The Emotional and Time Value of Advice

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Managing personal finances can be stressful and time-consuming given the complexity and critical nature of financial decisions. In this paper, we study the emotional benefits and time-saving value that paid professional financial advice provides to clients. Using a survey of 12,443 investors (including 7,746 advised clients), we found that:

- Advised clients are less financially stressed than self-directed investors. Advised investors are roughly half as likely (14%) as self-directed ones (27%) to experience high levels of financial stress.

- Advice delivers emotional value to clients through more peace of mind. 86% of advised clients report having greater peace of mind when thinking about their finances, compared with managing them on their own. Advice improves investors’ positive emotions and seems particularly effective at lessening negative emotions regarding personal finances, such as feeling overwhelmed and worried.

- Advice saves clients time. 76% of advised clients say advice saves them time — namely, a median of two hours per week (or over 100 hours per year) — from thinking about and dealing with their finances.

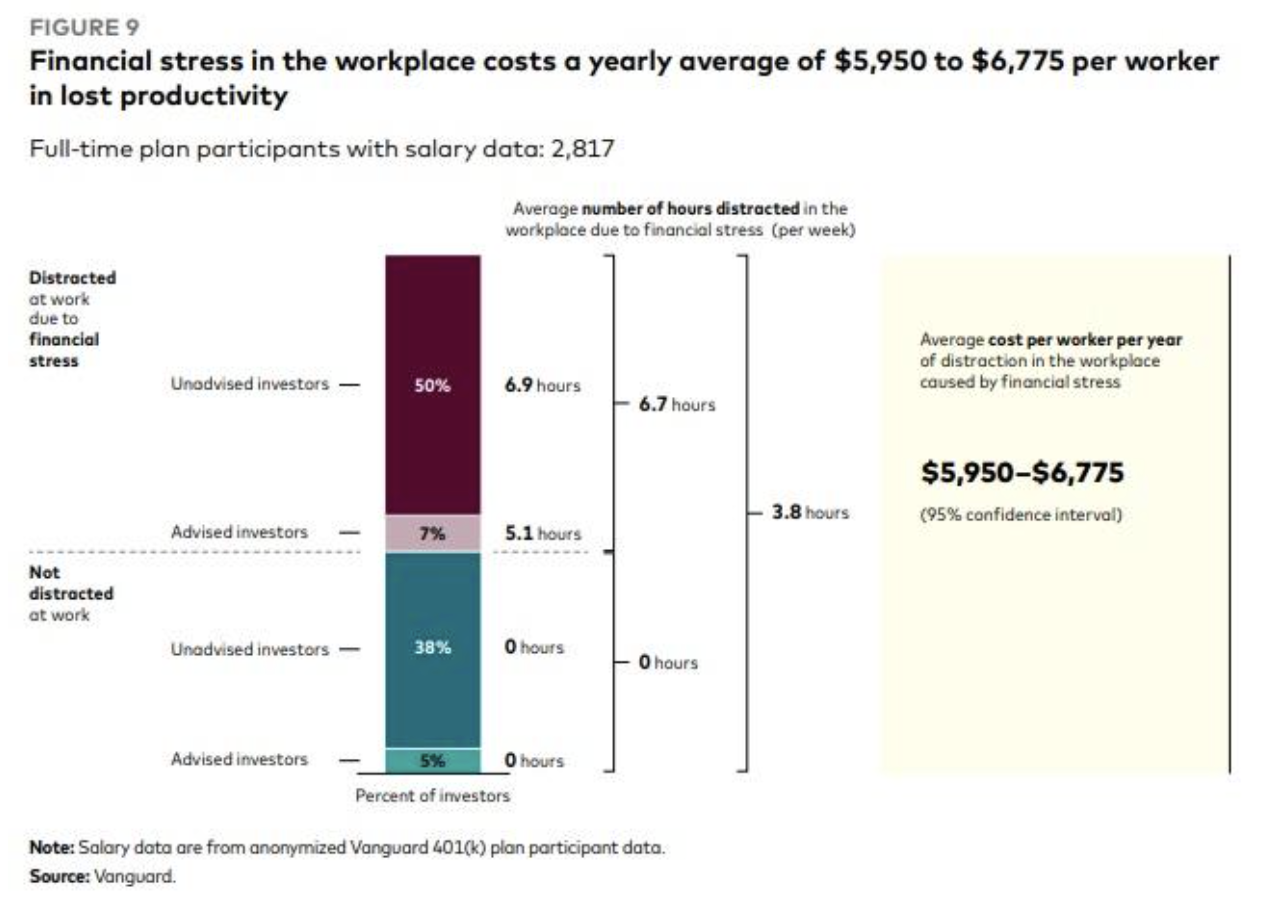

- Advice saves employers time through employees’ reduced financial stress. Workers in employer plans report spending an average of 3.8 hours per week distracted at work by financial stress, leading to a yearly productivity loss for employers of $5,950 to $6,775 per employee. Half of the advised clients in employer plans say advice reduces financial stress at work. Overall, advice saves clients almost two hours per week at work (over 100 hours per year), improving worker productivity by $2,200 to $5,850 per year.

Assessing the value of financial advice

The financial advice industry has traditionally focused primarily on money management (mostly through portfolio construction and monitoring) as the key measure of its value. Focusing on financial benefits, however, often overlooks other important benefits that investors gain from paid professional financial advice, such as peace of mind and the time they save by delegating their financial lives to an advisor (Gennaioli, Shleifer, and Vishny, 2015; Kim, Maurer, and Mitchell, 2016; Rossi and Utkus, 2024).

Recognizing the value beyond money management, Vanguard has developed a model of financial advice that also incorporates emotional outcomes and the time saved by investors. Figure 1 presents Vanguard’s framework for quantifying the value of personalized advice (Weber et al., 2022). In that research, the authors also measured the portfolio value and financial value provided by advice.

This paper examines the emotional and time benefits of having financial advice. Emotional value is defined as the financial peace of mind provided to clients. Time value refers to the hours clients save by not having to think about and deal with their finances.

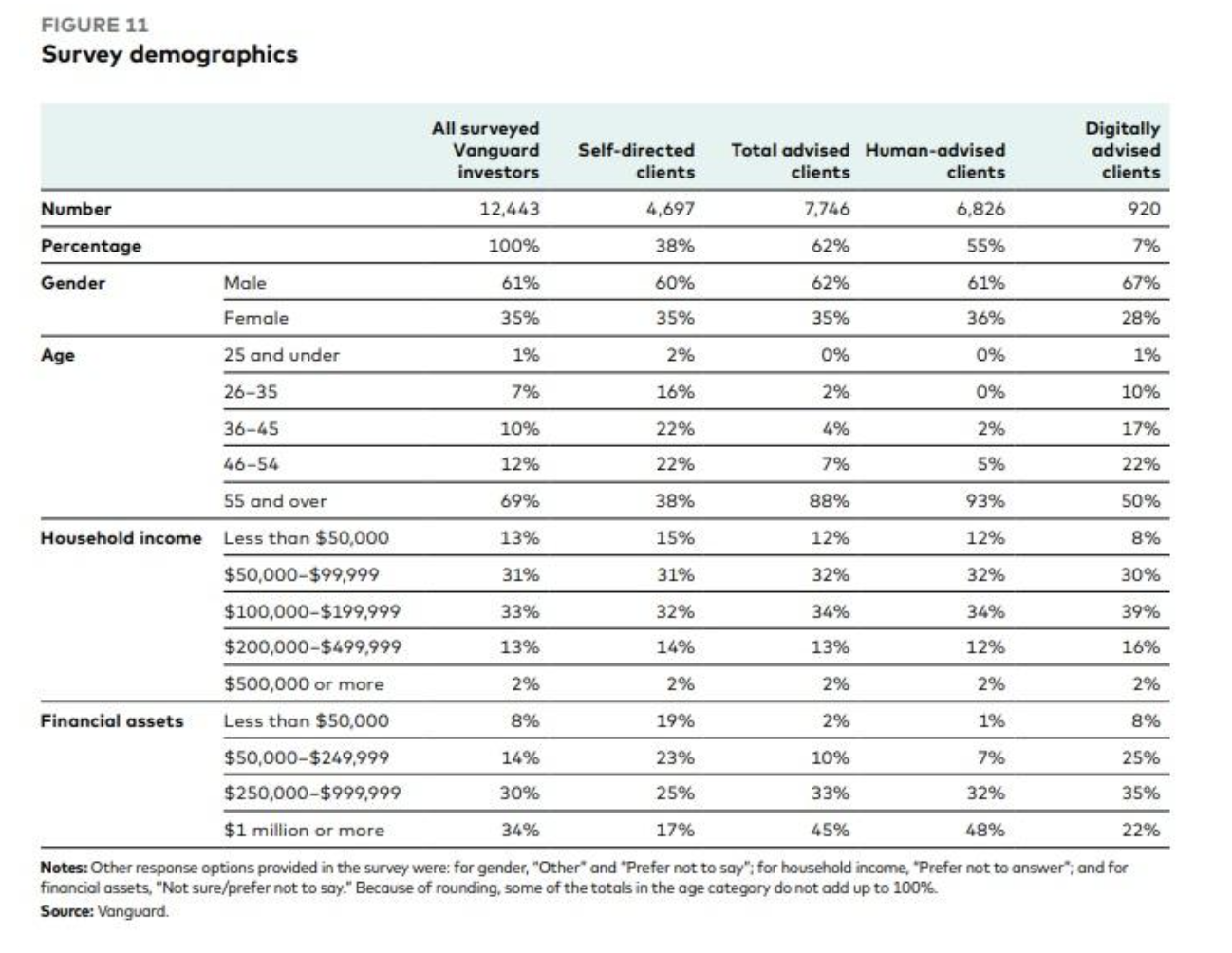

To measure the emotional and time value of advice, in July 2024 we conducted an online survey of 12,443 Vanguard investors, including 7,746 who are also advised by Vanguard. Our sample included both working and retired clients. They answered questions about their emotions regarding their finances, the time they spend managing them, their thoughts on financial advice and financial well-being, and some demographic information. The Appendix at the end of this article details the demographics for our sample, including financial characteristics.

We studied emotional and time benefits together because recent research has shown that financial stress is highly correlated with the number of hours people spend on financial issues and are distracted in the workplace because of them (Sergeyev, Lian, and Gorodnichenko, 2024). Our survey finds a similar correlation, with one important additional finding: For a given level of stress, advised clients seem to spend less time thinking about and dealing with their finances (Figure 2).

Figure 2a shows that 50% of advised clients have low financial stress, compared with 32% of self-directed clients. Conversely, only 14% of advised clients report high levels of financial stress, while nearly twice as many self-directed clients do so. Figure 2b shows that, even for similar stress levels among both advised and self-directed clients, self-directed clients spend more time thinking about their finances.1 These findings highlight that advised clients seem less financially stressed and spend less time thinking about their finances. But how much does advice contribute to their peace of mind and time savings?

How we measure the emotional and time value of advice

The emotional and time value of advice presents many challenges for measurement. Emotions rely on personal perceptions, influenced by many factors (Madamba, Pagliaro, and Utkus, 2020). Similarly, time value involves how much time people spend thinking about their finances, which is also hard to observe, even using administrative datasets (Rossi and Utkus, 2020). The decision to enroll in advice presents a selection issue: Those who signed up for it did so for a reason. This makes it difficult to directly compare those with advice and those without it, as an advised investor may differ in other ways from a self-directed one.

We find that advised investors differ from non-advised ones on some measures such as wealth and age. For example, wealthier clients may have a greater need for advice and be more likely to enroll in it. At the same time, they are likely to have lower levels of financial stress given their higher wealth. On the other hand, an advised investor may have signed up for advice specifically because they were initially more stressed about their finances than someone without advice, so comparing both groups directly would not be appropriate. In an ideal world, we would be able to observe the same client with and without advice to measure the true benefits of advice on emotions and time.

We addressed these important measurement challenges in two ways. First, to get into the minds of clients and capture perceptions of their emotions and time spent on their finances, we deployed our survey to self-directed, human-advised, and digitally advised investors. Second, to try to mitigate confirmation bias, we asked questions to measure people’s current emotions and the time spent on their finances, as well as whether they felt that advice had improved, worsened, or had no effect on those attributes. We classified investors who derive emotional value as those who reported more financial peace of mind compared with managing their finances alone. Similarly, we identified investors as benefiting from the time value of advice if they believe that they spend less time thinking about and dealing with their finances, versus going it alone.

To assess financial stress and time spent on finances in people’s lives and in the workplace, we used metrics from Sergeyev, Lian, and Gorodnichenko (2024). Our measures of emotions are based on the PANAS-X scale (Watson and Clark, 1994). For the overall value of advice, we deployed a mix of Vanguard proprietary measures, including some from our past research on the emotional value of advice (Madamba, Pagliaro, and Utkus, 2020). The Appendix at the end of this article details the measures we used.

Emotional value

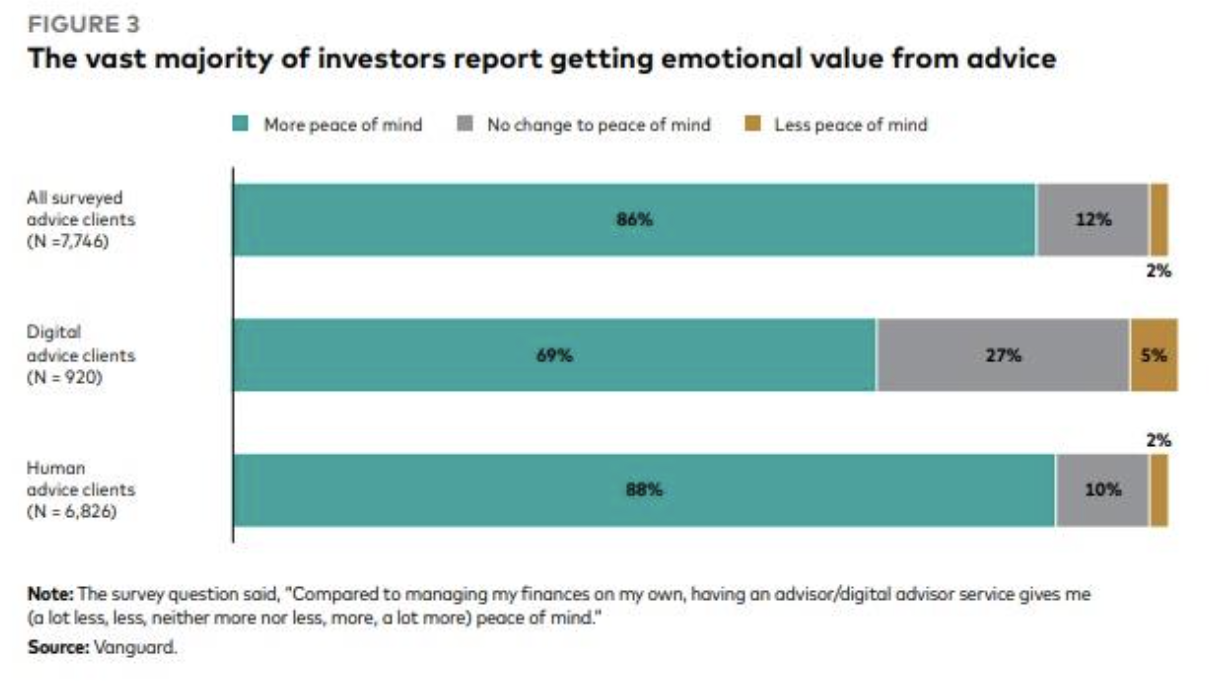

We define the emotional value of advice as the degree to which it provides financial peace of mind to clients. Figure 3 shows the relationship between peace of mind and advice. We found that 86% of advised clients reported having more peace of mind compared with managing their own finances. An additional 12% reported no change to their level of peace of mind. Among clients with a human advisor, 88% reported more peace of mind compared with managing their own finances. For those using a digital advisor, 69% experienced significant increases in peace of mind, highlighting digital advice’s potential for also providing that value.

Previous work by Vanguard shows that the emotional attributes that clients derive from human and digital advice options may also differ. For human advice, value is mostly derived from a client’s relationship with their financial advisor. For digital advice, the key attributes are the need for transparency — visibility of portfolio changes, constant plan monitoring, round-the-clock and online account access, as well as trust and being on track to meet goals, along with empowerment: a feeling of control over finances, an awareness of fees, and a feeling that there is a path to financial freedom (Madamba, Pagliaro, and Utkus, 2020).

Our survey also focused on how clients’ emotions regarding their finances have changed since they enrolled in advice. We divided emotions into two categories: self-focused emotions and social emotions. Self-focused emotions entail someone’s own feelings about their finances. Social emotions involve how a person feels while interacting with their human or digital advisor. Figure 4, below, shows both the proportion of investors who said their positive emotions have increased since getting advice and the proportion who said their negative emotions have decreased.

Figure 4a highlights two results. First, many digital- and human-advised clients reported significant improvement in their emotional state since they started working with an advisor or digital advisor service. Overall, 71% of human-advised clients and 47% of digitally advised clients reported an increase in positive self-focused emotions: confident, satisfied, positive, secure, and proud. The effect was even stronger for negative emotions, with 79% of human-advised clients and 57% of digitally advised clients reporting a reduced prevalence of these emotions: anxious, overwhelmed, worried, sad, and disappointed. Second, we found that human-advised clients were more likely to report improved emotions about their finances, consistent with previous findings about the differences in human versus digital advice (Costa and Henshaw, 2022; Greig et al., 2024).

For social emotions, Figure 4b showcases three key findings. First, as with Figure 4a, advised investors are more likely to report benefits in the form of a lower level of negative emotions, such as shame and anxiety, versus a higher level of positive emotions, such as respect and support. Second, digital advice does well in helping clients to not feel anxious, stressed, ashamed, frustrated, or confused. For example, 85% of digitally advised clients report not feeling ashamed when interacting with the service. This is consistent with previous work showing the importance of empowerment for digitally advised clients (Madamba, Pagliaro, and Utkus, 2020).

Overall, our findings show that clients believe that financial advice enhances their peace of mind, highlighting the emotional value delivered. We find that human advice increases positive emotions and decreases negative ones, while digital advice mostly decreases negative emotions. Finally, both types of advice show stronger results in decreasing clients’ negative emotions about their finances.

Time value

We define the time value of advice as reducing the number of hours thinking about and dealing with financial matters. On average, American workers spend 7.7 hours per week thinking about and dealing with financial issues (Sergeyev, Lian, and Gorodnichenko, 2024; Yakoboski, Lusardi, and Hasler, 2020). In comparison, our survey shows that Vanguard investors spend on average 4.3 hours per week, with advised investors spending 3.8 hours per week and self-directed ones spending 5.5 hours per week.2

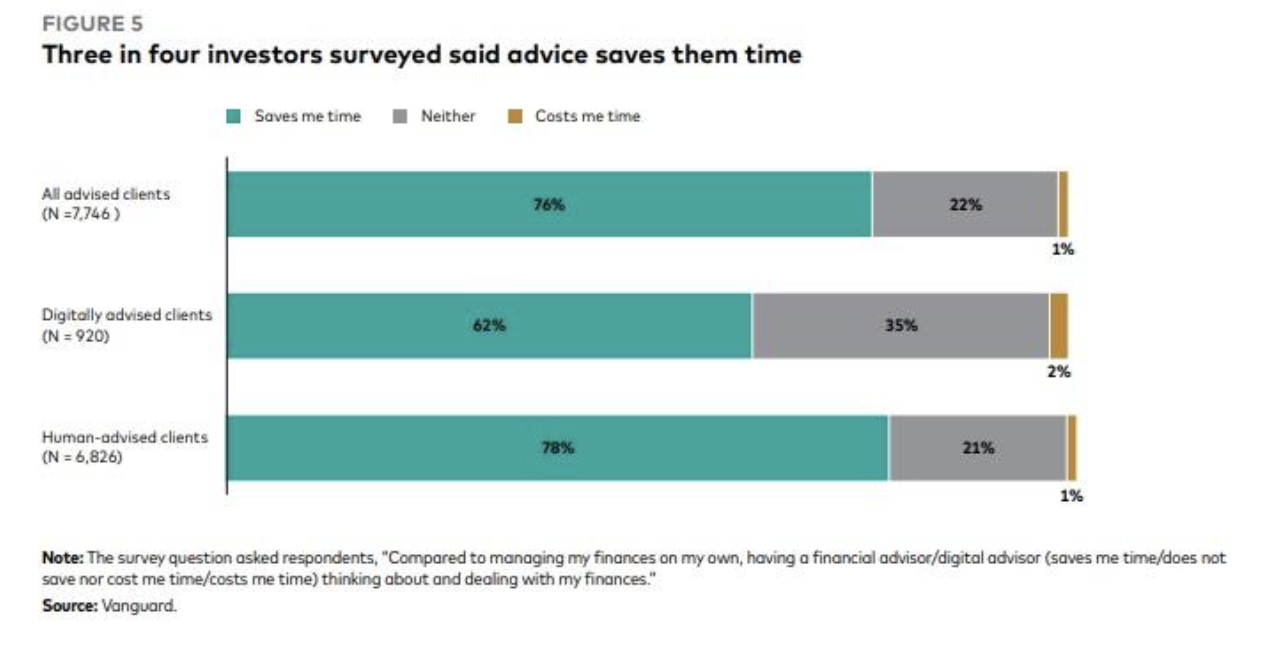

Our survey sought to answer whether having a human advisor or using a digital advice service saves an investor time (Figure 5) and, if so, how much?

In the survey, 76% of our advised clients reported that having an advice service saves them time. These clients further reported a median time savings of approximately two hours per week (or over 100 hours per year). Overall, 22% reported that having advice neither saves them time nor costs them time. And the share of clients who said advice saves time was higher for those who work with a human advisor (78%) than for those using digital advice (62%).

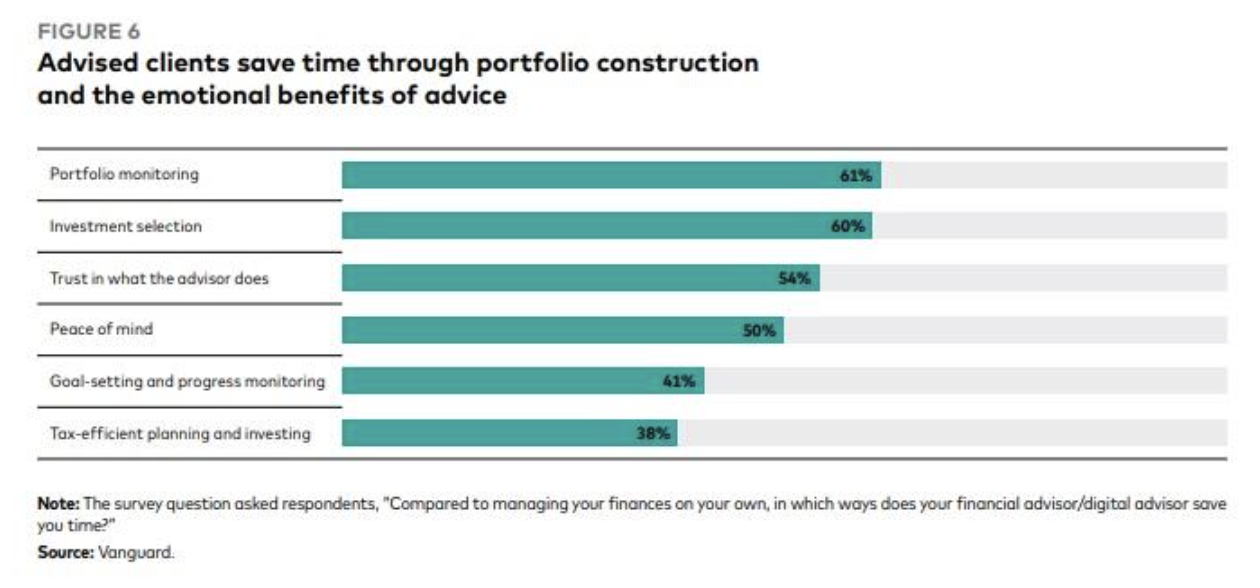

Understanding how financial advice saves clients’ time is important, both for advisors who’d like to know how they’re being most helpful to clients and for plan sponsors who could benefit from fewer financial distractions in the workplace and higher worker productivity. Going back to Vanguard’s framework on advice, we asked clients in which activities advisors saved them time, including two options each for portfolio construction (portfolio monitoring and investment selection), emotional value (peace of mind and trust in the advisor), and financial planning (goal-setting and progress monitoring, and tax-efficient planning and investing.) Figure 6 shows the results.

Most clients find that their time savings come from portfolio monitoring, investment selection, and the trust in what the advisor or digital advisor service does. Half of the clients surveyed say peace of mind also helps them save time. Finally, about 40% of clients report saving time through goal-setting and progress monitoring as well as tax-efficient planning and investing. These findings highlight that while portfolio construction activities are important for clients, the emotional benefits of advice themselves help clients save time as well.

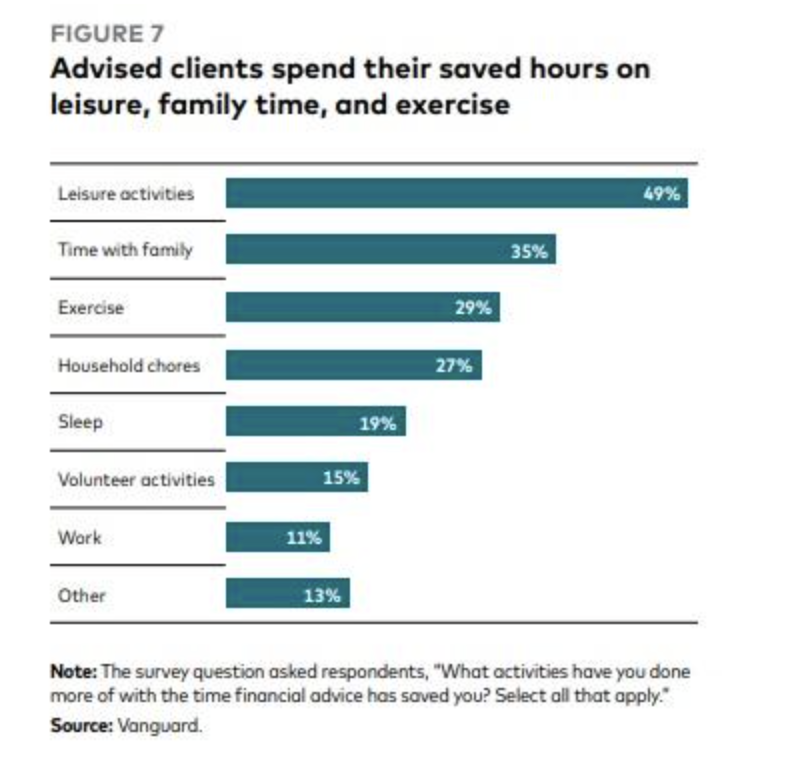

We also asked the survey respondents what they do with this extra time (Figure 7). Almost half of them (49%) reported engaging in leisure activities. Other top responses included time with family (35%), exercise (29%), and household chores (27%). These activities are likely to improve the well-being of clients beyond just financial well-being (Statman, 2018).

Does the emotional and time value of advice matter for investors?

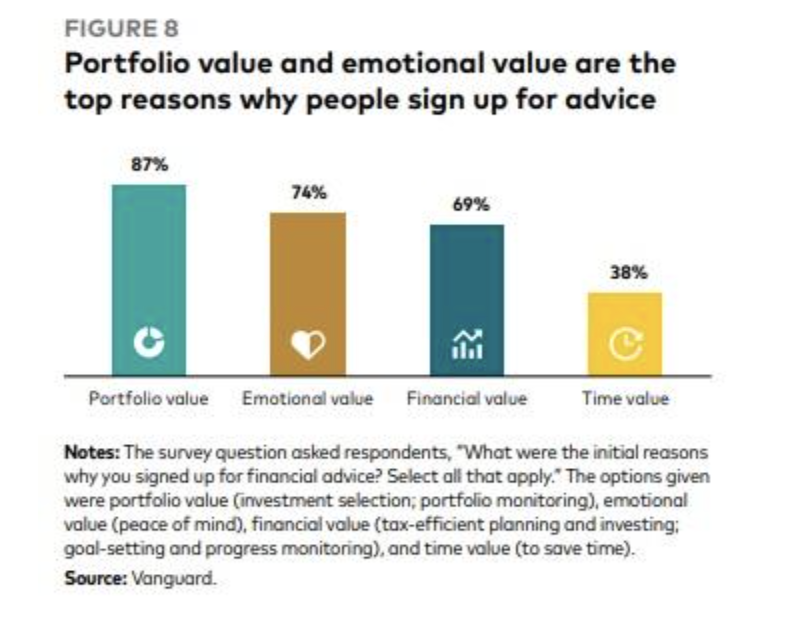

As we mentioned earlier, the financial advice industry has focused primarily on money management as the key measure of its value. One pertinent question is whether clients agree with that. To test this hypothesis, we asked clients their initial reason for signing up for advice (Figure 8).

Investors are most likely to consider the value of portfolio construction expertise received from the service when initially signing up for advice. Among clients surveyed, 87% considered portfolio value when choosing to enroll. Other types of value from advice, though, also play a role in the decision. When signing up, 74% of clients considered the emotional value or peace of mind they would gain from advice, 69% considered whether advice would help them reach their financial goals, and 38% considered whether advice would save them time.

Given our previous findings on how many clients report benefiting from the emotional and time value of advice, we have two observations: First, emotional value is an important reason why clients sign up for advice in the first place. Then, once clients are getting advised, 86% of them say that advice gives them peace of mind — so even clients who did not consider peace of mind as a key reason for signing up end up benefiting from it. Second, the time-saving aspect of advice isn’t top of mind for clients when enrolling. However, 76% of clients say advice saves them time, showing that some of the benefits of advice are not anticipated by clients when signing up.

The cost of distractions at work caused by financial stress

Financial stress may affect workplace performance by distracting employees, leading to diminished productivity (Kaur et al., 2025). We estimated the costs of such distraction.

In our sample of 2,817 plan participants, investors spend an average of 3.8 hours per week distracted by their financial stress while at work. Given that Vanguard keeps anonymized records of participants’ salary information, we estimate in our sample that financial stress costs $5,950 to $6,775 (or, on average, $6,362) per year per worker in productivity.3

But this estimate masks substantial heterogeneity. About 57% of the investors surveyed (1,618) reported being distracted 6.7 hours per week, while the remaining 43% (1,199) reported no financial distractions in the workplace. For the workers reporting financial distractions, we estimate that financial stress costs them $10,450 to $11,700 (or on average $11,077) per year per worker in productivity (Figure 9).

Does advice help reduce work distraction caused by financial stress?

Financial advice may help increase productivity by reducing the hours that employees are distracted in the workplace. Our survey asked workers whether advice helps reduce their financial stress and, if so, by how much.

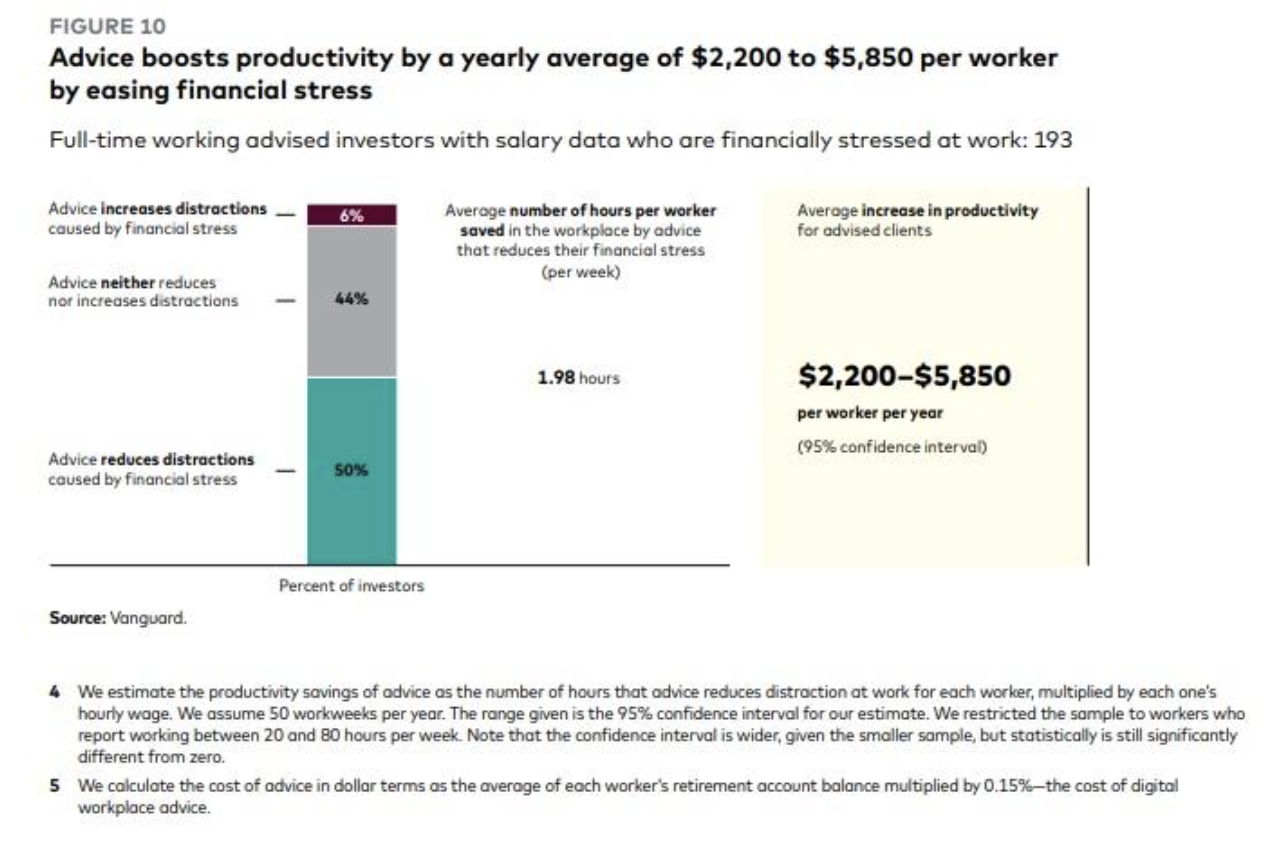

We now focus on the 1,618 respondents who reported being financially stressed in the workplace: 193 of them get financial advice, whereas 1,425 are self-directed investors. On average, advised investors reported fewer hours (5.1 per week) of being distracted by their finances in the workplace, compared with self-directed investors (6.9 per week). But the advised investors may be less stressed for various reasons, only one of them being financial advice.

With this in mind, we asked them whether they believe that advice specifically reduces, increases, or makes no difference to their distraction at work because of financial stress. Among the 193 advised clients who reported being financially stressed, 50% said that advice reduces the number of working hours when that stress distracts them, and the time they reported saving in the workplace averages 4.4 hours per week. Looking at all workers in the sample together, we estimate that advice is associated with an average reduction of 1.98 hours per week (over 100 hours per year) in distractions in the workplace because of financial stress.

Using salary data for the 193 advised clients, we estimate that the reduced distraction at work translates into productivity savings of $2,200 to $5,850 (on average $4,026) per worker per year across all advice clients reporting financial stress.4

Lastly, we compare the estimated productivity savings per year to the yearly cost of workplace digital advice. We estimate that the average cost of workplace advice for these investors, using retirement balance data, is $642 per year — significantly lower than the estimated productivity savings (Figure 10).5

Conclusion

Our survey findings indicate that most investors derive emotional benefits and time-saving value from financial advice. Investors report having more peace of mind and less negative emotions regarding their finances. And the majority of those surveyed say advice saves them time, both in their daily lives and at work. We calculated time savings in their daily lives as a median of two hours per week (over 100 hours per year), which they allocate to other important aspects of their lives, such as leisure, exercise, and time with family. Advised clients also reported being less distracted at work, potentially increasing their productivity.

Before signing up for advice, investors may be underestimating the full range of value that advice provides them. In our survey, 74% of clients initially signed up for the emotional value it provides. Once enrolled, though, 86% of clients report emotional benefits. And only 38% of clients reported considering time savings when signing up, but once clients are using the service, 76% of them report saving time. For financial advisors and investors, it is important to highlight that the benefits of financial advice go beyond portfolio management and financial planning. Emotional benefits and time-saving value are still under appreciated relative to their full potential.

References

American Psychological Association, 2023. Stress in America 2023: A Nation Recovering From Collective Trauma. apa.org/news/press/releases/stress/2023/ collective-trauma-recovery.

Costa, Paulo, and Jane E. Henshaw, 2022. Quantifying the Investor’s View on the Value of Human and Robo-Advice. Vanguard. corporate.vanguard.com/content/dam/corp/ research/pdf/quantifying-the-investors-view-onthe-value-of-human-and-robo-advice.pdf.

Gennaioli, Nicola, Andrei Shleifer, and Robert Vishny, 2015. Money Doctors. The Journal of Finance 70(1): 91–114.

Greig, Fiona, Tarun Ramadorai, Alberto G. Rossi, Stephen P. Utkus, and Ansgar Walther, 2024. Human Financial Advice in the Age of Automation. SSRN.com. papers.ssrn.com/sol3/papers. cfm?abstract_id=4301514.

Kaur, Supreet, Sendhil Mullainathan, Suanna Oh, and Frank Schilbach, 2025. Do Financial Concerns Make Workers Less Productive? The Quarterly Journal of Economics 140(1): 635-689.

Kim, Hugh Hoikwang, Raimond Maurer, and Olivia S. Mitchell, 2016. Time Is Money: Rational Life Cycle Inertia and the Delegation of Investment Management. Journal of Financial Economics 121(2): 427–447.

Madamba, Anna, Cynthia A. Pagliaro, and Stephen P. Utkus, 2020. The Value of Advice: Assessing the Role of Emotions. Vanguard.

Rossi, Alberto G., and Stephen P. Utkus, 2020. The Needs and Wants in Financial Advice: Human Versus Robo-Advising. SSRN.com. download.ssrn. com/21/01/03/ssrn_id3759041_code2149062.pdf

Rossi, Alberto G., and Stephen P. Utkus, 2024. The Diversification and Welfare Effects of Robo-Advising. Journal of Financial Economics 157 (Issue C).

For plan sponsors and consultants, the findings also emphasize the impact of the emotional and time benefits on employees’ overall well-being and productivity. We find that distraction at work due to financial stress is an important issue for workers. In fact, we estimate that the loss in productivity because of financial distraction per worker per year is economically significant for firms. Advice helps workers to be less stressed in life and less distracted at work. By recognizing and promoting these benefits, plan sponsors can better support their employees’ overall well-being and productivity.

Our findings demonstrate that financial advice offers significant value beyond traditional portfolio construction and financial planning interventions. The peace of mind and time savings that clients experience should be integral measures when assessing the value of financial advice, because they can enhance clients’ quality of life.

Sergeyev, Dmitriy, Chen Lian, and Yuriy Gorodnichenko, 2024. The Economics of Financial Stress. The Review of Economic Studies. academic.oup.com/restud/advance-article/ doi/10.1093/restud/rdae110/7900971.

Statman, Meir, 2018. Well-Being Advisers. SSRN.com. papers.ssrn.com/sol3/papers. cfm?abstract_id=3142039.

Watson, David, and Lee Anna Clark, 1994. The PANAS-X: Manual for the Positive and Negative Affect Schedule — Expanded Form. University of Iowa. iro.uiowa.edu/esploro/outputs/other/ThePANAS-X-Manual-for-the-Positive.

Weber, Stephen M., Paulo Costa, Bryan Hassett, Sachin Padmawar, and Georgina Yarwood, 2022. The Value of Personalized Advice. Vanguard. institutional.vanguard.com/content/dam/inst/ iig-transformation/insights/pdf/2022/value-ofpersonalized-advice.pdf.

Yakoboski, Paul J., Annamaria Lusardi, and Andrea Hasler, 2020. The 2020 TIAA Institute-GFLEC Personal Finance Index: Many Do Not Know What They Do and Do Not Know. TIAA Institute. tiaa.org/public/institute/publication/2020/2020- tiaa-institute-gflec-personal-finance-index.

Appendix

Measurements used in the survey Our survey used metrics available in published literature, including financial stress and its consequences, in addition to proprietary strategies to try to estimate perceptions of counterfactuals for advised clients.6

Financial stress

We used the following question from Sergeyev, Lian, and Gorodnichenko (2024): “On a scale from 1 to 10, how concerned are you about your current financial situation? 1 represents the lowest level of concern, and 10 represents the highest level of concern.”

Consequences of financial stress

We used two questions from that same paper regarding how much time people spend thinking about their finances broadly in their lives and how much time they are distracted by the subject during work hours:

- Time spent on finances: “In a typical week, how many hours do you spend thinking about and dealing with issues related to your household’s finances?”

- Time distracted at work because of financial stress: “In a typical week, how many working hours are you distracted by your financial stress?”7

Endnotes

1 Financial stress and time spent on finances may correlate with other household characteristics, such as income and levels of financial assets. Using regression models — and controlling for household income, financial assets, debt type, and other demographics — we find that for every one-point increase in financial stress, advised clients report an additional 0.4-hour increase in time spent on finances, compared with a 0.6-hour increase for self-directed clients. The lower effect of financial stress for advised clients provides suggestive evidence that advice may mediate the effect of financial stress on its consequences, such as time spent on finances.

2 This lower time spent on finances for Vanguard clients was expected, as Vanguard clients are investors by definition and therefore likely wealthier than the average American.

3 Productivity loss is calculated as the hours per week that each worker is distracted, multiplied by their hourly wage. We assumed 50 workweeks per year. The range given is the 95% confidence interval for our estimate. We restricted the sample to workers who reported working between 20 and 80 hours per week.

4 We estimate the productivity savings of advice as the number of hours that advice reduces distraction at work for each worker, multiplied by each one’s hourly wage. We assume 50 workweeks per year. The range given is the 95% confidence interval for our estimate. We restricted the sample to workers who report working between 20 and 80 hours per week. Note that the confidence interval is wider, given the smaller sample, but statistically is still significantly different from zero.

5 We calculate the cost of advice in dollar terms as the average of each worker’s retirement account balance multiplied by 0.15% — the cost of digital workplace advice.

6 Our survey also covered questions about emergency savings; those results will be published in a separate piece.

7 Our survey was deployed to U.S.-based investors the week following the July 4 holiday. For that reason, we slightly adjusted the wording of the questions compared with Sergeyev, Lian, and Gorodnichenko (2024). Instead of the phrase “Over the past week” used in that paper, we changed it to “In a typical week,” given our survey’s proximity to the holiday

Paolo Costa, Ph.D., is a senior behavioral economist with Vanguard’s Investment Strategy Group. Marsella Martino and Malena de la Fuente, Ph.D., are Vanguard investment strategy analysts.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Paulo Costa, Marsella Martino, Malena de la Fuente

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All