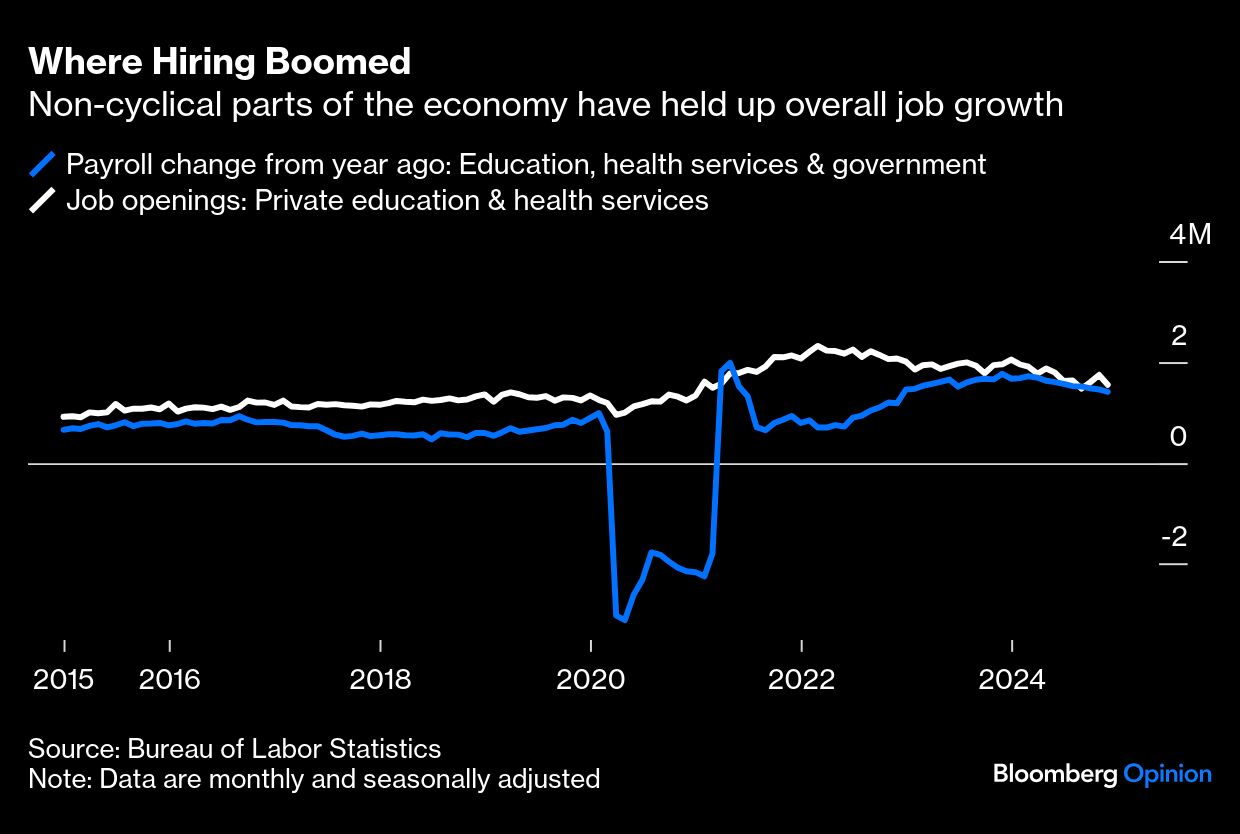

The resilience of the labor market over the past year has, in large part, been about strength in sectors such as education, health care and government that are somewhat immune to economic cycles. Continued robust hiring there has contrasted with weakness in more cyclical industries including construction, manufacturing and professional services. So long as that balance remains, we can muddle through without unemployment spiking, even if high interest rates and the prospect of a trade war keep some employers sitting on their hands.

The problem is that those less-cyclical parts of the labor market are also cooling off. Unless we get a pickup elsewhere, employment prospects for job seekers will weaken in 2025.

Out of the 2.2 million jobs added in the US in 2024, 1.4 million were in education, health care or government. In the 2010s, a solid contribution from those industries was closer to 700,000 positions per year, half of last year’s pace. These industries were laggards in the post-pandemic recovery, taking longer to normalize than food services or construction. Schools and hospitals weren’t getting into bidding wars for workers the way airlines or restaurants were in 2021. Government employers took longer to disburse the funds they received as pandemic relief or under President Joe Biden’s fiscal support programs. In some cases, it has taken weakness elsewhere for workers to accept the lower pay but relative stability of positions in education and government.

But the data show that the pandemic adjustment is now drawing to a close. Job openings in private education and health services remain above 2019 levels, but they fell 20.7% year-over-year in 2024, according to the Job Openings and Labor Market Survey data released this week. Openings in government fell 12.4% from a year ago, and that was before the Trump administration took office and began looking to cut seemingly every job it can.

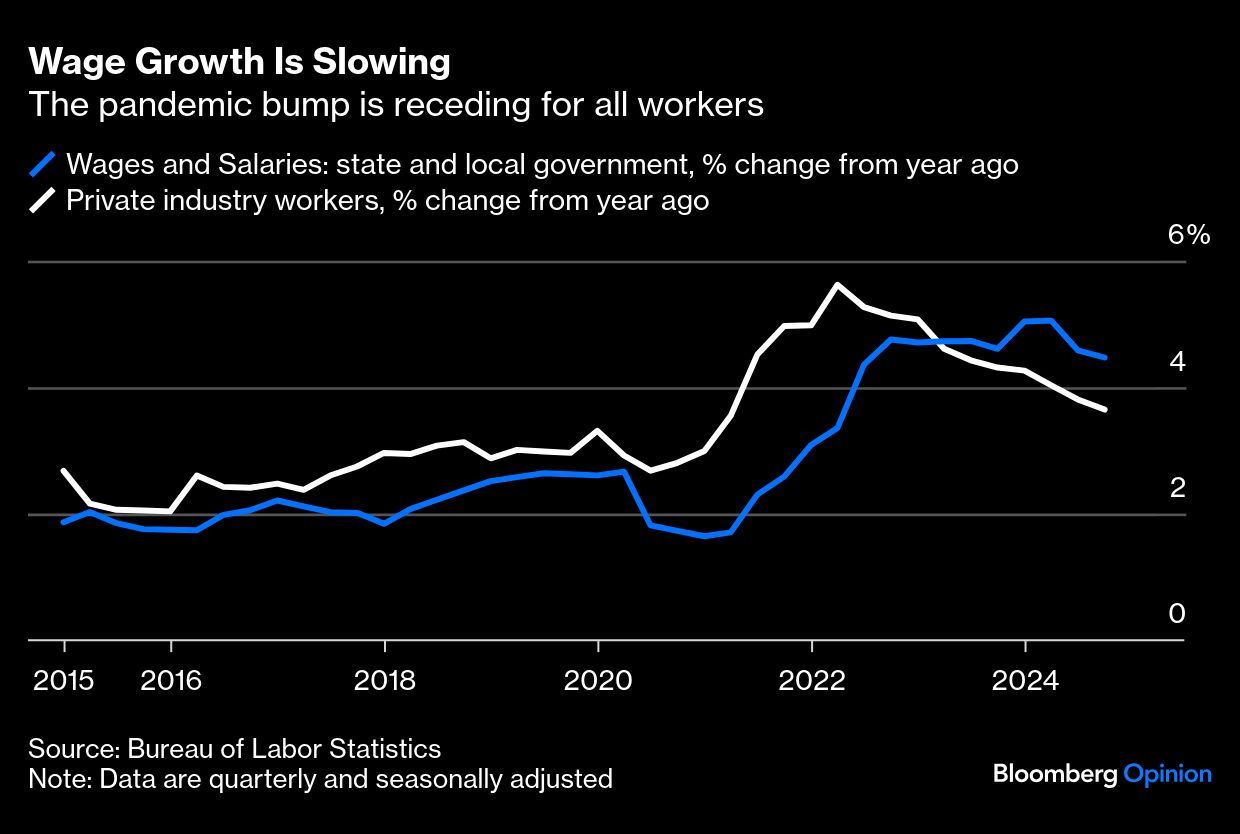

The dynamic in industries such as construction, manufacturing, and professional and business services is currently one of low hiring, and we’re seeing the same situation take hold in education, health care and government once job openings are filled. For federal and state governments, budgetary pressure and political shifts suggest an even more pronounced slowdown in 2025. This lagged labor market cooling is perhaps best seen in the quarterly Employment Cost Index report, where private sector wage growth is rapidly returning to pre-Covid levels while wage growth for government employees is much earlier in the cooling process.

There’s a world in which a mix of interest rate cuts from the Federal Reserve and the new administration’s pro-business policies encourage a labor market handoff from less-cyclical industries to more-cyclical industries. But that’s not the situation we find ourselves in at the moment.

While the Fed has cut interest rates by 100 basis points since September, longer-term rates have risen. Residential construction and resale housing activity remains subdued. And while the business community has been hopeful about the impact of the Trump administration, there’s so far not much visibility on the prospects for tax reform from Congress or deregulation. Instead, we’ve had an increase in tariffs on Chinese imports, and the threat of duties on goods from Mexico, Canada and the European Union — something that will raise costs for many businesses. The one part of the economy that’s booming is artificial intelligence, but its insatiable demand for semiconductors, data centers and electricity hasn’t yet translated into demand for many additional workers.

The bottom line is that as we progress through 2025, we’re going to need “low hiring” industries to start turning around to prevent labor market conditions from getting worse. Lower interest rates from the Fed or pro-worker policies from Washington would be the best ways to accomplish this, but it may take a pickup in unemployment for those to become a priority again.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Conor Sen