Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

A catch-22 is a paradoxical situation from which an individual cannot escape because of mutually conflicting or dependent conditions. The term was coined by Joseph Heller, who used it in his 1961 novel, Catch-22 (which was followed by a movie of the same name in 1970). The book invokes the term "Catch-22" as a fictional military rule that decrees any pilot requesting mental evaluation for insanity – hoping to be found not sane enough to fly and thereby escape dangerous missions – demonstrates his own sanity in creating the request and thus cannot be declared insane.

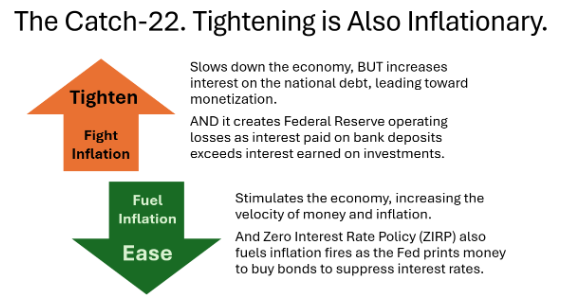

The Fed currently finds itself in a Catch-22 situation with interest rates.

Rates left untouched at Fed’s March meeting

The Federal Reserve announced on Wednesday that it will leave interest rates unchanged, despite pressure to resume the reductions it started last year. Regardless of the fanfare, this decision doesn’t matter much; bigger forces are in play. The Fed’s decision doesn’t move the needle, and that’s all right. Let’s take a look at where we are today and where we are heading.

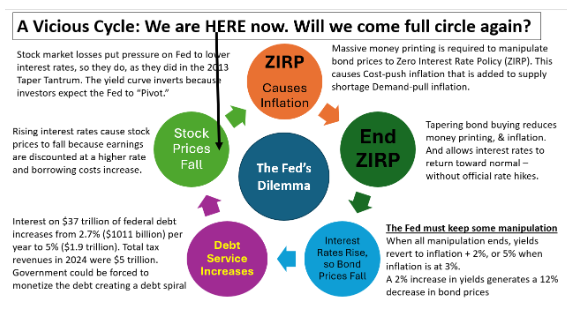

I’ve shown you the following cycle before, but in the last 45 days the “We’re Here” arrow has moved clockwise to “Stock Prices Fall.” Do we really want to go around this cycle again, and again, and…? Dizzy yet?

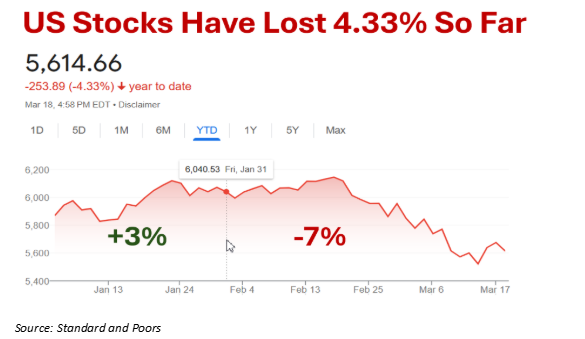

2025 started out really well, with a 3% return on the S&P 500 in January, but since then the stock market has declined 7%, putting pressure on the Fed to stimulate the economy by lowering interest rates.

However, the US economy is growing nicely at more than 2% per year. It doesn’t need stimulation, so reducing interest rates will fuel inflation fires.

Even though inflation appears to be under control, thus justifying rate reductions, threats of inflation loom large.

Inflation threats that overhang the economy

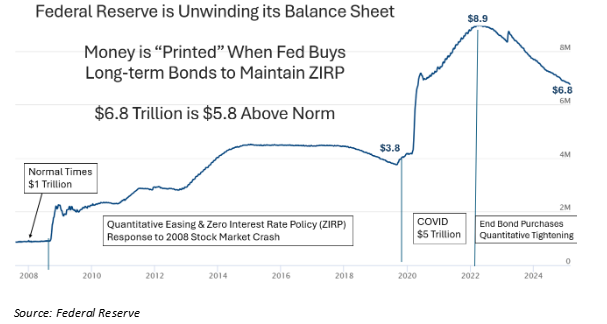

There’s no doubt that recently enacted tariffs are inflationary and a primary cause for recent stock market declines, but there is also the fact that the U.S. has printed lots of money in the past 15 years, as reflected in the Fed’s balance sheet.

Prior to the stock market crash of 2008, the Fed’s balance sheet was maintained at a constant $1 trillion. But then we printed money to save the economy. Despite being considered a controversial move, it has worked so far, since stock prices skyrocketed and inflation was under control – except for a blip caused by COVID-induced supply shortages.

Warren Buffet observes that quantitative easing (QE) is an experiment of consequence and magnitude that has never been run before. His concern is in its unwinding, because QE cannot go on forever. It did end – at least for now – in 2022.

Money printing ended in 2022, and the Fed has been unwinding its balance sheet under quantitative tightening (QT) ever since. The experiment is gradually and cautiously ending.

But $5.8 trillion remains sloshing around in the economy that will cause inflation if money circulation – AKA “velocity” – picks up. According to Perplexity AI, velocity will increase during:

-

Economic expansion: During periods of economic growth, consumers and businesses tend to spend money more readily, causing the velocity of money to increase.

-

Higher interest rates: Rising interest rates can increase velocity by reducing real money balances relative to personal consumption, encouraging more frequent transactions.

-

Improved payment systems: The availability of credit and electronic banking can reduce barriers to transactions, leading to increased velocity.

-

Consumer behavior: When consumers prioritize spending over saving, the pace of transactions accelerates, increasing the velocity of money.

-

Inflation: Higher inflation rates are often associated with increased velocity, as people tend to spend money more quickly to avoid losing purchasing power.

-

Technological advancements: Innovations that facilitate faster and easier transactions can contribute to higher velocity.

-

Increased economic activity: More transactions occurring throughout the economy naturally lead to higher velocity.

We’ll “feel” more than egg prices when velocity increases, and the causes for increases are definitely in play.

A delicate balance: Rising interest rates expedite an imminent debt spiral

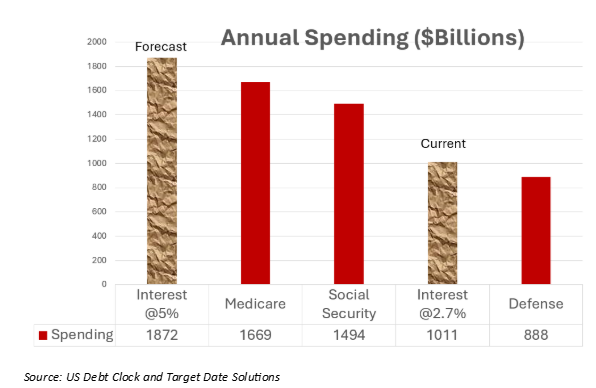

The Catch-22 in fighting inflation by raising interest rates is that this increases payments on our enormous $37 trillion national debt. As our debt swells to unsupportable levels, we will be forced to monetize it as were Argentina and Venezuela – wealthy countries that were boxed into a monetary corner.

We (U.S. taxpayers) are currently paying 2.7% on our debt, so $1.1 trillion. That makes it our third largest expense. But interest rates are currently much higher than 2.7%, so interest on our debt is increasing as old issues mature and new bonds are issued.

When interest payments on our debt reach 5%, debt service will be our largest expense, and the deficit (expenditures minus tax revenues) will more than double from $2 trillion currently to more than $4 trillion per year, swelling the national debt way above current levels. This could lead to printing more and more money, which is called “monetizing the debt.”

The Catch-22 is that keeping interest rates low under ZIRP – zero interest rate policy – is also inflationary, because the Fed needs to step in to buy new Treasury issues. Zero interest rate bonds do not clear the market, so the Fed buys what is required to suppress interest rates.

The Fed’s operational dilemma

As stated above, Warren Buffet is concerned about exiting QE. One aspect of the challenge is manifested in the Fed’s operating deficit. The bonds it holds are paying much less interest than Federal Reserve banks pay on their deposits, so it is losing hundreds of billions of dollars. This is accounted for by a “deferred asset” on the balance sheet. As the name suggests, the expectation is that someday those losses will be recovered. An income of $156 billion versus $400 billion paid to depositors creates an operating deficit of $244 Billion.

Conclusion

Quantitative easing has created serious inflation threats. The only way out is to increase tax receipts and reduce government spending, neither of which is in the Fed’s purview. Otherwise, serious inflation lies ahead, regardless of Fed actions. The good news for older people is that the reckoning might not happen in their lifetimes.

All investors can and should prepare for inflation on the horizon, and protect with investments like the following:

- Treasury Inflation-protected Securities (TIPS);

- Precious metals, especially gold;

- Some real estate, like farmland;

- Natural resources;

- Cryptocurrencies;

- Consumer Staples; and

- Some hedge funds.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.