Alternative investments including hedge funds and real estate will disappear from the portfolios of pension funds and endowments over the next 10 to 20 years, well-known institutional investment consultant Richard Ennis concludes in a recent report. Their trustees, he says, will wise up to the excessive fees and anemic returns from these alternatives compared with passive index investment in public stocks and bonds.

On the good side, the report is a readable and up-to-date summary of criticisms of alternative investments along the lines of classics like “Do hedge funds hedge” and “Demystifying illiquid assets.”

On the bad side, this is a classic example of chasing returns. Over the last 16 years, the S&P 500 Index’s total return, adjusted for inflation, has been a continuously compounded 12.72% — the fourth highest going back to 1871 and far higher than the average of 7.05%. If you knew this back in 2008, you’d have put everything in an S&P 500 index fund. There would have been no reason to diversify into alternatives. So, this is the period Ennis chooses for evaluation.

To understand the problem of return chasing, consider what happened after the three best 16-year periods in history. In 1937, you’d have been looking at a 13.82% continuously compounded annual return above inflation over the prior 16 years. Despite the stock market crash of 1929 and the Great Depression, you would have profited from the bull market of the 1920s, the sharp recovery from stock market lows in the early 1930s, and the negative inflation rate during the Depression. Over the next 15 years, you would have earned a below-average 4.12% annualized real return.

In 1965, things looked better but turned out to be worse. The postwar recovery of the 1950s and early 1960s delivered a 14.88% annualized return above inflation, the next 15 years of economic malaise and stagflation resulted in a negative 0.30% return. In 1998, you’d have looked back on 15.84% annualized real returns but realized only 2.82% going forward.

While no one knows what the next 16 years will bring, history argues that it is prudent to diversify your portfolio away from an excessive reliance on strong public equity returns. No one suggests getting out of equities completely — equity risk remains the driver of investment returns in modern economies — but most investors are overexposed to it.

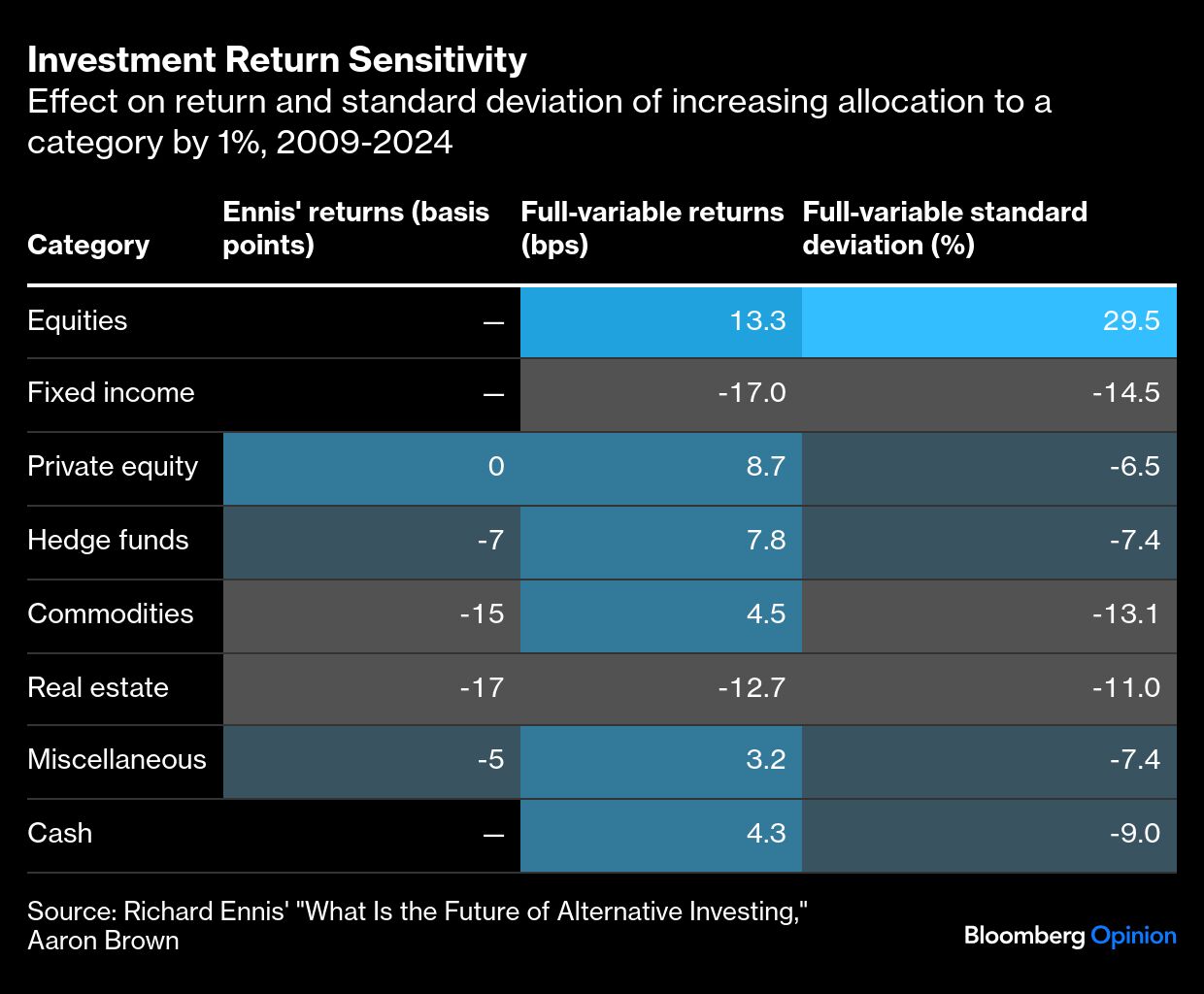

Ennis’ paper presents return data on individual types of alternatives, but this is not a useful way to evaluate them. One problem is that the data are not complete or reliable. Another is that these are not intended as stand-alone investments, they are used for diversification and hedging rather than return enhancement. Most important is that they don’t represent actual investor experience. Many good funds are not in public databases, and many other good funds don’t take new investors. Institutional investors do not choose funds at random; they select tailored portfolios after extensive due diligence. The relevant question is whether investors who use alternatives do better in the long run, not what’s the average return of all alternatives.