.5 million.

I must confess the above findings don’t make me look very good. I’m guilty of not digging into my coverage. I won’t get into the details of each of these changes, but essentially, I was paying mostly for insurance I could never actually collect a penny from. Our personal property isn’t worth nearly the reduced amount, and we could easily rebuild our home for the current insured amount and didn’t need that replacement cost guarantee. While only a few bucks a year, I’m embarrassed that we were paying for “other structures” when we didn’t have any.

The only significant coverage we reduced was the liability in our auto insurance. Previously, we had $3.5 million comprising $500,000 auto and a $3 million umbrella, and it declined to $3.3 million when we reduced the auto liability to $300,000.

The net savings was about $813 a year in premiums, or a decrease of about 3.1% from the previous year, which was a big improvement from the 15.2% increase. To these numbers, I’ve excluded a small $5,000 term policy we had before and after the renewal. We certainly don’t need this, but the multipolicy discount it provides on the property and casualty insurance is greater than the annual premium.

Insurance agents are generally very nice people, but remember that incentives matter in every profession (including financial planning). Agents have a financial incentive for you to buy as much insurance as you want. It takes a lot of time for an insurance agent to find savings, and those savings will reduce their commissions since they are typically based on the premium.

Conclusion

Insurance isn’t simple. I suspect the complexities are designed in such a way to make it hard to compare and understand the entire package. My advice is:

- Don’t mix investing and insurance. The purpose of investing is to grow wealth, while the purpose of insurance is to protect wealth.

- Insure only for what the client can’t afford to lose. The sole exception is when the savings from bundling the multipolicy discounts is greater than the premium for the additional policy not needed.

- Fight inertia and shop for the best insurance every year or two.

- Make sure you have an agent who will go above and beyond to find savings without jeopardizing your financial security.

I sure hope these double-digit rates increase moderate soon. But if they don’t, we can add even more value to our clients by helping our clients navigate these complexities.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All