China’s collapsing investment is as unprecedented as it is hard to explain.

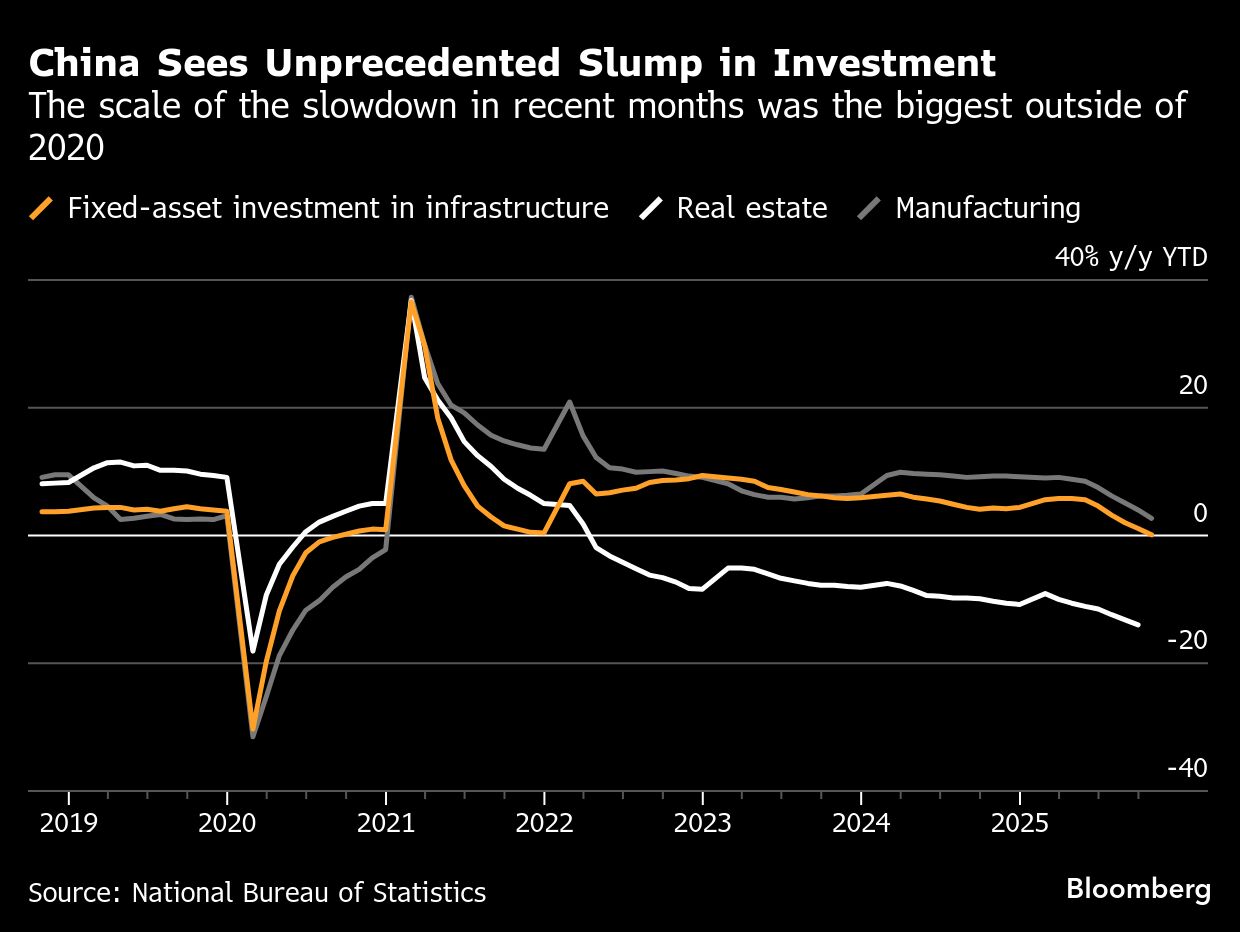

A plunge estimated at more than 11% in October from a year earlier was the worst single-month performance since the initial Covid lockdowns at the start of 2020, official data showed on Friday. A further crash in investment could prove destabilizing by affecting an activity that makes up nearly half of China’s gross domestic product, driving up risks for an economy already coping with a downswing in exports.

And yet economists are still struggling to square the unprecedented contraction with other statistics or to fully decipher its cause.

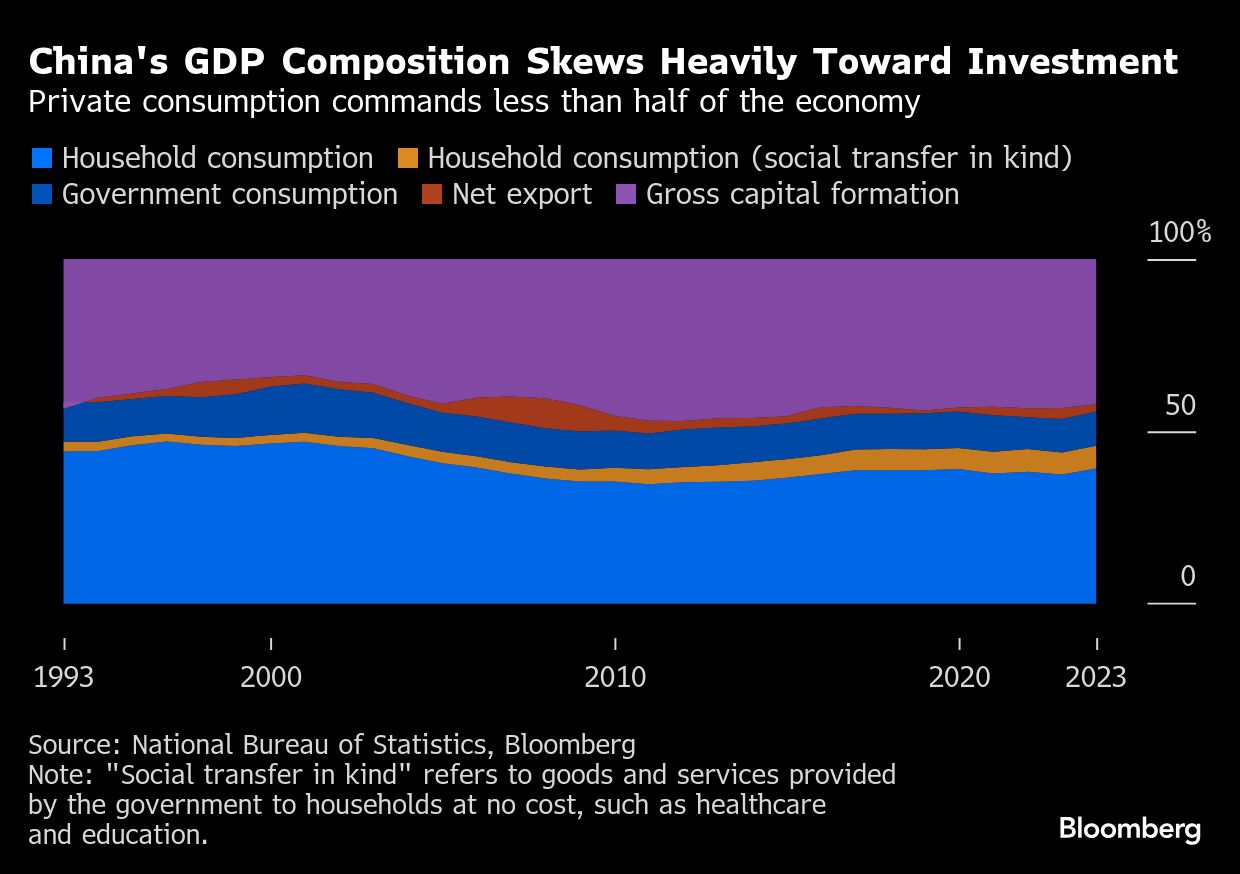

The precipitous slump in fixed-asset investment that began in July has yet to create a serious drag on growth. Gross capital formation, another measure of investment activity, even contributed to almost a fifth of the overall GDP gain in the third quarter.

“We can find some reasons to explain the investment drop, but it’s rather hard to understand how it dropped so much,” said Ding Shuang, chief economist for greater China and north Asia at Standard Chartered Plc. The drag from investment “will be even bigger” in the fourth quarter than in the prior three months, he said, predicting it “will be the most prominent reason for declining GDP growth.”

Adding to the intrigue is the fact that the downturn started at almost the same time as when the government launched a so-called “anti-involution” campaign to drain a glut in output across many industries. Still, it’s difficult to gauge the role played by that policy, since officials have issued no specific targets for restricting investment or capacity.

And though curbing industrial investment would put a lid on excess production, it might also hurt employment and household income in the absence of stimulus.

The slump raises important questions about the health of domestic demand. Even though economists have for years called on the country to shift away from investment toward consumption, the latter remains weak as a painful property downturn persists.

Fixed-asset investment, or FAI, fell by around 6% to 7% throughout the third quarter from a year ago, according to economists’ calculations based on official data. The National Bureau of Statistics only publishes year-to-date figures without breaking out the monthly totals.

In an attempt to explain the discrepancy between the two main measures of investment, the NBS said that the FAI numbers were weighed down by falling prices, while the contribution of gross capital formation reflected growth adjusted for those changes.

In a written response to questions from Bloomberg News, the NBS also pointed to the differences in the scope of the two data sets. FAI includes items that aren’t counted toward gross capital formation, such as fees made to buy land as well as used equipment.

The math doesn’t necessarily add up, according to Adam Wolfe, an emerging markets economist at Absolute Strategy Research.

“The recent contraction in FAI has been too deep and broad-based to be explained away by the statistical differences,” said Wolfe.

He also pointed to the fact that the distress is nowhere near as dire in other areas of the economy, a puzzling fact should the investment slump be as bad as reported. Industrial output expanded 6.1% in the year to date, and retail sales are up around 4% over the same period.

China’s statisticians have long faced questions over the credibility and transparency of their reports, even though authorities in recent years made some headway in addressing them.

At the same time, a number of official and private data series have been halted in recent years, making it more difficult to gauge the real health of the world’s No.2 economy.

FAI is a vestige from the era of the Soviet-style planned economy. For years, this measure of investment outstripped that of gross capital formation, due to problems such as double-counting and falsification.

The gap narrowed in the past few years — evidence that the NBS began to fix the problems and improved the quality of the FAI data, according to Peterson Institute for International Economics.

For all the improvements in the quality of statistics, local officials may now feel motivated to under-report investment data in order to appear diligent in carrying out the “anti-involution” campaign.

It’s likely that actual corporate investment is decelerating and has already been slowing for some time, according to Andrew Batson, China research director at Gavekal Dragonomics. The recent sharp decline in FAI may then be the result of a change to the reporting of the data rather than a shock to actual underlying investment activity, he said before the latest data was released.

There are a few other possible reasons for the recent setbacks in investment.

The property sector has continued to deteriorate, resulting in a bigger decline in real estate investment. Spending on infrastructure also slowed significantly, as local governments focused on repaying their hidden debt and clearing arrears owed to companies.

What’s especially concerning about the slump, however, is the drastic slowdown in manufacturing investment growth, which slid to 2.7% on year in the first 10 months from almost 9% in May.

A breakdown by industry reveals the damage done to some industries targeted by the “anti-involution” campaign — such as electric equipment and machinery, which includes solar panels and batteries. It saw investment fall more than 9% so far this year from a year ago, though its decline began as early as August 2024.

But other sectors targeted by the government crackdown are showing little sign of slowing down. The auto industry, for example, saw investment surge close to 18%.

The questions preoccupying other analysts go beyond the inconsistencies in the FAI and GDP data.

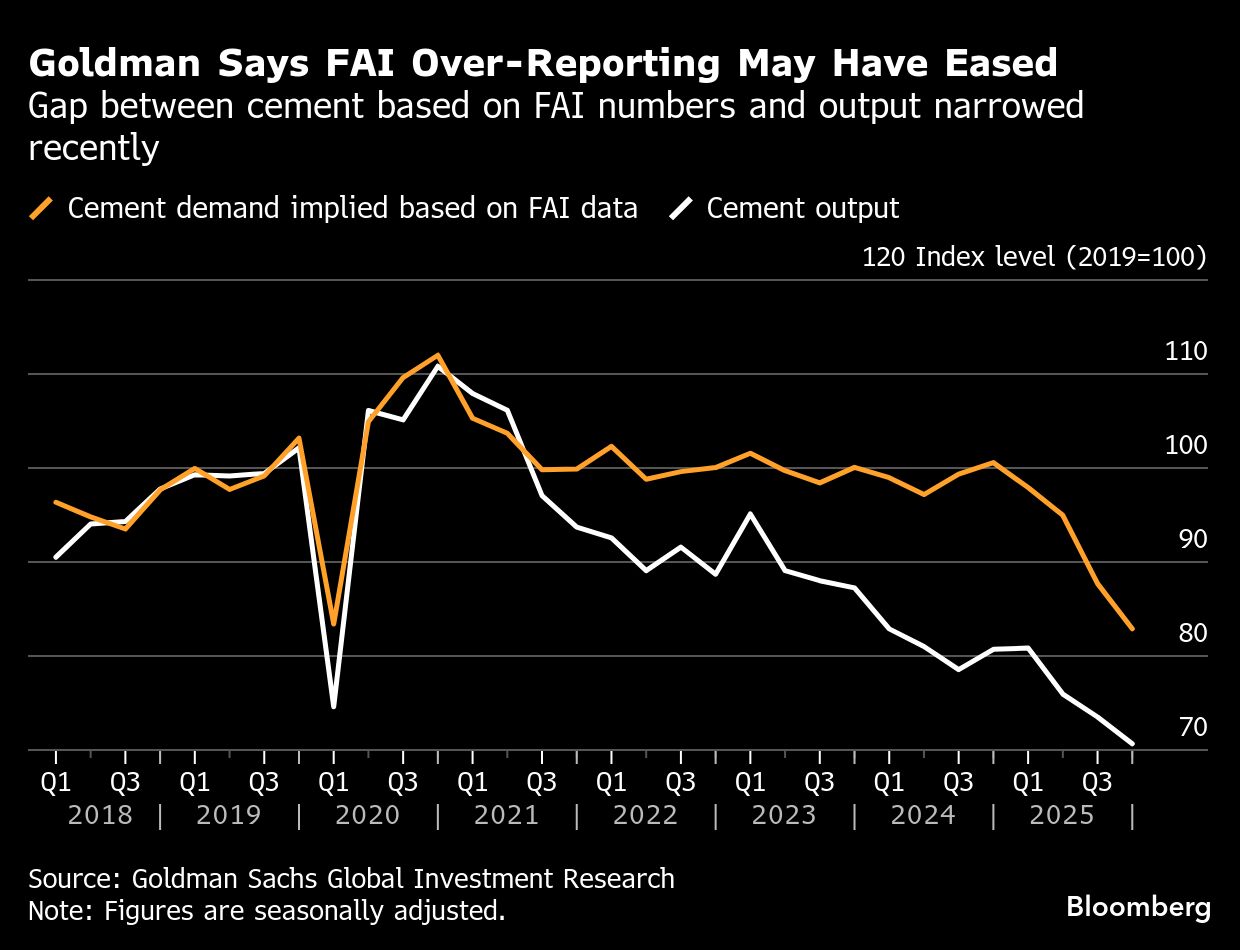

Goldman Sachs Group Inc. economists measured the implied cement demand based on the FAI figures and the actual output of the building material, finding the gap narrowed in the past few months.

This could be a sign that the NBS “may have proactively adjusted FAI data to avoid potential over-reporting,” economists including Lisheng Wang wrote in a Friday report.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by