DWS, through its lineup of Xtrackers ETFs, has a 20-year history of delivering unique investment solutions featuring competitive expense ratios. Among its top funds are two that provide different angles on the MSCI EAFE Index: the $8 billion Xtrackers MSCI EAFE Hedged Equity ETF (DBEF) and the $2 billion Xtrackers MSCI EAFE High Dividend Yield Equity ETF (HDEF). While the former offers an investment exposure to the EAFE index that mitigates moves in currencies, HDEF tracks a version of the index that tilts toward quality companies that have maintained higher dividend yields.

These two funds are characteristic of the Xtrackers lineup. The issuer offers a wide range of passively managed ETFs that provide exposure to non-U.S. equity markets, usually as alternatives to plain-vanilla index products. Xtrackers offers a suite of additional currency-hedged ETFs, offering exposure to the eurozone (DBEZ), European Union (DBEU), Japan (DBJP), emerging markets (DBEM), and All World ex-U.S. (DBAW). Other Xtrackers ETFs target different slices of non-U.S. markets based on factors, responsible investing, or themes.

However, more recently, it is the international developed space that has been getting more attention from investors, especially after demonstrating strong outperformance relative to the United States year-to-date. DWS Senior Portfolio Strategist Jason Chen explained in a recent interview why investors may find the region appealing.

Why is the market environment favoring international stocks so much this year?

For some time now, there has been a growing valuation gap between U.S. equities and developed and emerging international equity markets. This historically large valuation differential coming into the year reflected a far less demanding earnings outlook for international developed companies as compared to their U.S. counterparts. Conversely, near-historically expensive valuations in the U.S. reflected outsized optimism around corporate earnings; in particular, a sanguine outlook around technology-related growth. Furthermore, there is an increasing recognition among investors that the magnitude of concentration among the Magnificent Seven has reached historical proportions. Even with a positive outlook on these seven stocks, investors need to be aware of the disproportionate risk they contribute to an overall portfolio.

However, a significant valuation gap alone is not typically enough to change investors’ attitudes toward these respective equity regions. Thus far this year, positive momentum in international developed markets has been driven by optimism around European fiscal spending related to infrastructure and defense spending, as well as other potential fiscal stimulus packages. In the U.S., on the contrary, investors are voicing increasing concerns about the accumulating deficit, which may limit fiscal flexibility for U.S. policymakers, particularly as real interest rates remain elevated.

In Japan, significant progress has been made in the multiyear reflationary efforts by the Japanese government and the Bank of Japan to stimulate wages, inflation, and economic growth after three decades of secular stagnation. As a result, positive trends across prices and wage negotiations have slowly but gradually aided a shift in consumption and investment behavior by Japanese households.

These diverse trends across different international markets, combined with the demanding risk premia and significant concentration risk in the U.S. equity market, create a backdrop that argues for a potentially strong positive relative performance from international equities, which could continue to close the sizable valuation gap relative to the U.S.

Europe has performed quite well compared to the U.S., as you’ve mentioned. Does it still have some upside from here?

While it’s difficult to predict over the short term, Europe has more positive catalysts relative to the U.S. over the next few years. If you compare the “fiscal impulse” in Europe to the U.S., there is a significant contrast, where the European outlook includes a potentially substantial fiscal stimulus, whereas the U.S. is more likely to enter a multiyear period of fiscal austerity that is necessary after a few years of overspending. This need for more fiscal discipline in the U.S. contrasts not only with Europe, but also with more positive trends across portions of Asia.

In our view, this divergence in economic momentum, combined with the backdrop of relative valuations, paints a more positive macroeconomic picture for Europe than it does for the U.S. And while it sounds overly simplistic, when you see 30%-35% cheaper valuations in Europe relative to the U.S., you don’t have to be right as often if your starting level earnings yield is more forgiving in Europe than it is in the U.S.

Why does the valuation gap between the U.S. and the rest of the world matter? And do you think it’s likely to persist or narrow?

History would indicate that the valuation gap may contract, but history doesn’t necessarily account for trends like the AI dominance we’ve experienced in the last few years. With that in mind, predicting the valuation gap going forward becomes perhaps more challenging than it has been historically. However, even if the valuation gap remains stable, investors are receiving more earnings yield simply by owning stocks at a cheaper valuation. Effectively, by paying less per dollar or euros per unit of earnings, you are getting more “income” per share in international equities than you are in the U.S. It is similar to owning a bond that pays a 7% yield versus a 5% yield. The price of the 7%-yielding bond doesn't necessarily have to outperform for you to be better off relative to the 5% bond.

For international investors, how do currencies impact returns? If currencies are so notoriously difficult to predict, why bother hedging them?

We agree with the premise that predicting currency moves is historically a very difficult task. However, this is precisely the reason we would advocate to hedge currencies when investing internationally. If the volatility and uncertainty around currencies disproportionately impact risk without commensurate return compensation, you should not own that risk.

For currencies in general, there are a few reasons why keeping currency risk in international equities doesn’t make strategic sense.

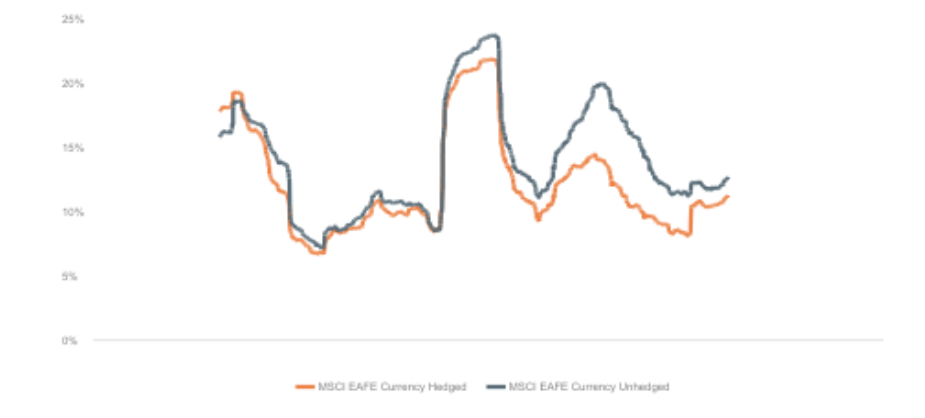

First, currencies are risk-additive — not risk-diversifying — to equities. When a U.S.-dollar-based investor wants to purchase a European stock, for example, they must first exchange their U.S. dollars for euros, creating a 100% long position in the euro. They then have to purchase the equity with the euros, adding another 100% long position in the local equity. The combined 100% currency exposure and 100% equity exposure create mathematical portfolio leverage, which explains why unhedged EAFE equities have historically been more volatile than hedged EAFE equities.

Figure 1. Differential between MSCI EAFE unhedged and local volatility in 5-year increments (12/31/1969 to 3/31/2025)

Source: Bloomberg, DWS Calculations as of 3/31/2025. Past performance is not indicative of future results. It is not possible to invest directly in an index.

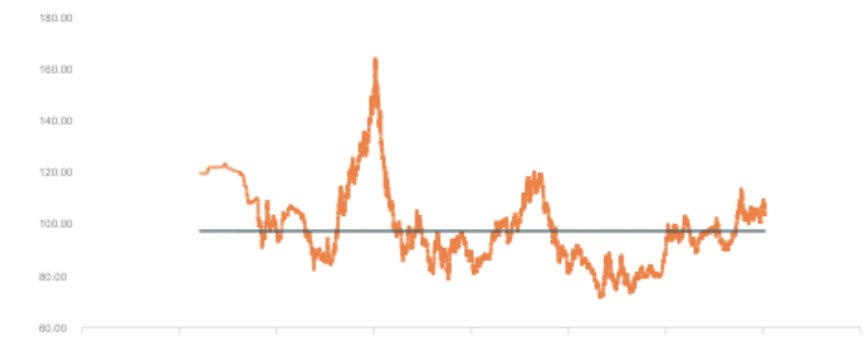

Secondly, this additional source of risk is uncompensated. Over the long term, currencies haven’t generated any material spot return. Since 1967, the US Dollar index (DXY Index) has returned -1 basis point per annum.

Figure 2. US Dollar Index historical spot price (1/31/1967 to 3/31/2025)

Source: Bloomberg as of 3/31/2025. Past performance is not indicative of future results. It is not possible to invest directly in an index.

Not only have currencies historically failed to compensate investors for their risk, there is also no academic basis for expecting risk compensation for currency exposure. To anticipate a positive risk premium for any investment risk, the seller of the risk must be willing to pay the buyer of the risk to appropriately compensate for the willingness to warehouse said risk. This is similar conceptually to an insurance or uncertainty premium. This concept of risk transfer does not apply to currencies in the way it does for equities. For example, an equity issuer is willing to pay an equity buyer a risk premium to transfer some of the risk off of their balance sheet. In contrast, in the currency space, an individual in Europe is unlikely to pay an individual in the U.S. a risk premium to their own detriment to simply get euros off of their individual balance sheet, particularly when their individual liabilities are mostly denominated in euros.

Uncertainty exists across almost all investment risks, but appropriate compensation for assuming a risk is often necessary to justify that risk exposure. If you experience negative equity returns in any given year, you are still accumulating value through accruing risk premia over time. That accrual of risk premia can increasingly help offset the uncertainty over time. However, currencies offer nothing to offset the uncertainty.

When do you not get the risk benefits of currency hedging?

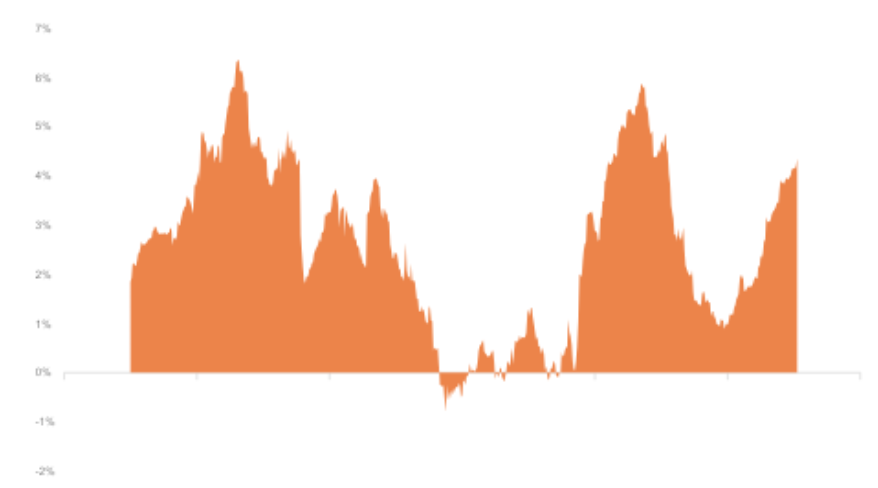

Due to the combined 200% risk (100% from equity and 100% from currency), the MSCI EAFE Currency Unhedged Index experienced roughly 2.8% higher annualized volatility over the last 10 years compared to the MSCI EAFE Currency Hedged Index. Historically, the unhedged index, which includes both 100% of currency risk and 100% of equity risk, realized about 15.1% volatility per annum. In contrast, removing the currency risk and focusing solely on equity resulted in about 12.4% volatility per annum. This represents about a 20% reduction in realized risk.

Figure 3: Rolling 1-year volatility (3/31/2015 to 3/31/2025)

Source: Bloomberg, DWS Calculations as of 3/31/2025. Past performance is not indicative of future results. It is not possible to invest directly in an index.

Due to the leverage math where you have 200% risk, currency only acts as a diversifier or risk reducer if the euro is strongly negatively correlated with European equities. That has rarely happened. Over the long term, you need to realize roughly a negative 0.3 correlation between the euro and European equities to be indifferent to keeping currency risk in a European equity allocation.

For this to occur, whenever the European equities sold off, the euro would have to rally far more often than not. However, this is not how the markets typically operate. Essentially, the dollar would need to behave in a completely opposite manner than it has historically by exhibiting a very strong positive correlation to equity markets that is uncharacteristic of any asset class outside of equities or high yield bonds.

For investors willing to accept currency risk in their portfolio, is an international high dividend strategy a promising alternative?

When considering the composition of developed international equity markets, they tend to feature more mature economies, more stable and cheaper companies, and higher free cash flow yield generation compared to a tech company in the U.S., for example. These are the types of companies held by HDEF, the Xtrackers MSCI High Dividend Yield Equity ETF, which typically have high payout ratios.

These companies generally do not invest as much in capital expenditures and business expansion efforts, allowing them to return much of their generated free cash flow to shareholders. These are precisely the kind of companies you would target if you were seeking income and dividends.

If you compare the dividend yields, the contrast in market composition becomes clear. The S&P 500 typically offers a dividend yield around 1.5%. By shifting to international developed equities with the MSCI EAFE Index, investors are earning something closer to a 3% dividend yield. Overlaying a higher-quality, higher-dividend yield bias to the EAFE universe can further generate a dividend yield in the range of 4.5%-5.0%.

Thank you for your insights, Jason.

Glossary

MSCI EAFE Index: An equity index which captures large and mid-cap representation across Developed Markets countries around the world, excluding the US and Canada. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

MSCI EAFE 100% Hedged to USD Index: Represents a close estimation of the performance that can be achieved by hedging the currency exposures of its parent index, the MSCI EAFE Index, to the USD, the "home” currency for the hedged index.

S&P 500 Index: A stock market index weighted by market capitalization that is made up of 500 of the largest public companies in the United States. It is considered to be one of the best gauges of U.S. equities, the stock market, and the American economy.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Disclosures

The brand Xtrackers represents all systematic investment solutions. Xtrackers ETFs ("ETFs") are managed by DBX Advisors LLC (the "Adviser"), and distributed by ALPS Distributors, Inc. (“ALPS”). The Adviser is a subsidiary of DWS Group GmbH & Co. KGaA and is not affiliated with ALPS. Shares are not individually redeemable, and owners of Shares may acquire those Shares from the Fund, or tender such Shares for redemption to the Fund, in Creation Units only. The brand DWS represents DWS Group GmbH & Co. KGaA and any of its subsidiaries such as DWS Distributors, Inc., which offers investment products, or DWS Investment Management Americas, Inc. and RREEF America L.L.C., which offer advisory services.

www.Xtrackers.com.

Carefully consider the Fund's investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the fund's prospectus, which may be obtained by calling 1-844-851-4255, or by viewing or downloading a prospectus. Read the prospectus carefully before investing.

War, terrorism, sanctions, economic uncertainty, trade disputes, public health crises, and related geopolitical events have led and, in the future, may lead, to significant disruptions in U.S. and world economies and markets, which may lead to increased market volatility and may have significant adverse effects on the fund and its investments.

General Risk: Investing involves risk, including possible loss of principal. Stocks may decline in value. Bond investments are subject to interest rate, credit, liquidity, and market risks to varying degrees. When interest rates rise, bond prices generally fall. Foreign investing involves greater and different risks than investing in U.S. companies, including currency fluctuations, less liquidity, less developed or less efficient trading markets, lack of comprehensive company information, political instability, and differing auditing and legal standards. Emerging markets tend to be more volatile and less liquid than the markets of more mature economies and generally have less diverse and less mature economic structures and less stable political systems than those of developed countries. Funds investing in a single industry, country, or in a limited geographic region generally are more volatile than more diversified funds. Performance of a fund may diverge from that of an underlying index due to operating expenses, transaction costs, cash flows, use of sampling strategies, or operational inefficiencies. There are additional risks associated with investing in high-yield bonds, aggressive growth stocks, non-diversified/concentrated funds, and small- and midcap stocks that are more fully explained in the prospectuses, as applicable. An investment in any fund should be considered only as a supplement to a complete investment program for those investors willing to accept the risks associated with that fund. Please read the applicable prospectus for more information.

DBEM: Special risks associated with investments in Chinese companies include exposure to currency fluctuations, less liquidity, less developed or less efficient trading markets, lack of comprehensive company information, political instability, and differing auditing and legal standards, the nature and extent of intervention by the Chinese government in the Chinese securities markets, and the potential unavailability of A-shares. The U.S. government has imposed restrictions on the ability of U.S. investors to hold and/or acquire securities of certain Chinese companies. To the extent that an Underlying Index includes such a security, and the Fund excludes it, the Fund’s tracking error may increase, and the performance of the Fund and Underlying Index may diverge. Uncertainties in the Chinese tax rules governing taxation of income and gains from investments in A-shares could result in unexpected tax liabilities for the fund, which may reduce fund returns. Any reduction or elimination of access to A-shares will have a material adverse effect on the ability of the fund to achieve its investment objective.

DBAW / DBEF / DBJP: The fund’s use of forward currency contracts may not be successful in hedging currency exchange rate changes and could eliminate some or all of the benefit of an increase in the value of a foreign currency versus the U.S. dollar. Funds investing in a single industry, country, or in a limited geographic region generally are more volatile than more diversified funds. Investing in derivatives entails special risks relating to liquidity, leverage, and credit that may reduce returns and/or increase volatility.

DBEU / DBEZ: The European financial markets have recently experienced volatility and adverse trends in recent years due to concerns about economic downturns or rising government debt levels in several European countries, including Greece, Ireland, Italy, Portugal, and Spain. A default or debt restructuring by any European country would adversely impact holders of that country’s debt, and sellers of credit default swaps linked to that country’s creditworthiness (which may be located in countries other than those listed in the previous sentence). These events have adversely affected the exchange rate of the euro, the common currency of certain EU countries, and may continue to significantly affect every country in Europe, including countries that do not use the euro. Italy, Portugal, and Spain currently have high levels of debt and public spending, which may stifle economic growth, contribute to prolonged periods of recession or lower sovereign debt ratings, and adversely impact investments in the Fund. The Fund’s use of forward currency contracts may not be successful in hedging currency exchange rate changes and could eliminate some or all of the benefit of an increase in the value of a foreign currency versus the U.S. dollar.

HDEF: Foreign investing involves greater and different risks than investing in U.S. companies, including currency fluctuations, less liquidity, less developed or less efficient trading markets, lack of comprehensive company information, political instability and differing auditing and legal standards. If the dividend-paying stocks held by the fund reduce or stop paying dividends, the fund’s ability to generate income may be adversely affected.

MSCI: The funds or securities referred to herein are not sponsored, endorsed, issued, sold, or promoted by MSCI, and MSCI bears no liability with respect to any such funds or securities or any index on which such funds or securities are based. The Prospectus contains a more detailed description of the limited relationship MSCI has with DBX Advisors LLC and any related funds.

Investment products: No bank guarantee I Not FDIC insured I May lose value

ALPS Distributors, Inc., 1290 Broadway, Suite 1100, Denver, CO 80203

© 2025 DWS Group GmbH & Co. KGaA. All rights reserved. 106718-1 (07/25) DBX006758 (07/26)

Read more articles by Special to VettaFi