Fixed Income Asset Allocation Post-Apocalypse

December 21, 2012 — the day the Earth was prophesized to collide with a black hole of kaputness — has come and gone in defiance of the Mayan calendar. The sun continues to rise, the earth turns and, wouldn’t you know it, 2013 booted up on schedule. While the world didn’t end, it’s not all bunnies and sunshine here on the third rock from the sun; although we humans didn’t fall by the wayside as 2012 drew to a close, neither did all those other earthly problems we were so worried about. Curses!

The more upbeat interpretation of the 5,125-year Mayan cycle, however, is that the end date doesn’t signify Armageddon but rather the beginning of a new time for positive change here on earth. Although that sounds like a bit of fortune-cookie poppycock, the alternative meaning of calendar reset is all we’re left with in the absence of Armageddon, and that truly may be news to celebrate. Because while scary unknowns have and always will exist, we — unlike our Mesoamerican forefathers — know now that we have an opportunity to address them. So allow us to suggest an investment playbook to cash in on this silver lining. In short, the sweetness of the metaphorical fortune cookie in your hand will depend on how you allocate your fixed income assets in 2013.

Global imbalances are here to stay. The developed world’s growth-inhibiting deleveraging cycle has only just begun, as evidenced by the frenetic end-2012 headlines surrounding the doom-and-gloom forecasts of the U.S. driving over its own self-imposed fiscal cliff. Our long-standing psychological prognosis of European leaders squaring off over their debt crisis — that mutually assured destruction is not the path typically chosen by rational parties — is just as applicable to U.S. politicians and lawmakers, who we believe will continue to concede to a stair-step approach to fiscal tightening in the form of prudent tax hikes and spending cuts, as opposed to reckless and destructive cliff-diving.

Against the backstop of highly accommodative monetary policy, private sector growth in the U.S. appears to be sustainable. Even as the salutary impact of Uncle Sam’s fiscal Alka-Seltzer begins to fade, U.S. consumers appear to have recuperated enough from their mid-‘00s overindulgences to foster economic growth in 2013. Balance sheets for private citizens are in significantly better shape today than they were prior to the financial crisis, and the renaissance within the U.S. housing market is contributing to growth both directly and indirectly (by supporting household wealth and thus consumer sentiment).

Europe, on the other hand, will not be able to offer much in the way of 2013 growth, as its banking system continues to deleverage. Alternative sources of financial intermediation will struggle to fill the gap seamlessly, but the availability of aid from the European Central Bank, European Financial Stability Facility and European Stability Mechanism has and will continue to provide significant insulation from hiccups in the periphery. However, we admit political outcomes will almost assuredly be suboptimal at times and lead to bouts of heightened volatility.

Across emerging markets, the stimulus cycle that featured broad rate cuts in 2012 — while largely over — is paying dividends, as the drivers of global growth like China and Brazil are no longer stalling out. The giant in the east, for instance, now appears able to achieve stable growth levels consistent with the new central government’s 7.5% target. Buoyed by the aforementioned demand from the U.S. consumer, China’s export channel will contribute to keeping the global growth engine humming.

Despite the presence of political uncertainty and volatility likely induced at times by global imbalances and the larger deleveraging cycle, our forecast is for sustained positive macro momentum and modest global growth in 2013. The latter is in large part due to the ubiquitous fiscal and monetary stimulus of 2012, which produced exceptional calendar year returns ranging from 9% in U.S. investment-grade credit to 17% in emerging market dollar-denominated bonds; even U.S. Treasuries rallied sharply. The result is that the fixed income landscape has richened substantially going into 2013, with valuations further stretched by capital flows from investors hungry for sources of sustainable yield and income.

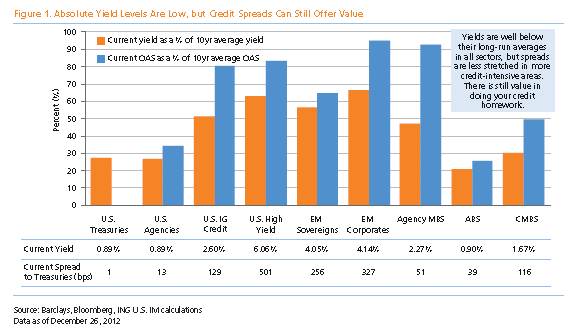

Whereas in 2012 allocating to just about any spread sector with yields in excess of long-term inflation expectations was absolutely the right play, yields in Treasuries, agencies and asset-backed securities are now 70–80% lower than their average level in the decade prior and are far less attractive relative to credit sectors like investment grade corporates, high yield and emerging markets sovereigns and corporates. While yields in these asset classes are a hopping 40–50% lower than they were in 2010–11, as a spread to comparable U.S. Treasuries they are much closer to long-term averages and therefore present greater relative value — particularly in our base-case scenario of moderate economic growth, abundant financial liquidity and good credit quality (i.e., low default probabilities) in most sectors. Moreover, given that Treasury yields are biased to correct upward this year as investors replace Treasury holdings with riskier, growth-sensitive asset classes like equities, simply allocating to fixed income in general — and credit, in particular — is not the best approach and could prove costly from a total-return standpoint in a world where the risk of rising interest rates is once again a concern as growth momentum picks up and the scary unknowns grow less scary.

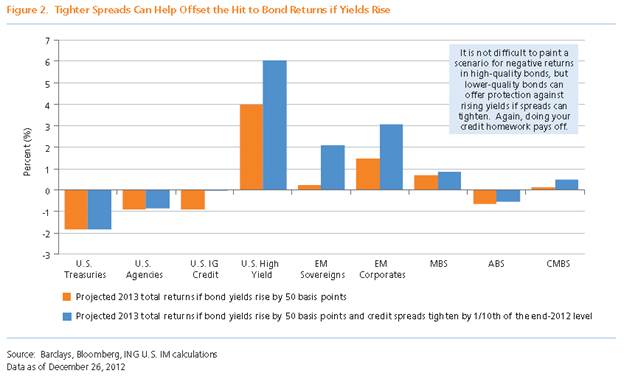

The true sweet spot of fixed income investing occurs after a period of rising Treasury yields and widening credit spreads, when opportunities emerge in undervalued sectors that can benefit from both falling yields and spread tightening. But with low Treasury yields and below-average credit spreads a reality at the start of the new year, 2013 is not shaping up to be quite as sweet as 2012. A rise in yields of only 50 basis points, for instance, would generate negative total returns in the higher-quality sectors like U.S. Treasuries and investment grade credit. While tighter credit spreads in lower-quality sectors will help boost total returns — particularly helpful in a rising-yield environment — return expectations vary considerably based on the underlying credit quality of the specific sector and by the degree of actual spread tightening (see Figure 2) That means that 2013 will be a year during which income investing, active sector allocation and security selection will be prerequisites for success. Fixed income investing will return to its roots — performing credit analysis to pick the right sectors, the right issuers and the right bonds, while being wary of and managing interest rate risk along the way.

As growth momentum is expected to be positive in 2013 despite lingering macro uncertainties from 2012, the silver lining for fixed income investors is that, as tail risks continue to abate, attractive total-return opportunities will present themselves, but only if you do your homework — good old-fashioned credit homework, that is! Because as central banks stay active and as cheaply valued investments become more scarce — especially in the highest-quality segments of each asset class — active sector rotation will be important, but prudent bottom-up security selection will drive a growing share of risk-adjusted excess returns in 2013. The Mayans may have envisioned an end to the world in 2012, but by sidestepping the Apocalypse and buying time to address our earthly problems, the tried-and-true tools of old-school bond investing will be key to our 2013 story.

This commentary has been prepared by ING Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors. Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169