“The American Republic will endure until the day Congress discovers that it can bribe the public with the public’s money.”

Alexis de Tocqueville, 1805-1859

French political thinker and historian

Author, “Democracy in America” 1835

If he were alive today, we think monsieur de Tocqueville, who “wrote the book” on American democracy, might be concerned about the viability of the American Republic. Our government provides generous services for which the current public is not required to pay. Though collectively failing to run the country well, individual Congressmen are reelected by delivering the bribes their constituents want, whether these be low taxes or high services (world class defense, state-of-theart health care, secure multi-decade retirement for all, etc.).

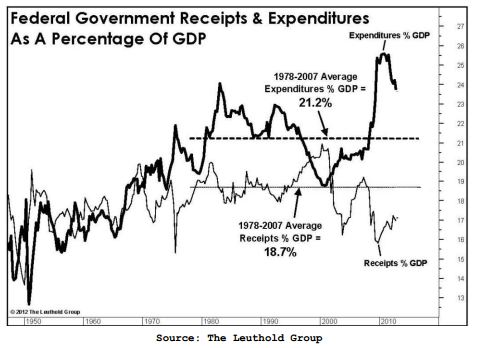

While a last minute compromise may have been reached on taxes, it represents only a brief rest stop on a required road of repair. On the positive side, we should see less annual wrangling with tax rates having been made “permanent”, meaning they will not automatically change at some future date (but rather only when Congress feels like changing them), with many areas also sensibly indexed for inflation. On the negative side, the projected $737 billion of deficit reduction1 associated with the politically self-congratulated Tax Act does not erase continued budget deficits. Put another way, the $16.4 trillion in outstanding federal debt obligations will continue to grow, not shrink. Worst of all, the fast and furious political wrangling at a seemingly final hour represents only the opening act in a drama which will continue to play out as we wrestle with the yawning gap between federal government receipts and expenditures, as illustrated below.

Still aboard a Mr. Toad’s Wild Ride, we are set to crash against the federal “debt ceiling” in March. The new deadline for implementation of blunt automatic federal spending “sequestration” cuts arrives at the same time. The situation is a tinderbox. The President has vocally and explicitly stated he will not engage in debate over raising the debt ceiling… meanwhile, a majority of House Republicans voted against the New Year’s Eve Tax Act and many consenting Republicans stated they were keeping their powder dry for the debt ceiling fight. This year, “March Madness” will encompass more than basketball.

Politicians are often blamed for their inability to enact a plan to reduce the deficit. While this is true to a certain degree, we believe the ultimate guilty party is the American voter, who gets the sort of politicians that they elect and perhaps deserve. The digression of a short quiz will help diagnose the problem.

Question #1) do you support ending the continued budget deficits?

Question #2) do you propose closing these deficits by:

a) cutting government services for the most vulnerable Americans: the elderly, poor, sick? or

b) raising taxes which inevitably hurts the economy, businesses, workers and overall American competitiveness?

Question #3) if your preferred solution in #2 was outvoted, would you support the alternative solution?

If you answered “no” to question #3, then you can see why Congress has such trouble coming to a comprehensive deal. If you answered “yes” to question #3, congratulations, please call your Congressman.

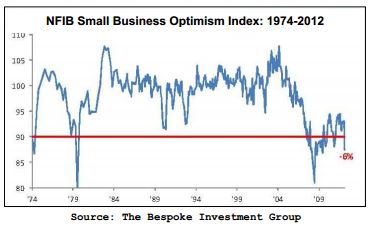

Not surprisingly the absence of budgetary certainty has badly bruised business, consumer and investor confidence. Mid-December witnessed a monthly drop of six percent in the National Federation of Independent Businesses (NFIB) Small Business Optimism Index. This is the largest monthly drop since 1986 and the current level of optimism is the lowest recorded outside a recessionary period. 41% of index respondents cited either taxes or government requirements and red tape as their single most important problem. The Michigan Consumer Confidence report also showed a 13.8% drop in its expectations component during December, the third steepest one-month decline since the 1970’s.

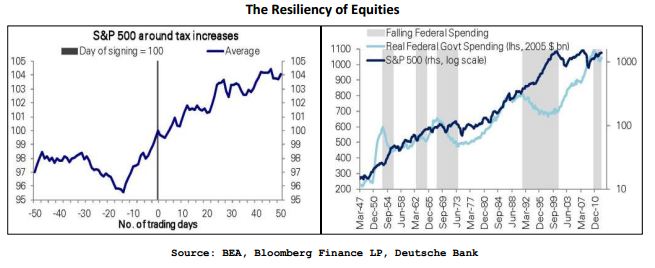

Despite largely locking in Bushera rates, taxes went up for 77% of Americans (most being hit by expiration of the 2% payroll-tax holiday). The annual tax increases, estimated to amount to roughly 1% of GDP in total, are mild and fall within the range of past hikes. Additional fiscal drag of perhaps 0.5% might arise from upcoming across-the-board “sequestration” spending cuts set to take place in March. These tax increases and spending reductions might cause one to fear for the economy and hence equity prices. History may suggest otherwise. Stocks typically weaken in the months leading up to a tax hike, as was the case during the fourth quarter, but then bounce back to new highs (see chart below at left). Perhaps surprisingly, the S&P 500 Index has a history of performing well during periods of falling federal spending (see chart below at right). The point is that capitalism and markets are irrepressible and it would be a mistake to let dark clouds on the horizon keep you completely out of the markets.

With all the gloomy discussions of a sub-par recovery and dysfunctional government, many would be surprised upon remembering that we are in the fourth year of an equity bull market. This is a really useful reminder. If you knew how dysfunctional the government was going to be over this time, you might have thought it wise to sell all your stocks… that would have been a big mistake given over 100% in market gains to date. Four-year bull markets have occurred only eight times since 1935. Five of these past eight cycles made it another full year, averaging an additional 19% gain. We see the coming year producing further equity gains on the back of P/E expansion driven by improved investor confidence and an eventual move away from cash and low yielding fixed income into equities. Those previous bull markets that did not complete a fifth year were at more expensive levels than today: forward P/E ratios of 16x to 22x versus the current 14x. Previous failures to complete fifth years of bull markets were commonly marked by recessions… and we do not expect one this year for the following reasons: pent up demand from corporate cash levels at a fifty year high and durable good spending at a 50 year low; economic tipping points have historically only been reached when readings of initial jobless claims were at far lower levels; the household debt service ratio (debt payments vs. income) is at a 30 year low. Hence, subdued market and economic conditions leave ample room for growth before we risk overheating. The bigger danger is a slip into deflationary contraction, but that specter is being fiercely confronted by the Fed… such a policy is not without cost, however.

Savers enjoy the pleasure of real loss in wealth as inflation runs above available yields. For those with money in the bank or money market funds, your purchasing power (i.e. real wealth) is being siphoned off at a rate of about two percent per year. This situation gives rise to an interesting result: if the average stock declines three percent in price every year it will still prove a better investment than cash, because the average two percent dividend yield will result in a net loss of (only) one percent. Bonds may slightly outpace the decaying effects of inflation, but they offer virtually no upside while retaining not insignificant downside risks, as detailed in our previous letters.

Despite what we see as relative value in stocks, the year 2012 saw US equity mutual fund net outflows of $156 billion, surpassing the record net outflows of the crisis year 2008. Exchange Traded Funds (ETFs) continued to gain investor acceptance and contributed to traditional mutual fund outflows: US equity ETFs reaped a record $80 billion in net inflows for the year. These contrasting fund flow directions bring a good opportunity to reflect on financial products, which, much like security prices, have cycles all their own. For example, consider credit default swaps, which were more or less invented over the last 20 years and enjoyed an absolute explosion in growth. Some prescient commentators warned of the risks, but these concerns were (and amazingly continue to be) largely shrugged off by market participants, especially the banks that profit immensely from operating the infrastructure. Of course we now know what happened. These products introduced huge risks to our financial system, contributing greatly to its near total collapse in 2008. Credit default swaps, the up and coming wonder product, directly resulted in a $162 billion dollar bailout of AIG because regulators were too afraid of what might happen if AIG couldn't pay off all its losing swap-bets to Goldman Sachs and other teetering banks.

Financial history is the most woefully under-taught aspect of our discipline, but at Knightsbridge we strive to be students. We’ve observed a simple three-stage pattern in financial products and innovation that has repeated itself over and over in financial history from South Sea Company shares in the 1720's, to stock margin accounts in the 1920's, to junk bonds in the 1980's, to CDO's and CDS's in the 2000’s.

Stage 1: Introduction of new financial product

Stage 2: Enthusiasm

Stage 3: Tears

What might be the next product to experience this cycle? One candidate could be ETFs, which have advanced well into stage 2.

A growing number of commentators have speculated (we agree) that the explosion in ETFs has played a large role in the increasing correlation and volatility of financial markets that have proved so damaging to the investing public’s confidence. Recent congressional testimony indicates that the amount of money traded in futures and ETFs dwarfs the amount traded in individual stocks, so the tail has begun to wag the dog as the derivatives are more prevalent than the underlying. However, we’d like to speculate on a danger other than that posed to market stability and the financial system, a danger not as widely recognized: the risk to the common investor that some of these instruments may not perform as advertised.

Our sense of danger stems from a simple dichotomy of two observations that don’t seem to add up. 1) ETFs often charge lower direct fees than the mutual funds they are replacing. 2) ETFs are largely assumed to be wildly profitable for their sponsors, and there has been an explosion in their offerings. According to Izabella Kaminska of the Financial Times, “…the ETF business is so profitable that it’s turning the money management world on its head… ETF providers [are] generating profit margins more than four times higher than traditional mutual fund providers – even though ETFs are inevitably marketed as ‘low cost’.” In the last 12 years the number of ETFs offered has exploded from 95 to more than 1,400.

How are sponsors (largely banks) able to charge less and profit more? Yes, there are some plausible explanations that financial advisors trying to sell you ETFs will offer, but we will posit another explanation, one that often underlies a new product with slightly higher return: the higher return comes from taking hidden risk.

ETFs, like mutual funds, are usually explained as holding a basket of underlying assets from whence the return really comes. However, we’ll discuss three separate scenarios where the assets aren’t really there.

First and most importantly, ETF sponsors don’t act as fiduciaries in the way mutual fund managers do. ETF sponsors don’t need to bring the best possible return, they just need to deliver returns mimicking some benchmark. As a result, the sponsors engage in what is called “sweating the assets” in order to increase their own returns. A vanilla example of this would be a sponsor taking the money you buy the ETF with, buying underlying assets, and then lending those assets out to someone else to collect a little profit. If the loan is repaid, then you, the ETF holder, receive the return of the underlying assets, but the ETF sponsor gets to keep all of the lending income. And if the loan isn’t repaid… well, that just hasn’t happened yet on a large scale. Do you know in what ways your ETF sponsor is “sweating the assets”? Have you read your ETF prospectus? Does the sponsor even disclose its activities?

Second, according to recent congressional testimony, 27.4% of trades associated with the largest ETF end up temporarily failing. Failing means that money is delivered, but underlying securities are not. A retail investor would never know, as the ETF will show up on a brokerage statement sure enough, but it may not actually be there on the books of your broker, or the securities that are supposed to underlie the ETF may not be there with the sponsor. With stocks there are rules against failing on trades and fines are imposed, but somehow ETF sponsors have gotten exemptions from these rules. Is it any surprise then that failed trades abound and seem to increase every year? Yes, your broker is supposed to make investors whole and usually tracks down and fixes the fail in due course, but what happens when your broker is MF Global?

Lastly, there are so-called “synthetic” ETFs (contrast with previously described “physical” ETFs), which don’t even claim to own underlying assets. Instead, they mimic the return of those underlying assets through the use of derivatives, but as we all know, and as described above, derivatives don’t always work as advertised. Is it surprising that synthetic ETFs are even more profitable to sponsors than are the physical variety? Using over-the-counter derivatives is another form of hidden risk. You have the “visible risk” that you lose the bet, and then you have the “hidden risk” that you win the bet but the counterparty cannot pay.

To be fair, the vast majority of ETFs are probably run by honest and forthright institutions, most funds will turn out to efficiently do what they were advertised to do, and ETFs do have certain tax advantages over mutual funds. By far the highest risks are in the synthetic ETFs with esoteric objectives (e.g. triple levered returns), and most investors will probably be fine if they avoid these in favor of vanilla physical ETFs designed to replicate large stock indices. However, we question “why risk it?” when the ETF creation/redemption process is so complicated, when there are incentives for sponsors to take on hidden risk, and when the settlement structure is largely untested. Most importantly, why risk it when insufficient time has passed and insufficient misery has been inflicted to expose and publicize ETFs’ weaknesses. If you sell your mutual funds to obtain a few tenths of a percent in fee savings, trusting that this new product will always work as well as the old, remember that you are engaging in the same thought process as the pension fund manager, who, for a few extra points of yield, bought a AAA mortgage CDO instead of a traditional AAA mortgage bond (this manager lost most of his money in 2008). We’ve already seen a few cockroaches on the floor and are willing to pay a bit more to avoid finding out the hard way if there are any behind the walls.

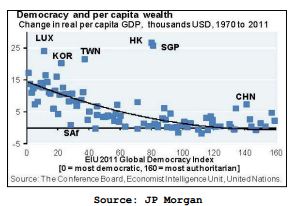

Let us leave behind the topic of financial innovation and return to the prospects of the United States. Despite its polarized state, we live in a country of substantial means and proven ability. Democracy, while frustratingly messy, offers proven ability to build wealth (as an aside, this is one reason we are skeptical that China can experience uninterrupted growth). The chart on the left ranks GDP per capita over 1970-2011 vs. a country’s degree of democracy as defined by the Economist Magazine’s 2011 Index. On a per capita basis, the more democratic countries have seen greater GDP growth. As Alexis de Tocqueville aptly stated, “The greatness of America lies not in being more enlightened than any other nation, but rather in her ability to repair her faults.” At least in this country we are fretting about our indebtedness as opposed to the Japanese who are much further down this path and appear much less concerned.

Despite a subdued economic recovery and fiscal fiasco, the year 2012 produced above average returns for US equities. In Europe, where macroeconomic conditions were even worse, equity returns were even better. In fact, one might say broad recognition of negative conditions directly creates the opportunity for compelling forward returns when conditions improve. Once again we are reminded that a contrarian perspective is often a critical ingredient for investment success.

Very Truly Yours,

John G. Prichard, CFA

1As with most budget figures, this is a ten year number, i.e. there is $737

billion of projected savings over the next ten years as compared to a scenario

whereby all 2012 policies would be extended.

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

© Knightsbridge Asset Management