Ratings that underpin a growing slice of the $1.8 trillion private-credit market, the hottest corner of Wall Street in recent years, are systematically understating investment risk, according to a new study by Columbia Business School researchers.

The finding, in a paper posted online this month and not yet peer-reviewed, adds to concerns about perils lurking in the US life insurance industry. Carriers are piling up bets on private credit, fueling a bonanza for the financiers who create the products, while leading regulators and analysts to warn of potential risks for policyholders.

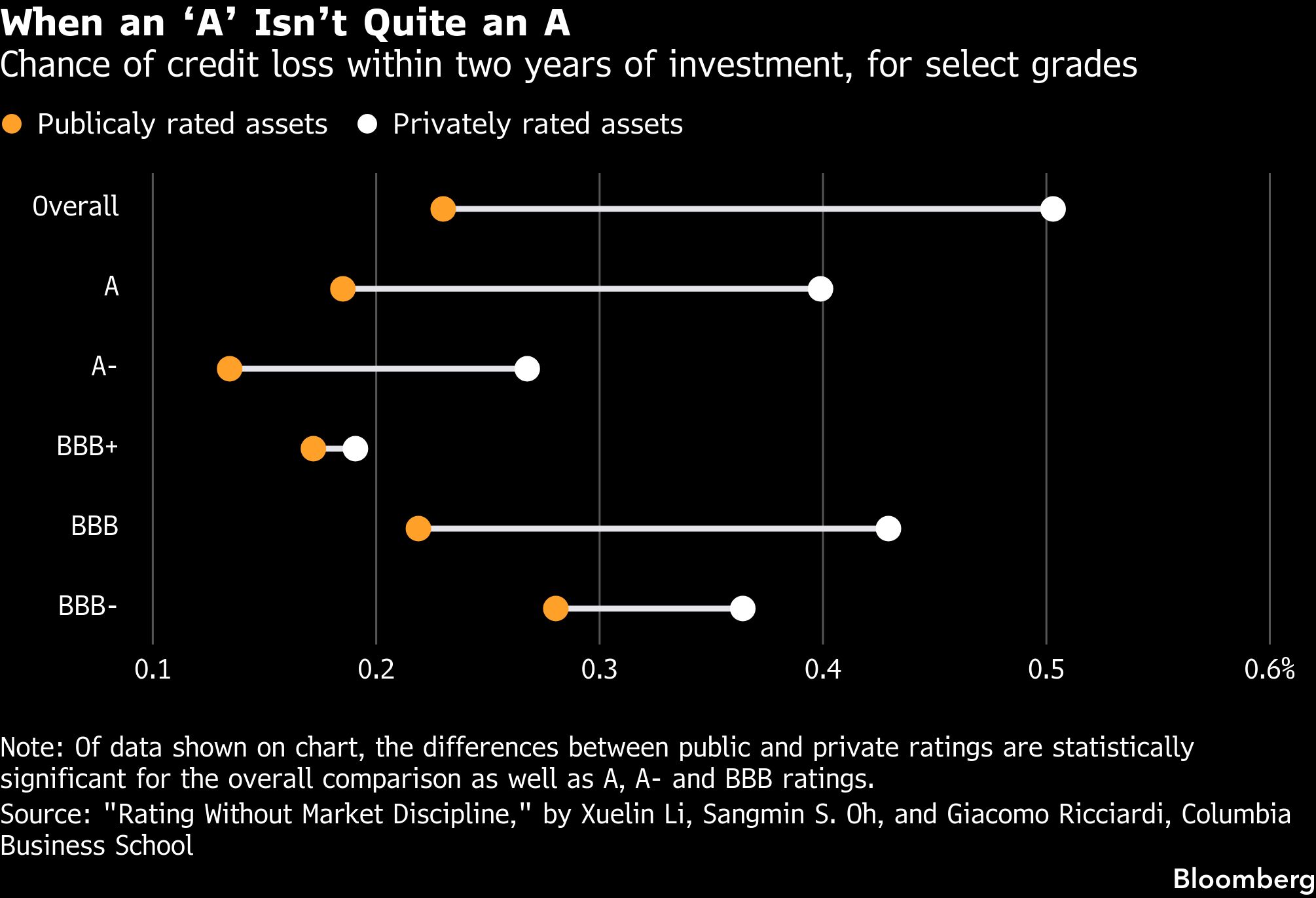

The study focuses on so-called private-letter ratings, which aren’t widely disseminated the way traditional public ratings are. Assets bearing a private rating are about twice as likely to incur a credit loss as debt assigned the same grade in a public rating, according to the paper from Xuelin Li, Sangmin S. Oh and Giacomo Ricciardi. The unexpectedly high loss rates — while below 1% — were in relatively benign years.

Put differently, private ratings are two to three notches higher than public ratings with the same underlying impairment risk, the researchers found. That means a bond with a private BBB rating, one of the lowest investment grades, is about as likely to suffer a loss as one with a public rating of BB+ or BB, which is below investment grade.

“For many, many years we have taken this credit rating system as a given,” said Oh, an assistant professor at Columbia, in an interview. “A lot of regulation and investor decisions depend on the credit-rating system being accurate when it comes to measuring and assessing risks.”

Most private ratings used by life insurers come from three ratings firms: Egan-Jones Ratings Co., Kroll Bond Rating Agency and Morningstar DBRS. The data used in the study doesn’t identify which firms rated credits that suffered losses.

KBRA and Morningstar said they apply the same standards and methods for ratings whether they’re public or private, and that both types have a good track record. Morningstar added that the Columbia paper contains “egregious errors and assumptions” and called its conclusions “severely flawed.”

The paper lumps all ratings firms together and doesn’t account for differences among them, Richard Sibthorpe, Morningstar’s head of investor strategy, added in an interview.

Egan-Jones declined to comment.

Ratings play a crucial role in the portfolios of US insurers. To make sure they’ll have enough money to honor promises that can stretch decades into the future, carriers are required to hold mostly safe assets. For years, the industry focused primarily on plain-vanilla investment grade corporate bonds, which typically had public ratings.

But in recent years, alternative asset managers acquired and built up insurance affiliates, leading the industry ever-deeper into more complex investments, including privately rated debt.

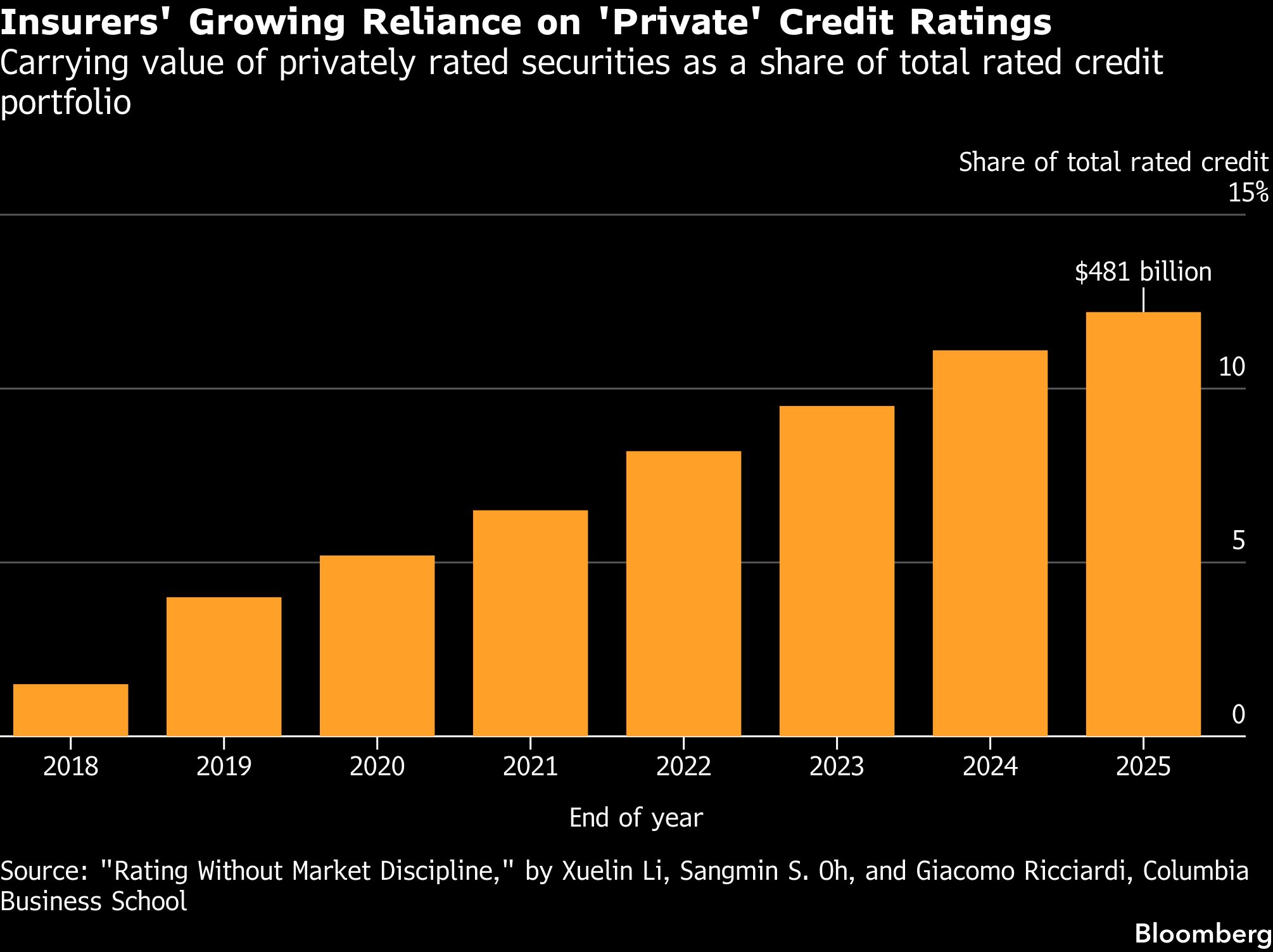

Life insurers’ privately rated assets totaled about $481 billion, or about 12% of their rated credit portfolio at the end of last year, the researchers said, up from less than 2% in 2018.

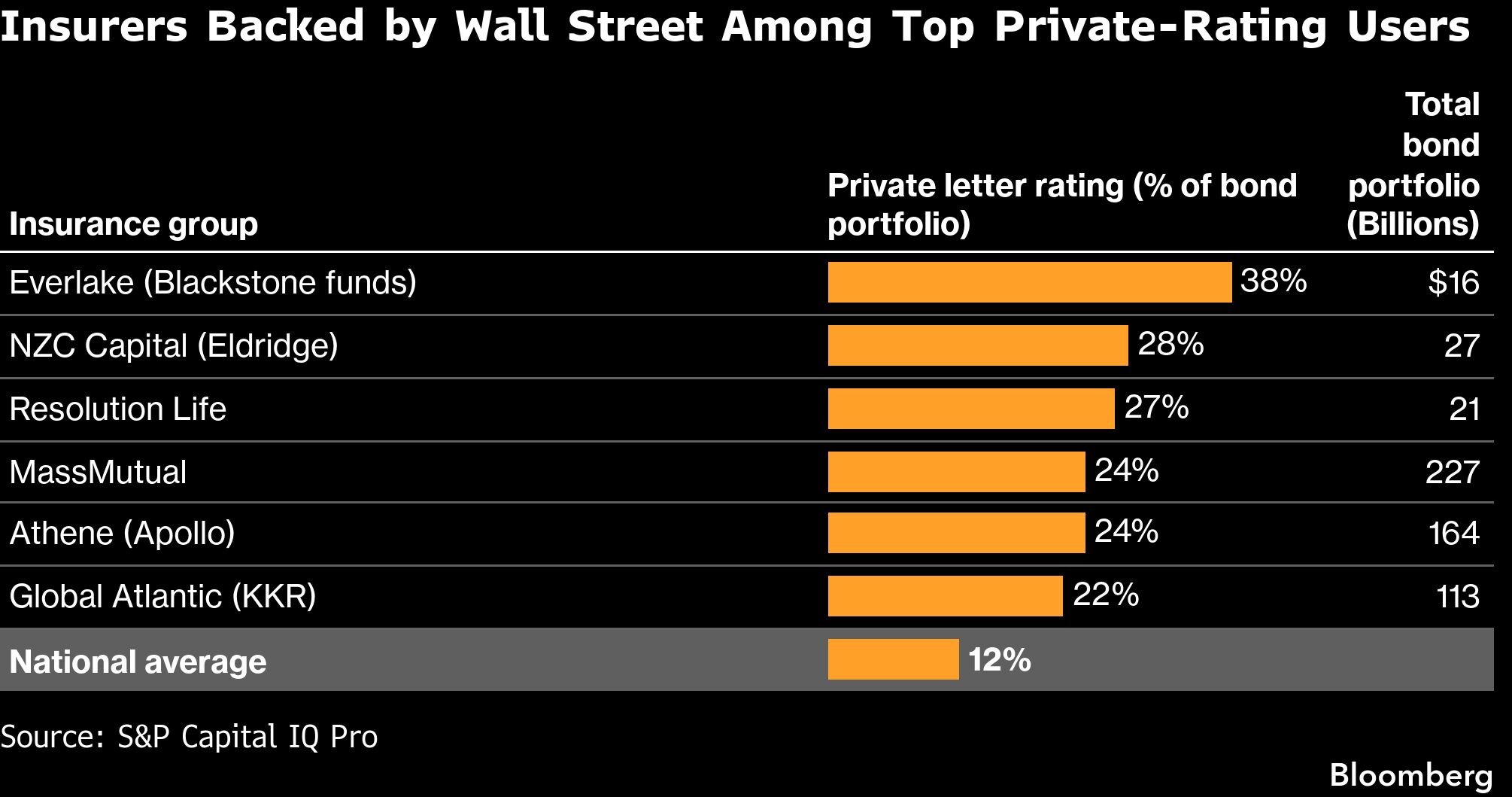

Insurers owned by Wall Street investing firms tend to use private ratings much more. Filings by their insurance affiliates show privately graded securities can represent more than 20% of their total rated credit portfolios.

That includes the insurance affiliates of fund managers Blackstone Inc., Eldridge Capital Management, Apollo Global Management Inc. and KKR & Co. Spokespeople for those businesses declined to comment, as did a representative for Resolution Life Group Holdings Ltd., which uses Blackstone as an asset manager.

Massachusetts Mutual Life Insurance Co., which uses private credit ratings for 24% of its rated credit portfolio, said it’s “been a disciplined and successful investor” in private credit for more than five decades. “Our strategy has consistently outperformed public market alternatives across economic cycles, reflecting our diversified investment approach across asset classes and sectors,” it said in a statement.

Highlighting private credit’s increasing centrality in financial markets, Apollo and Blackstone on Tuesday announced a $35 billion financing package for Anthropic PBC’s AI infrastructure. It’s one of the biggest private credit transactions in history.

The Columbia researchers estimated that if private ratings were aligned with the underlying assets’ performance, the insurers would need to hold about $4.5 billion more capital, a total that would be borne by a fleet of firms.

Insurance companies in the US are regulated primarily by their home states, while the National Association of Insurance Commissioners sets nationwide standards and rates a small number of assets itself.

“The NAIC and state insurance regulators have been actively monitoring and progressively addressing insurers’ evolving investment portfolios for many years,” the organization said in a statement, noting that regulators are able to challenge ratings when appropriate.

The team of academics released their sweeping study examining more than $4 trillion of assets after a much smaller review a few years ago by the NAIC that set off controversy.

In that case, the NAIC examined 109 securities that were assigned a credit rating by its staff and then later given a private rating, which on average was three notches higher. After pushback from the industry, the NAIC retracted the report “to undergo further editorial work” and hasn’t published an update since.

The NAIC is now working on a new process to test the appropriateness of credit ratings, with the possibility of barring ratings firms with persistent problems. The industry has been invited to submit questions and comments on the proposal.

For insurers, ratings firms do more than simply determine whether a bond clears the investment-grade threshold.

Insurers are required to set aside extra capital based on the riskiness of each asset in their portfolio. The higher an asset’s grade, the greater the relief to the insurer.

For instance, an insurer holding a $100 million bond rated BBB, the second-lowest investment-grade notch, would set aside about $1.5 million — less than half the charge for a BB+ or a BB rating.

The less capital insurance companies must hold, the more they can return to their owners or deploy for growth.

A message from Advisor Perspectives and VettaFi: Discover something new! Click hereto register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.