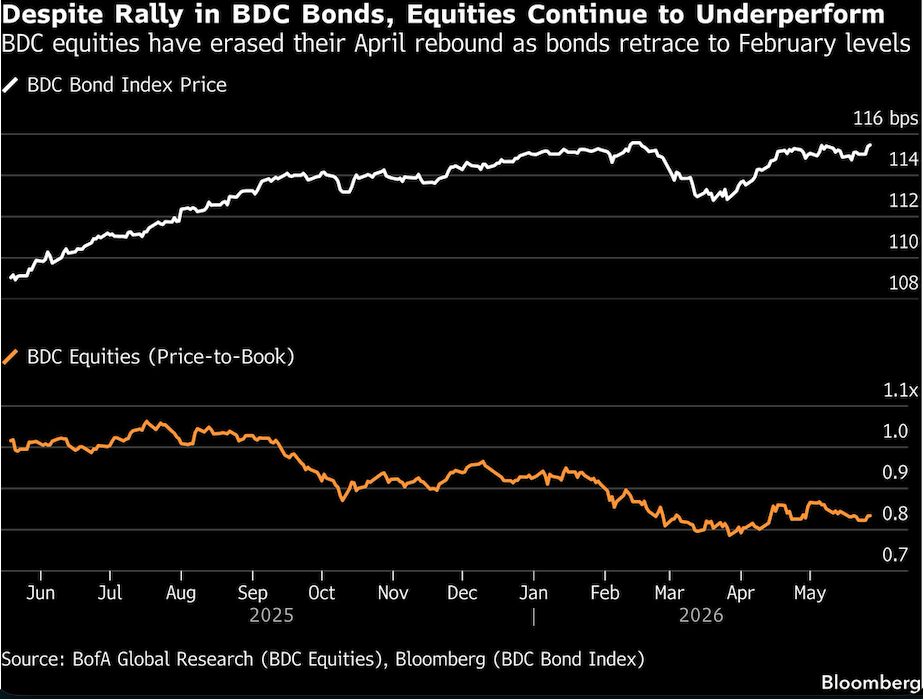

As shareholders rush to pull money from private credit funds over troubling questions about software exposure, opaque loan values and non-payments, some bond investors are doing the opposite: buying their debt.

Drawn in by yields that reached multi-year highs, investors have in recent months waded back into bonds issued by business development companies, or BDCs, even as share redemptions swell. In April and May, the niche credit funds raised billions of extra capital from debt buyers, while their existing bonds have recouped much of their losses from February and March.

It’s too soon, many industry watchers say, to conclude the worst is over for the $1.8 trillion private credit market, which continues to be beset by concerns about lax lending standards and loans to software firms vulnerable to AI. Just last week, two big names, Blackstone Inc. and Cliffwater LLC, disclosed soaring redemption requests at their flagship funds and imposed limits on withdrawals, indicating the bleeding is far from over. The bond gains, some argue, may simply reflect fast money snapping up beaten-down assets with high yields.

The disconnect, though, is notable in a couple ways. First, it suggests that some bond investors are betting that BDCs — which generate income for both creditors and shareholders by extending loans to smaller companies — will bring in enough cash to repay their debts even if they’re forced to cut dividends. Second, while the waves of redemptions risk begetting more fund outflows that spiral into a liquidity crunch, steps to restrict, or “gate” withdrawals to preserve capital are a plus for bondholders who are first in line to be paid.

“Initially, some investors viewed gating negatively and thought equity injections would be needed,” said Teddy Hodgson, Morgan Stanley’s global co-head of investment-grade debt capital markets. “But as people have done the work, from a senior unsecured bond perspective, gating is actually viewed as a good thing.”

Since the start of April, BDCs have raised nearly $8.4 billion issuing bonds, according to Bloomberg Intelligence. That compares with just $3 million in March and more than $7.3 billion in the first two months of the year.

ARCC — Ares Management Corp.’s largest publicly listed BDC — sold $800 million of notes in early May. The deal not only drew longtime buyers but also new investors such as international and long-only asset managers, according to Scott Lem, ARCC’s chief financial officer.

BCRED, Blackstone’s flagship BDC, attracted about $4.3 billion of demand for an $850 million offering in April — up from a target of $500 million — and priced at yields only slightly above its existing debt.

That same month, a private credit fund from Blue Owl Capital Inc., which has been at the center of the industry storm, raised $400 million. In a vote of confidence, Pacific Investment Management Co., an early direct-lending critic, bought the entire chunk. The same fund raised another $400 million selling bonds last month, while separate Blue Owl BDCs sold $500 million bonds this week and last.

The $36 billion fund that sold debt this week — Blue Owl Credit Income Corp., or OCIC — is the second largest BDC after Blackstone’s BCRED. Though redemption requests from OCIC totaled 22% in the first quarter — and were subsequently capped at 5%, the industry standard — net outflows were less than 1% of net assets after accounting for share subscriptions, according to BI.

“The market seems to have considered emerging risks and concluded they’re not a dire threat,” said David Havens, a credit analyst at Bloomberg Intelligence.

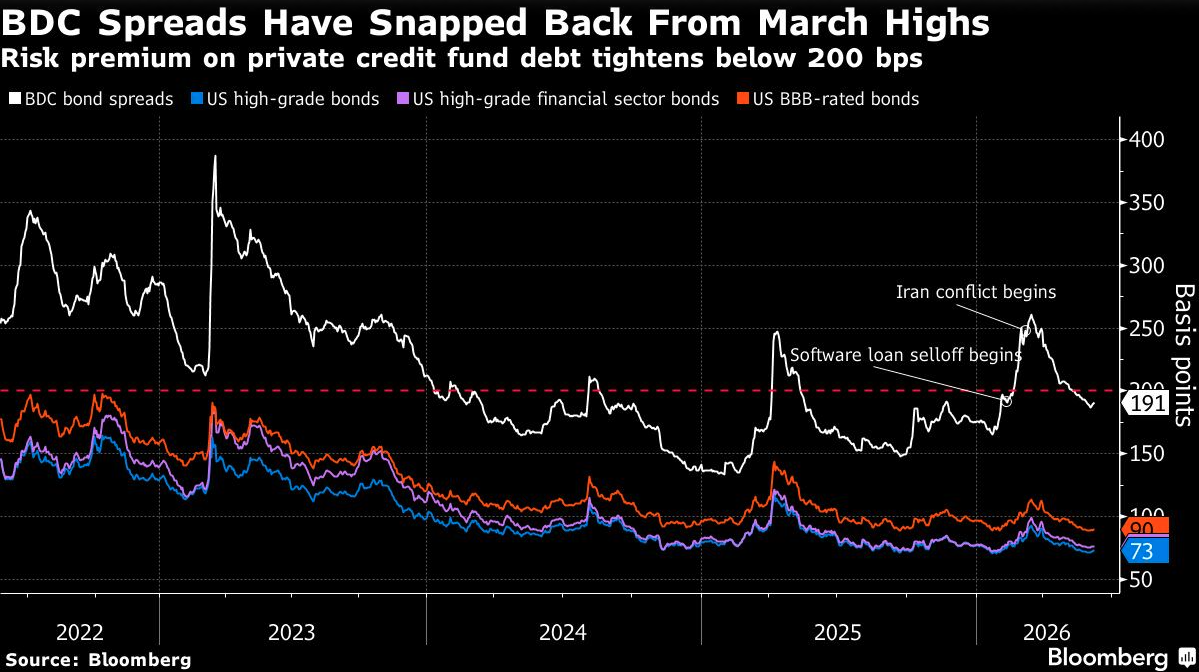

Indeed, the extra yield that investors demand to own BDC bonds instead of Treasuries has snapped back below 2 percentage points to levels last seen in February. In March, the spread stood at more than 2.6 percentage points.

The rally “suggests that the system is structurally protected and that many of the fears were overblown,” said Michael O’Brien, who helps run the Hilton BDC Corporate Bond ETF, the first exchange-traded fund investing solely in unsecured notes of publicly-traded BDCs.

O’Brien and Morgan Stanley’s Hodgson expect BDC spreads to narrow further. Those of non-public BDCs in particular have room to tighten, after their risk premiums widened more than twice as much on average as their listed peers.

Last month, CreditSights Inc. initiated coverage of BDC debt with an “outperform” recommendation, emphasizing that several higher-quality funds more than compensate investors for any lingering concerns. Meanwhile, some buyers are locking in yields today to hold to maturity, Hodgson said.

Although BDCs are borrowing more and at cheaper rates, worries over liquidity, valuations and earnings still abound. At the Bloomberg Global Credit Forum in New York last week, investors warned the direct-lending market could be due for a long-delayed reckoning.

For instance, more private BDCs are at risk of losing their high-grade debt ratings, according to Bank of America Corp. Meanwhile, after redemptions exceeded fundraising last quarter for the first time, according to Robert A. Stanger & Co., this quarter is shaping up to be even worse.

Cliffwater’s flagship fund capped redemptions at 5% in the second quarter after shareholders tried to pull about 17% of shares. BCRED limited withdrawals for the first time after investors sought to redeem 10%. In other words, there’s a real risk that bond investors are getting it very wrong.

“Don’t mistake a reprieve for a recovery,” said Mark Malek, chief investment officer at Siebert Financial. “The underlying stress hasn’t cleared by any means. It’s just been papered over by fast money hunting for yield on the dip — newer hot money searching for a home.”

To Steve Katznelson, CIO at Radcliffe Capital Management, the different pressures on the shares and bonds are a reason to prefer BDC debt.

Both produce steady income, but BDCs are far more likely to cut dividends rather than skip bond interest payments to preserve capital.

At Radcliffe, which has invested in BDC debt since 2014, part of the strategy is identifying investment-grade BDC bonds that offer better metrics — like higher yields and greater potential appreciation — than other high-rated debt.

“There are lots of challenges for equity holders — potential dividend cuts, writedowns — but from a credit perspective we like it a lot, and clearly others do too,” Katznelson said.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Rene Ismail