Financial markets generally displayed exuberance Monday after the US and Iran agreed to an interim peace deal to reopen the Strait of Hormuz. Oil prices fell to the lowest since early March and the S&P 500 Index surged, leaving it just a few points below its all-time high reached at the start of the month. The odd man out was the bond market, with US Treasuries giving up most of their initial gains to end the day little changed.

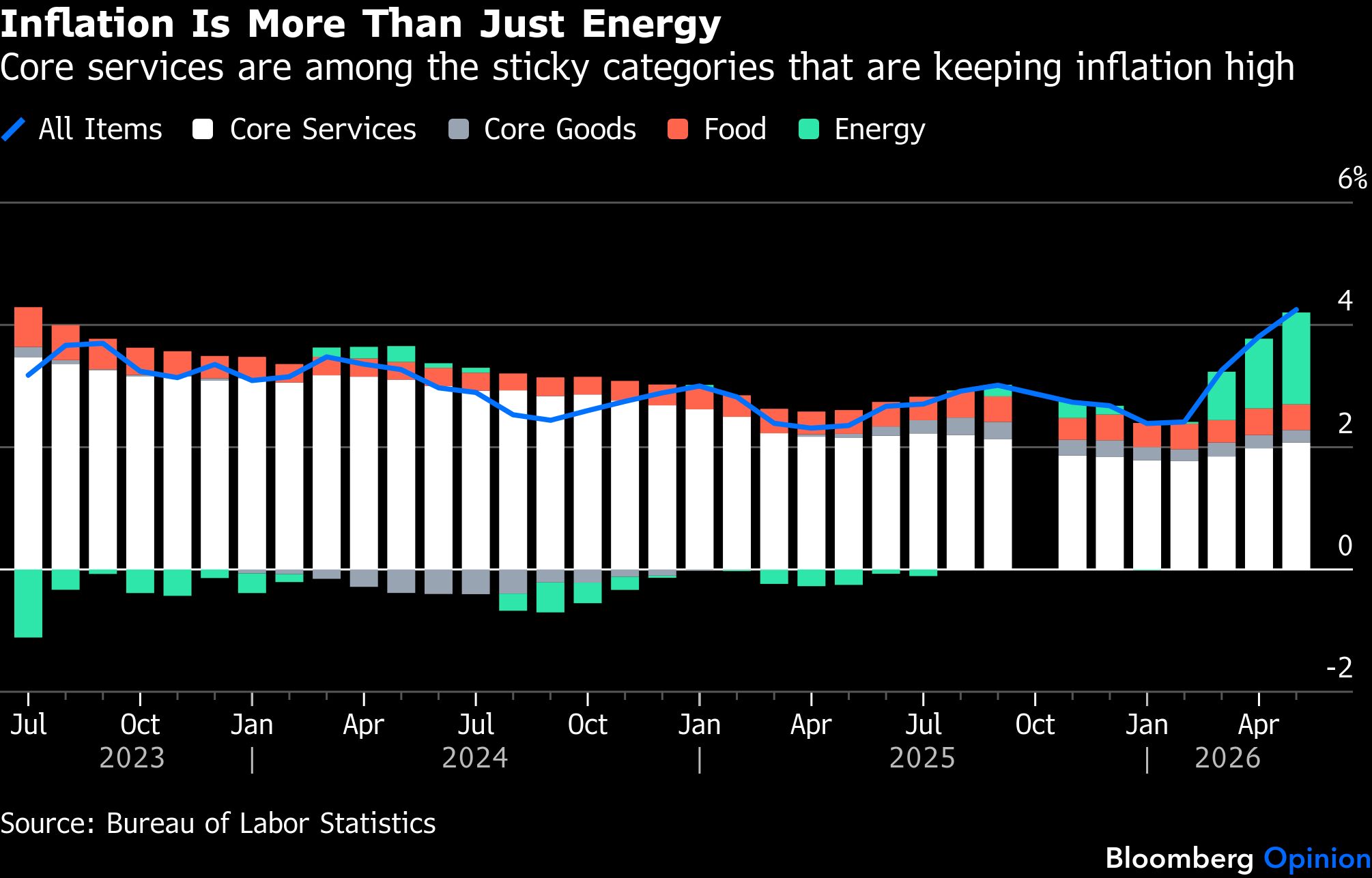

Let’s start with the bad news: Bond yields don’t have much room to fall from here. Even leaving energy costs aside, there are plenty of signs that inflation is a bit stickier than previously understood. Core services such as medical care and internet providers are inflating at a persistently warm rate, while ripple effects from the artificial intelligence boom are adding upward pressure on software and other categories including memory and storage.

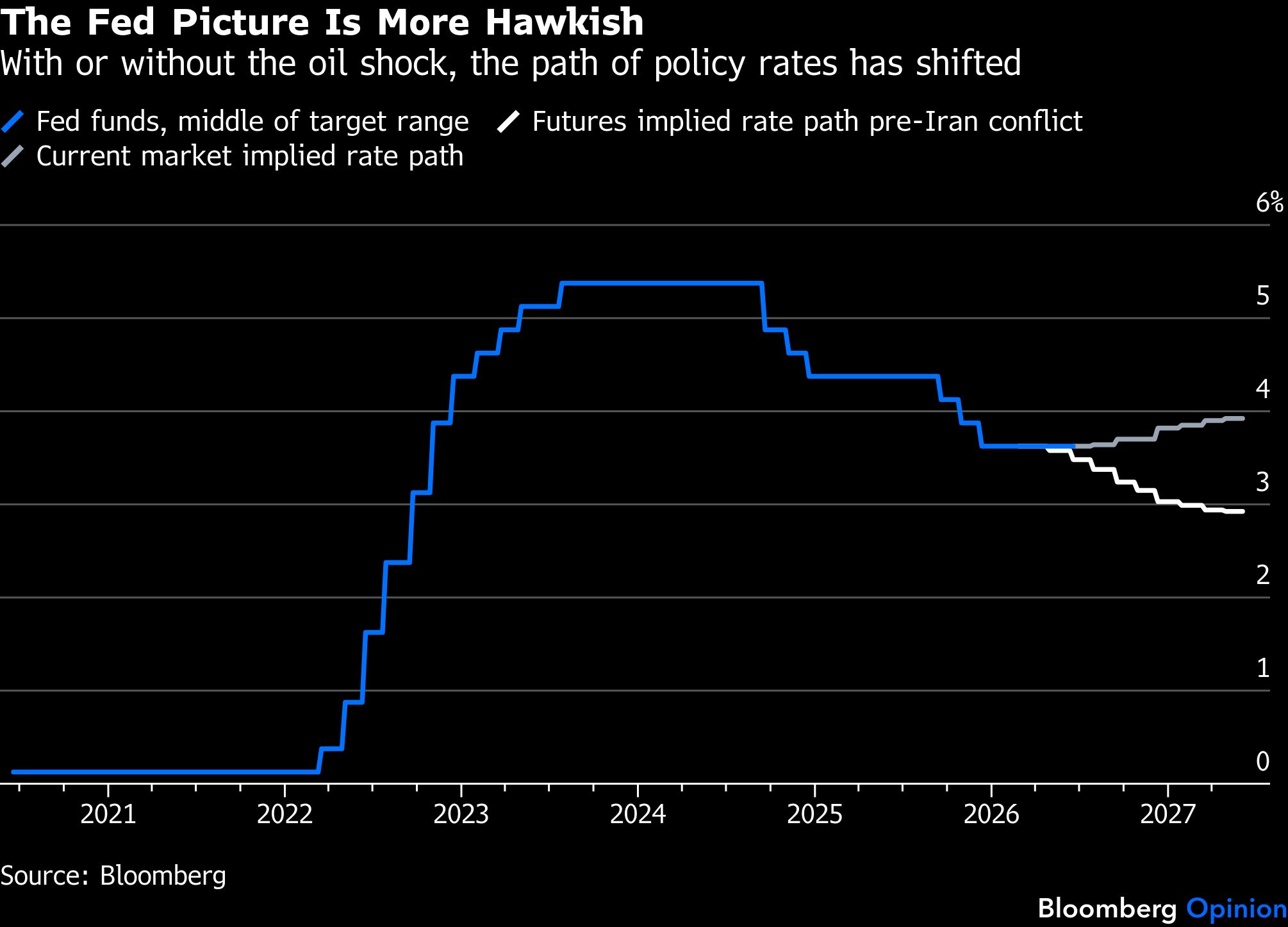

The labor market has seemingly begun to stabilize, too, taking pressure off the maximum-employment side of the Federal Reserve’s dual mandate. Nonfarm payrolls have expanded by an average of 188,000 in the past three months, the best result since March 2024. Federal Reserve interest rate cuts that were priced in before the US-Israeli strikes on Iran are now ancient history. The Fed certainly isn’t going to be cutting rates twice in 2026, as futures markets implied back then.

Don’t expect to hear that message from new Fed Chair Kevin Warsh on Wednesday. He isn’t likely to come out overtly hawkish at his first post-meeting press conference, given the dovish preferences of President Donald Trump. But I suspect that a combination of persistently high core inflation and a resilient labor market may, by the final quarter of the year, bring him to the realization that the economy now requires some modest rate increases. With yields on 10-year Treasury notes down about 0.20 percentage point from the May peak, it’s likely that the bond rally is about to hit a wall.

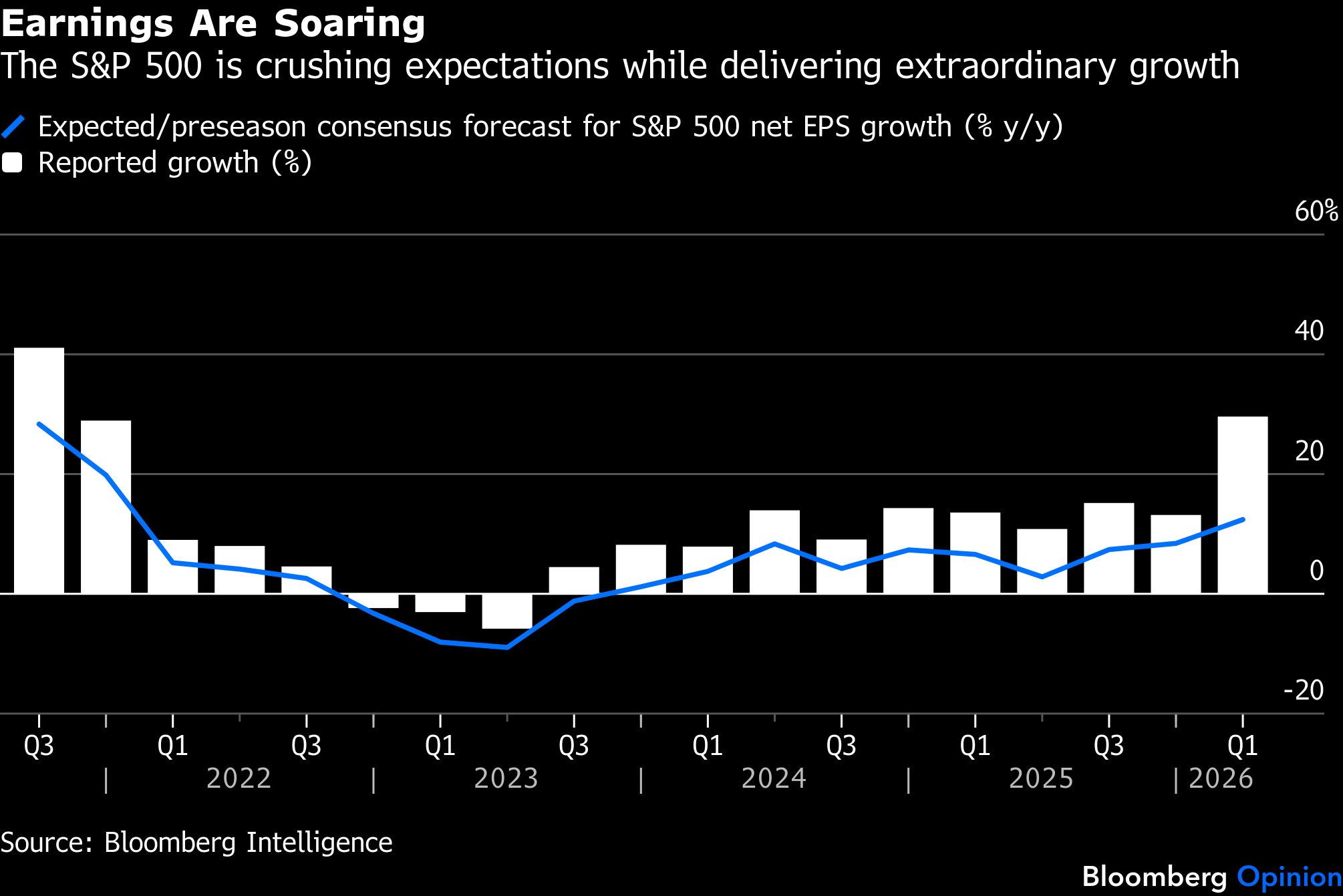

The stock market is a different story. The earnings of S&P 500 companies have gone from good to on fire in the months that tensions in the Strait have simmered. The index’s earnings per share grew around 30% in the first quarter from a year earlier, the best quarter since 2021 and well over double the 12% growth that analysts expected before earnings season.

The market has been rallying on pure fundamentals, even as price-earnings multiples contracted during the conflict. The index’s forward price-earnings ratio sat at 20.8 at the time of writing, down a half point from before the hostilities. It’s still no bargain by historical standards, but it’s meaningfully below the average that prevailed from 2024 through 2025.

Needless to say, it’s still possible that the reopening of the Strait of Hormuz will be a lot more complicated than Trump has conveyed in public. As Bloomberg reported, the US’s European allies have many practical questions and have expressed skepticism about Trump’s timeline for a reopening. Even the interim deal is far from set in stone, with Washington and Tehran still hashing out next steps ahead of a signing event planned for Friday in Switzerland.

Another risk for the market is that earnings themselves are in a sort of bubble. The most extraordinary growth has come from sectors benefiting from the big technology companies’ capital spending such as semiconductors. If the hyperscalers were to even signal an investment slowdown, the whole edifice could wobble, including the wealth effect that has sustained resilient spending in the US. Consumption is about two-thirds of the economy, but consumer stocks have been conspicuously absent from the S&P 500’s 10% rally since the Iran hostilities began. Excluding Amazon.com Inc. and Tesla Inc., large-capitalization consumer discretionary stocks retreated 5.1% in the period, with homebuilders, restaurants and apparel all suffering.

AI concentration risk is very real, but so are the earnings that companies are churning out. At this pace, stock optimism can clearly outlast the latest geopolitical gambit from Trump — and maybe even the one after that.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Income Topics >