When it was all said and done not much happened in the final quarter of 2012. Anxiety picked up immediately after the election as the bickering over the fiscal cliff escalated.In the end, the worst-case scenario was avoided – at least for a couple of months –and stocks ended about where they began the quarter.The S&P 500 was down -0.38%.Mid- and small-cap stocks did a little better but the clear winner was international stocks with the MSCI World ex USA up almost 6%.Despite many overt headwinds (the European debt crisis, a China slowdown, slowing earnings momentum, and the fiscal cliff) the year was very kind to equity investors.In general, stocks gained more than twice what will likely be a long-term average with most stock indices rising more than 15%.

The outlook for the stock market is as cloudy as ever. Although it may not feel like it, we are entering the fifth year of a bull market, which is relatively long from a historical perspective. Unfortunately, we are still dealing with the aftermath of the financial crisis and will be for many years to come. Deleveraging has begun where there was no alternative –consumers and state and local governments –and ultimately will need to end with federal governments.A real concern is the lack of progress for middle-income Americans. The US’s median household income in 2011 of $50,054 was $570 less than its median household income in 1989.The job market remains a problem and all wage earners will see a jump in taxes as the payroll tax holiday expired and was not renewed during the fiscal cliff negotiations.Adding to the uncertainty is the battle over spending, tax reform and entitlements that will start shortly.

Central bank action is both supporting stock prices and the biggest potential risk to investors. A major reason we turned bullish after the spring sell-off in 2012 was due to unprecedented support by the world’s central banks, especially the Federal Reserve (Fed) and the European Central Bank (ECB).Not only is the Fed providing liquidity to the market but also is forcing investors out on the risk curve by keeping interest rates near zero. Currently, the Fed is printing money to the tune of $85 billion a month to buy $85 billion of bonds, meaning its balance sheet is set to rise by $1 trillion a year! The ECB has announced a similar intent, although they haven’t started yet. We are in uncharted territory, and despite Bernanke’s soothing assurances, there most likely will be negative unintended consequences at some point in the future.

Offsetting these long-term risks are several near-term positive developments. The housing market has stopped falling and has bounced off a depressed base. Car sales are rebounding and consumer confidence is up. The US is at the beginning of what looks like an energy boom. China's slowdown looks to be over with manufacturing activity hitting a 14-month high in December. Conditions in Europe have even improved. Sovereign bond yields in key euro periphery countries are much lower than a few months ago. Unit labor costs are converging between northern and southern Europe.The Markit purchasing managers' index for the 17-member eurozone hit a nine-month high in December, although the reading of 47.2 reflected an 11th month of contraction.Most importantly, Europe took its first big step towards banking union, as eurozone finance ministers agreed to a plan to cede power to a common bank supervisor in Frankfurt.

From our perspective risk and return seem fairly balanced at this time.Strong arguments can be made for both bullish and bearish cases. Given our conservative nature we will err on the side of caution and will be sensitive to deteriorating conditions should they occur, especially regarding corporate earnings.On the positive side investors have yet to embrace equities in this bull market. According to federal data Americans have poured record amounts of money into savings accounts even though interest rates are at historic lows.The stock market could be pushed higher if sentiment shifts and this money leaks back into equities.Regardless, many stocks are attractively valued and we expect to continue to own a diversified portfolio of high-quality, dividend-paying sto cks.

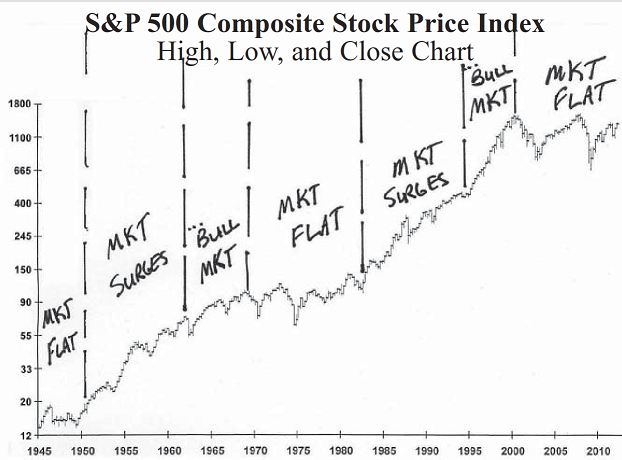

The chart below is a "long term" look from a piece by James Paulsen of Wells Capital Advisors, Jim writes: Since 1999, the experience of the "lost decade" looks amazingly similar to the character of the "earnings production" stage which occurred at the beginning of each of the last two major stock market cycles. That is, earnings have more than doubled while the U.S. stock market has been essentially flat. The next two stages could certainly depart from the character of the last two stock market cycles. The contemporary cycle could be prematurely aborted by numerous problems including another financial crisis, a war, or by escalating inflation. However, should this cycle continue to rhyme with the previous two post-war cycles, it may be time to worry less over earnings growth (which could be very modest indeed in the next few years) and focus more on how much valuations could rise as confidence continues to improve and investment horizons are lengthened? We believe the stock market cycle has already begun to enter stage 2-the "getting paid" part of the cycle where stock prices are less dependent on earnings and more driven by rising PE valuations. (Perspective Update 12-27-2012)

We cannot predict but we analyze available information. As always we appreciate your confidence in our work and look forward to a New Year.

Be sure to call us if you have any questions.

Best Wishes,

Jim Tillar, CFASteve Wenstrup

This electronic message transmission contains information from Tillar-Wenstrup Advisors, LLC., which may be confidential or privileged. The information provided in this report should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities listed herein will remain in an account's portfolio at the time you receive this report. It should not be assumed that any of the securities holdings listed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable. In addition we do necessarily agree with or endorse any outside commentary within this newsletter. If you have received this electronic transmission in error, please notify us by telephone (937) 428-9700 or by electronic mail [email protected]. Chart source: Wells Capital Management 12-27-2012. Tillar-Wenstrup does not warrant or endorse any outside commentary or guarantee its correctness.

© Tillar-Wenstrup