The fiscal cliff bill, formally titled “American Taxpayer Relief Act of 2012” (“Act”), was signed into law by the President on January 3. The Act extends certain tax relief provisions enacted in 2001 and 2003, and contains numerous other tax provisions. Of particular note for individuals, the Act:

- Extends the Bush-era tax cuts for individuals earning under $400,000 annually and under $450,000 for married couples filing jointly;

- Provides a permanent patch for the alternative minimum tax (AMT);

- Sets the top federal estate, gift and generation-skipping transfer tax rate at 40%, with a $5 million exemption, adjusted for inflation; and

- Taxes dividends and capital gains at 20% for individuals earning over $400,000 and married couples filing jointly with an income over $450,000.

Many of the tax provisions in the Act will be permanent, and may offer individuals and their planners more certainty than recent history has provided. However, it is possible that Congress will tackle comprehensive tax reform in late 2013 or 2014 to raise needed revenues. Key provisions of the Act include:

Individual Income Tax

Permanently extends income tax rates for certain taxpayers

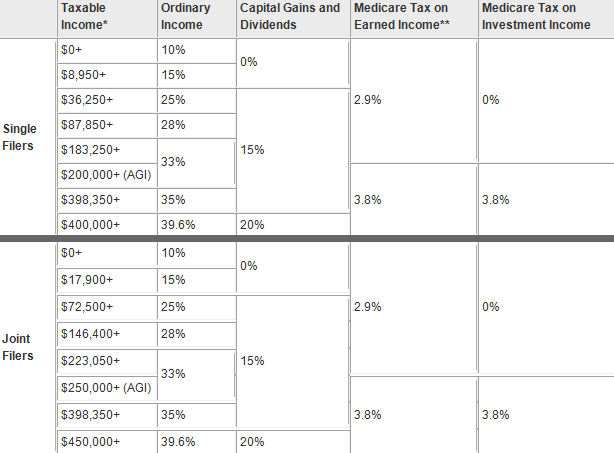

Under the new law, the 10%, 25%, 28%, 33% and 35% individual ordinary income tax brackets will continue to apply on income at or below $400,000 (individual filers), $425,000 (heads of households) and $450,000 (married filing jointly). A new rate of 39.6% will apply to taxable income in excess of these thresholds.

Permanent marriage penalty relief

Generally, taxpayers itemize deductions if the total deductions are more than the standard deduction amount. The new law makes permanent the repeal of the itemized deduction limitation for incomes at or below $250,000 (individual filers), $275,000 (heads of households) and $300,000 (married filing jointly) for taxable years beginning after December 31, 2012.

Permanent repeal of personal exemption phase-out for certain taxpayers

Under the new law, the 10%, 25%, 28%, 33% and 35% individual ordinary income tax brackets will continue to apply on income at or below $400,000 (individual filers), $425,000 (heads of households) and $450,000 (married filing jointly). A new rate of 39.6% will apply to taxable income in excess of these thresholds.

Higher-income taxpayers will see a limitation of their itemized deductions computed by reducing the taxpayer's otherwise allowable itemized deductions by 3% of the amount by which the taxpayer's adjusted gross income exceeds the applicable threshold. However, the reduction of itemized deductions cannot be reduced by more than 80%. It is worth noting that certain items such as medical expenses, investment interest and casualty, theft or wagering losses are excluded from this limitation.

Alternative Minimum Tax

An AMT patch has been put in place retroactively to cover 2012 and future tax years. Prior to the new law, taxpayers would have received an exemption of $33,750 (individuals) and $45,000 (married filing jointly) under the AMT. Additionally, the prior law did not allow for nonrefundable personal credits against the AMT. The new law increases the exemption amounts for the 2012 tax year to $50,600 (individuals) and $78,750 (married filing jointly) and provides for an annual inflation adjustment thereafter. Further, it allows taxpayers to apply nonrefundable credits, such as the child tax credit (which reduces one's tax liability dollar for dollar) against their AMT liability.

Long-Term Capital Gains and Qualified Dividend Tax Rate

Long-term capital gains and qualified dividend tax rates for taxpayers below the 25% bracket were equal to 0%, but set to rise in 2013 with the sunset of the Bush-era tax cuts. For those in the 25% bracket and above, the long-term capital gains and qualified dividend rates were set at 15%. The new law extends those rates for long-term capital gains and qualified dividends rates on income at or below $400,000 (individual filers), $425,000 (heads of households) and $450,000 (married filing jointly) for taxable years beginning after December 31, 2012. For income in excess of $400,000 (individual filers), $425,000 (heads of households) and $450,000 (married filing jointly), the rate for both long-term capital gains and qualified dividends will be 20%.

2013 Individual Income Tax Rates

Estate and Gift Taxes

Unified Transfer Tax Exemption Amount and Rates

The new law has made permanent the federal estate, gift and generation-skipping transfer tax exemption amount of $5 million per person, indexed for inflation beginning in 2012. The exemption amount, indexed for inflation, is projected to be $5,250,000 for 2013. The Act sets the top federal estate, gift and generation-skipping transfer tax rate at 40%. This is up from the top federal tax rate of 35% in 2012 (but is less than the 55% rate that had been scheduled to go into effect on January 1, 2013). The law makes the top federal tax rate permanent and applies to estates of decedents dying after December 31, 2012, and for gifts made after December 31, 2012.

Portability

The Act also makes permanent “portability,” the ability of an executor of a deceased spouse's estate to transfer any of the deceased spouse's unused federal estate and gift tax exemption to the surviving spouse for estates of decedent's dying after December 31, 2012. However, the Act did not extend portability to the generation-skipping transfer tax.

New York State Issues

For clients domiciled in New York State, it is important to keep in mind that, while the state does not impose a gift tax, it does impose an estate tax with an estate tax exemption amount of only $1 million per person. In addition, portability currently does not apply for New York State estate tax purposes.

Medicare Surtax

Beginning January 1, 2013, provisions from the Patient Protection and Affordable Care Act will go into effect. Specifically, the 3.8% Medicare surtax on investment income will apply to individuals with modified adjusted gross income (“MAGI”) in excess of $200,000 if single or $250,000 if married filing jointly.

The surtax is an additional tax on investment income. Depending on the investor's MAGI, the surtax will trigger four different marginal rates on long-term capital gains and qualified dividends: 0%, 15%, 18.8% and 23.8%. Taxpayers subject to the highest income tax rate of 39.6% will pay a marginal rate of 43.4% on ordinary investment income with the surtax.

For individuals, the 3.8% surtax is imposed on the lesser of (1) net investment income for the tax year or (2) MAGI above the threshold amount in that year, allocable to such income. For purposes of the surtax, investment income includes dividends, interest, rents, capital gains, annuities royalties and passive activity income.

Wages over $200,000 if single or $250,000 if married filing jointly will be subject to a Medicare surtax of 0.9%, beginning January 1, 2013. If appropriate Medicare taxes are not withheld by the employer, the balance due will be computed with the filing of an individual's Form 1040. This surtax increases the total Medicare taxes paid on wages to 3.8% when considering the 1.45% Medicare tax already being paid via withholding on wages earned by the employee, as well the 1.45% Medicare tax being paid by the employer on the same wages.

The amount of medical expenses a taxpayer may deduct is affected by this tax act as well. Beginning with the 2013 tax year, the itemized deduction floor on medical expenses will increase to 10% of AGI from 7.5% of AGI, causing a decrease in the amount of medical expenses that may be deducted on an individual's income tax return.

Other Relief Provisions Impacting Individuals

Deduction of state and local general sales taxes

The new law extends for two years (2012 and 2013) the election to take an itemized deduction for state and local general sales taxes in lieu of the itemized deduction permitted for state and local income taxes, which is of particular interest to individuals living in states without income taxes.

Extension of provision encouraging contributions of capital gain real property for conservation purposes

The law extends for two years (2012 and 2013) the increased contribution limits and carry-forward period for contributions of appreciated real property (including partial interests in real property) for conservation purposes.

Extension of tax-free distributions from individual retirement plans for charitable purposes

The law extends for two years (2012 and 2013) the provision that permits tax-free distributions by individuals, 70 1/2 or older, to public charities from an Individual Retirement Account (IRA) of up to $100,000 per taxpayer, per taxable year. This distribution to charity may count toward the individual's required minimum distribution amount.

Of note: Due to the late timing of the extension, the new law allows individuals to make charitable transfers during January of 2013 and treat them as if they were made during 2012. It also allows taxpayers to treat an IRA distribution made in December 2012 as a charitable distribution, if the taxpayer transfers cash to charity before February 1, 2013.

Extension of special rule for S corporations making charitable contributions of property

The new law extends for two years (2012 and 2013) the provision allowing S corporation shareholders to take into account their pro rata share of charitable deductions even if these deductions would exceed the shareholder's adjusted basis in the S corporation.

IRS Circular 230 Disclosure:

Please be advised that any discussion of U.S. tax matters contained within this communication (including any attachments) is not intended or written to be used and cannot be used for the purpose of (i) avoiding U.S. tax-related penalties or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.

This material is presented solely for informational purposes and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation or solicitation to buy, sell or hold a security. Before acting on any advice or recommendation in this material, you should consider whether it is suitable for your particular circumstances and, if necessary, seek legal, tax or other professional advice. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole. Investing entails risks, including possible loss of principal.

Tax, trust and estate planning are services offered by Neuberger Berman Trust Company. “Neuberger Berman Trust Company” is a trade name used by Neuberger Berman Trust Company N.A. and Neuberger Berman Trust Company of Delaware N.A., which are affiliates of Neuberger Berman Group LLC. Neuberger Berman LLC is a Registered Investment Advisor and Broker-Dealer. Member FINRA/SIPC.

The "Neuberger Berman" name and logo are registered service marks of Neuberger Berman Group LLC.

The "Neuberger Berman" name and logo are registered service marks of Neuberger Berman Group LLC. Neuberger Berman LLC is aRegistered Investment Advisor and Broker-Dealer. Member FINRA/SIPC.

© 2013 Neuberger Berman LLC. All rights reserved.