Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This article was written with the assistance of artificial intelligence. The underlying data, financial arguments, and strategic insights were authenticated by the author, who retains full accountability for the accuracy of the content.

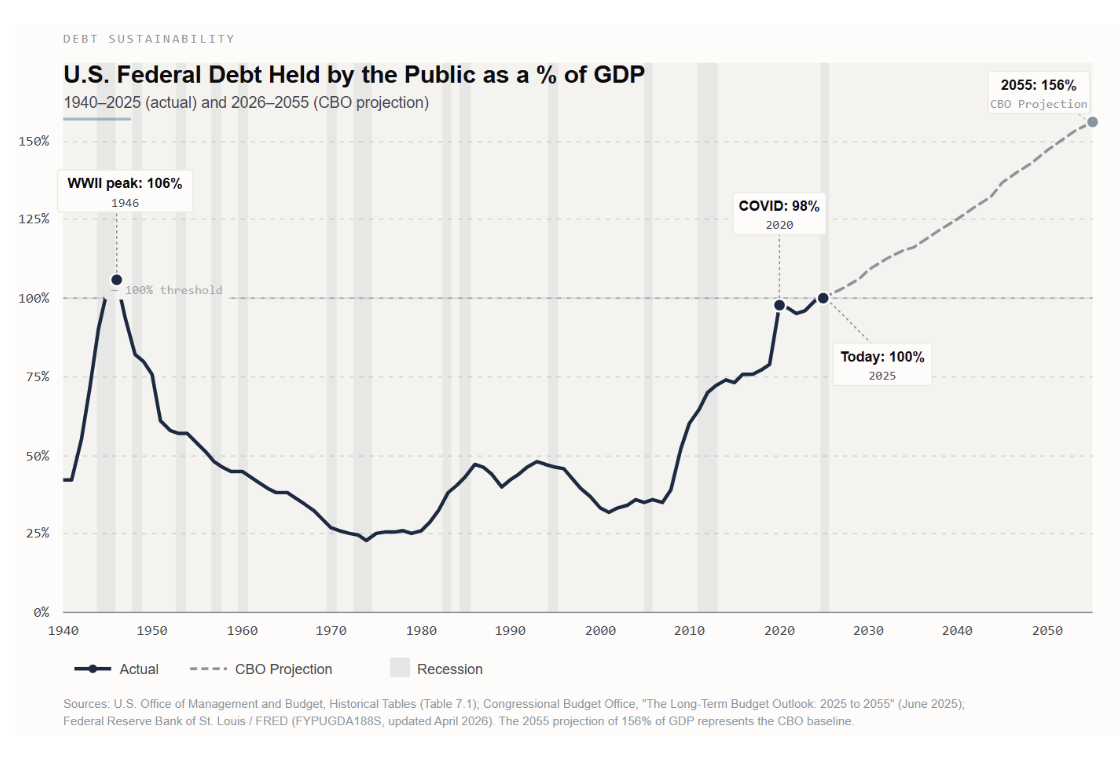

There is one metric that should give every advisor pause: 100%.

That is the current level of U.S. debt held by the public as a percentage of GDP — a threshold not crossed since the aftermath of World War II. The last time the U.S. was here, the country had just mobilized its entire industrial and financial capacity to fight a two-front war against fascism.

The context today could not be more different. The country is not mobilized for global conflict, and despite severe inflationary pressures and recent market turbulence, the domestic economy is still expanding. Our labor market, while facing structural shifts, is not in freefall. That contrast is precisely what makes this moment worth discussing with your clients.

The Absence of Fiscal Normalization

Debt has historically spiked during genuine national emergencies: the Civil War, the Great Depression, WWII, the Global Financial Crisis, and COVID-19.

In each case, borrowing was a response to extraordinary circumstances, and the trajectory eventually reversed as conditions normalized. What is different and genuinely concerning about today is that no such normalization has followed.

U.S. debt is not elevated because of a crisis being managed. It is elevated and still growing during a period of reasonable growth and low unemployment.

The numbers tell the story clearly. Between 2011 and 2025, U.S. public debt grew by 145% while other advanced economies grew their debt by just 17%.

Over that same period, Germany reduced its debt burden from 80% to 63% of GDP. Sweden held its ratio below 35%. Meanwhile, the U.S. added 25 percentage points to its debt-to-GDP ratio. These are not perfect economies, but their governments demonstrated a directional commitment to fiscal normalization that the U.S. government has not.

Net interest payments have now crossed $1 trillion annually, making interest the second largest line item in the federal budget, behind only Social Security and larger than defense, Medicare, and Medicaid individually. Unlike every other budget item, this one cannot be negotiated, deferred, or voted away. It compounds automatically with every dollar of new debt issued.

Perhaps most telling was fiscal year 2019: unemployment was 3.5%, GDP growth was 2.9%, and the annual deficit still approached $1 trillion. It would have been a perfect moment to clean up the balance sheet. Lawmakers didn't. The decision to keep spending during good times was not a failure of economic understanding, it was a deliberate political calculation, delaying accountability for the next Congress, the next president, and the next generation.

When Markets Begin to Notice

Markets are beginning to notice. The U.S. dollar fell approximately 10% in the first half of 2025, its worst performance in over 50 years. What made the move unusual was not its magnitude but its character. Historically, when U.S. markets stumble, investors flood into dollars for safety. In 2025, stocks and the dollar fell together. Investors were not moving money around within the U.S., they were moving it out. Gold hit record highs. Foreign buyers of U.S. debt began demanding higher yields.

These are not signs of a crisis. They are early signs of wavering confidence, and confidence is far easier to maintain than it is to rebuild once lost.

The U.S. retains enormous structural advantages. The dollar remains the world's dominant reserve currency. America's culture of innovation, its dynamic capital markets, and the rise of artificial intelligence represent a genuine productivity opportunity. The generation that came home from WWII reduced debt from 106% of GDP to 23% by 1974, not through painful cuts, but through extraordinary economic expansion. That remains the most plausible path forward.

But the direction of travel matters more than today's snapshot. The CBO projects debt reaching 120% of GDP by 2036 under current law. That trajectory has consequences, both for portfolios and for the conversations you are already having with clients.

Five Takeaways for Advisors

1. Reframe the Conversation from Crisis to Trajectory

When clients ask about the national debt, they are often asking through an emotional lens — fear, frustration, or political anxiety. The honest framing is this: The U.S. is not in a debt crisis, but the direction of travel is unsustainable without structural change.

Your job is to separate the signal from the noise. Clients who understand that this is a slow-moving, manageable structural challenge, not an imminent collapse, are better positioned to stay invested rather than react emotionally.

2. International Diversification Deserves a Fresh Look

For years, U.S. equity dominance made global diversification feel like a drag on performance. That calculus is shifting. The 2025 dollar weakness demonstrated that currency exposure is itself a source of return or loss.

Many client portfolios carry a degree of U.S. concentration they may not fully appreciate. This is a natural moment to revisit the international allocation conversation, not as a hedge against the U.S., but as prudent diversification given where we are in the cycle.

3. Real Assets Belong in the Toolkit

Real estate, infrastructure, and commodities have historically preserved value better during periods of dollar softness and what economists call "financial repression," when real interest rates are kept below real growth to quietly erode the debt burden. That dynamic is partially underway today and is likely to continue.

For clients with long time horizons, real assets are not just an inflation hedge; they are a structural positioning tool for an environment where the government has strong incentives to inflate its way out of a portion of this burden.

4. Be Thoughtful About Duration in Fixed Income

If markets begin demanding a higher risk premium for lending long-term to a heavily indebted government — and there are early signs they already are — long duration bond prices feel that consequence first and most acutely.

Clients who built bond allocations in a low-rate world may be carrying more duration risk than they realize.

This is not a call to abandon fixed income, but it is a reason to think carefully about where on the yield curve clients are positioned and whether that exposure is commensurate with the risk they are being compensated for.

5. Don't Abandon U.S. Innovation

The most important thing advisors can communicate is that concern about fiscal trajectory is not the same as pessimism about America. The specific advantages that make the growth path plausible — technology leadership, dynamic capital markets, and a culture of entrepreneurship — remain intact. Maintaining exposure to those themes is as important as ever.

Rather than de-Americanize a portfolio, the goal is to position it for an environment that is more complex, more volatile, and more global than the one we navigated over the past decade.

Navigating Macroeconomic Anxiety With Proactive Conversations

America has navigated debt at these levels before and grown its way out. The tools exist. What has been missing is political will.

As advisors, our role is not to solve fiscal policy; it is to ensure our clients are positioned to weather the uncertainty that comes from that gap, stay committed to their long-term plans, and not let macroeconomic anxiety drive short-term decisions they will regret.

The conversation about America's tab is one worth having. The good news is that having it proactively, with context and clarity, is one of the most valuable things you can do for a client right now.

Read more by Joe Halpern:

Joe Halpern is managing partner and CIO of Obsidian CIO, a technology-enabled OCIO for RIAs, and is host of the Investment Wars podcast and co-host of the Advisor Wars podcast.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

More Smart Beta Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.