Sentiment in the US stock market has shifted quickly from fear of missing out to fear of getting wiped out.

Traders nervous about a further plunge in US stocks in the coming weeks are loading up on downside protection. That’s pushed the one-month skew, a measure of demand for options to protect against a drop in the S&P 500 Index, from the lowest in a year to a 72nd percentile of observations, according to data compiled by Mandy Xu, head of derivatives market intelligence at Cboe Global Markets Inc.

And sentiment among individual traders appears to have turned more bearish, with put buying making up 27% of all new positions opened by retail traders in Big Tech stocks on Friday, compared with just 15% a week prior.

“Friday’s selloff was meaningful in waking up traders to looming risks in the stock market,” Xu said by phone, referring to that day’s 2.6% drop in the S&P 500 and an almost 4.8% plunge in the Nasdaq 100 Index. “There had been a lack of hedging any downside risks after everyone was chasing the rally. But now we’re seeing a reversal on an index level, which signals investors see the potential for another leg lower in the market.”

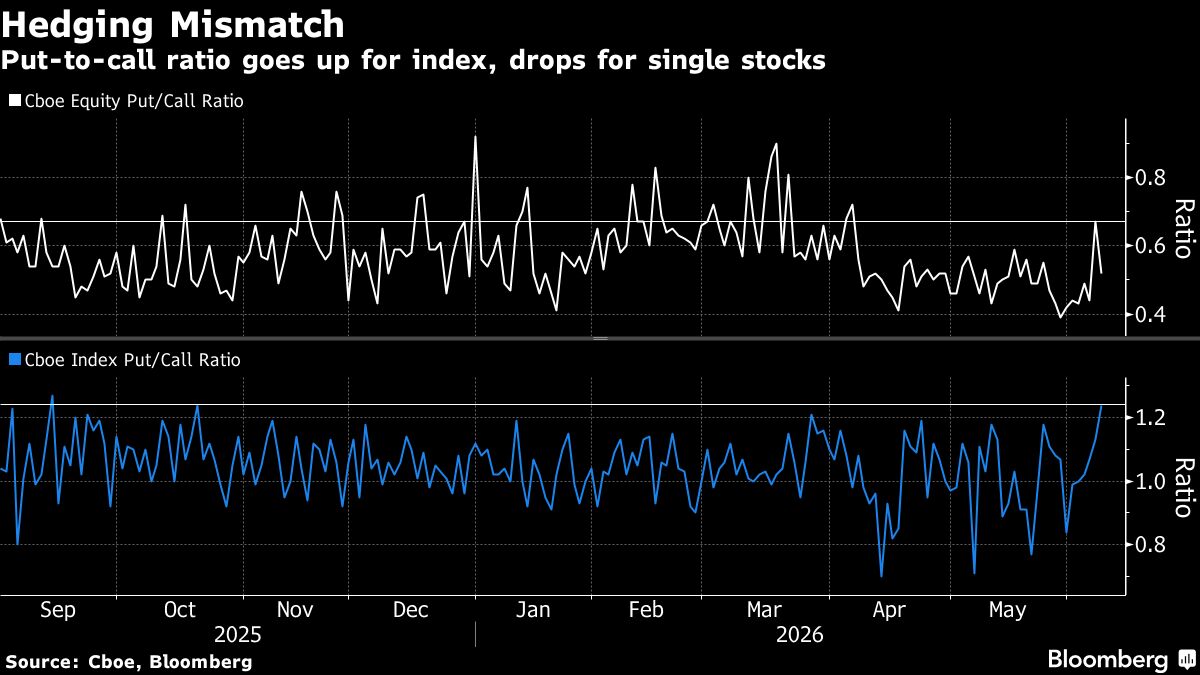

Another sign of increased demand for downside protection can be seen with the Cboe’s index put-to-call ratio, which has risen to match its highest level since September. The opposite has been happening on a single-stock level: Rising demand for index hedging comes as investors have been monetizing hedges on the single-stock level, instead of reaching for more.

Investors who watched the S&P 500 add $9 trillion in market value since its March low have grown uneasy with re-accelerating inflation, elevated crude-oil prices and worries about rising interest rates. Even the Federal Reserve is no longer a source of comfort. With all eyes glued to Wednesday’s consumer prices report, last week’s robust jobs data has put extra focus on the inflation figures as traders speculate the Fed’s next move may be to hike, rather than cut, interest rates.

Warnings of a bubble have been loudest in parts of the market riding the artificial-intelligence wave, where many of the Magnificent Seven megacaps and chipmakers have delivered strong returns. Instead of ditching those winners, investors have bid up protection for a marketwide downturn.

FOMO-driven traders keep chasing technology shares, and that odd divergence between the skew of single-stock versus indexes may, in turn, keep the broader rally chugging along — for now — amid higher volatility for single stocks.

“People are much more focused on hedging at the index level while looking for upside in single-name stocks if they still want exposure to market winners,” Xu added.

Contracts protecting against a 10% decline over the next month in the SPDR S&P 500 ETF Trust, or SPY — the largest exchange-traded fund tracking the broad equities index — briefly rose to the highest since early April relative to the cost of contracts hedging against a similar-sized rally.

Owning index protection in either the SPY or the Invesco QQQ Trust exchange-traded fund, the largest ETF tracking the tech-heavy Nasdaq 100, is one of the better risk-reward opportunities at a macro equity level right now, according to Alexander Altmann, global head of equities tactical strategies at Barclays Plc.

Correlation among individual stocks remains low even after Friday’s selloff, so buying index protection “still makes sense,” Altmann said.

“We’ve been turning more cautious the past few weeks because the risk-reward for owning equities is beginning to deteriorate,” Altmann said by phone, adding that the attractiveness of index puts is too strong to ignore currently. “So buying protection with index hedges still makes sense. We’re not out of the woods yet.”

For now, an increase in investor angst remains relatively confined to the near term following a nearly 3% dip in the S&P 500 from its last record on June 2. While the S&P 500’s options skew is indeed climbing, it is still well below the level seen during the market’s March swoon.

To Chris Murphy, co-head of derivatives strategy at Susquehanna International Group, the case for adding hedges toward the end of the summer is growing more compelling because the setup is “starting to look increasingly vulnerable” to a correlation shock after a strong run.

He said clients have been hedging this week on an index level more than they had been in prior weeks, though they have been maintaining bullish positioning at a more company specific level on the mega-cap tech names and the Magnificent Seven tech companies.

“The concern isn’t hedging against AI stocks,” he added. “It’s fears about higher interest rates.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click hereto register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.