Stocks Rise on Earnings, Economic Data

In the lead up to a long holiday weekend, marked by the Presidential Inauguration, equity markets moved consistently higher throughout the week. The S&P 500 Index gained 0.9% and the Dow Jones Industrial Average picked up 1.2%.

Amongst an improving backdrop for corporate earnings, investors were also pleasantly surprised by domestic economic reports. Positive news centered on housing, inflation, and consumer spending, while consumer sentiment was largely disappointing.

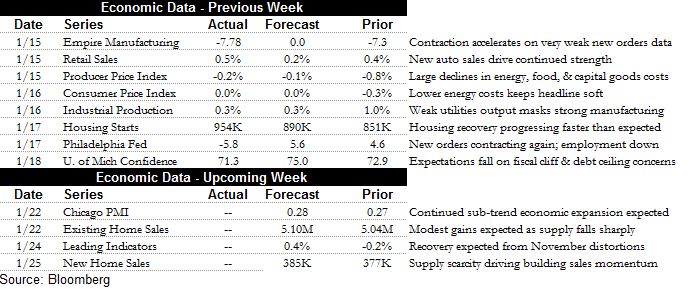

Retail sales for December posted a 0.5% gain, besting a 0.4% increase in November and a 0.2% drop in October. Strength in the final month of 2012 was partially attributable to vehicle sales, which climbed 1.6%. Gasoline station sales fell 1.6%, reflecting the softening of retail gas prices throughout the final months of the year. Excluding the impact of autos and gas, retail sales were up 0.6%, identical to the rate in November. Consumers spent in a broad-based way during the holidays, evidenced by strong gains in clothing, department stores, personal care, and furniture.

Consumers are unlikely to be as cheerful in the first quarter, however, after the recent expiration of payroll taxes shrinks take home pay. Remnants of that concern were reflected in consumer sentiment figures for mid-January, showing a 1.6-point fall since December. Consumers have been particularly downbeat within the expectations component of the index, which has fallen steeply since late 2012.

Many consumers will be encouraged by recent trends in housing markets, though. Housing starts rose 12.1% between November and December, and are now up 37% in the past year. Seasonally warm weather and rebuilding efforts from Hurricane Sandy were commonly cited reasons for the December pop.

Real estate firm CoreLogic released data showing that 1.4 million homeowners moved from negative to positive equity over the first three quarters of 2012. This still leaves 10.7 million property owners in a state of negative equity and another 2.3 million at near-negative equity (5% or less equity in their home). The trend has improved, but it is clear that many homeowners are still impacted.

Source: Calculated Risk Blog

Following a long bottoming out process in 2009 and 2010, housing starts have been on a consistent path towards recovery. Low levels of inventory and improving consumer credit metrics will undoubtedly bolster housing markets in the quarters ahead.

The final bit of positive news came in the labor markets, where the number of initial claims for unemployment insurance fell to January 2008 levels. Roughly 335,000 individuals filed for unemployment in the week ending January 12. Improvement in the labor markets has been slow, but recent reports suggest the improvement is quickening.

Is the European Crisis Over?

The European sovereign debt crisis that first erupted in 2010 and stoked almost three years of intense market volatility has all but faded from the front pages. Overshadowed by domestic policy issues and European Central Bank (ECB) President Mario Draghi’s pledge to do “whatever it takes” to save the Eurozone, fears that the monetary union would crumble and unleash a maelstrom of financial distress appear to have dissipated.

Since Draghi’s famous “bumble bee” speech on July 26, European risk assets have experienced a remarkable rally. The MSCI Europe index is up 22%, with financial stocks rising an astounding 45% in that period. Yields on sovereign debt spreads have also tightened, with the debt of troubled borrowers like Spain and Italy coming in more than 200 bps since the summer. The relief in funding pressures allowed Spain and others to avoid tapping into the ECB’s Outright Monetary Transactions (OMT) program, whereby the bank would directly recapitalize troubled sovereigns.

The euro, too, has rallied. Calls for the currency to reach par with the US dollar now seem like a distant memory. The denomination has strengthened by 7% against the greenback and 20% against the Japanese yen since July, reflecting improving sentiment for the union’s prospects. It was not long ago that many investors could justifiably contemplate whether the denomination would survive.

Asset prices have climbed the so-called wall of worry over the past six months, but is there really nothing to worry about anymore?

Structurally, it is tough to see what has really changed. Leverage in the European public sector remains astronomical. Ireland, Italy, and Portugal sport debt-to-GDP ratios well in excess of 100%, while Spain’s stands at approximately 77%. The overall debt-to-GDP ratio for the Eurozone continues to climb, reaching 90% in the third quarter of 2012.

Greece, the epicenter of the crisis, continues to miss deadlines for budget improvement imposed by its troika of creditors – the IMF, ECB, and European Commission. The latest print shows Greece’s debt-to-GDP ratio stands at 153%.

Improvement in these metrics is a difficult prospect given the state of economic growth in Europe. The region is already in recession, with major economies like Spain, Italy, and France contracting in 2012. The strength of stalwart economy Germany has also come into question, as the country expects meager GDP growth of 0.7% in the fourth quarter. The country’s robust manufacturing sector is under pressure, with the latest PMI down to 46.0 and industrial production shrinking 2.9% in the past 12 months. The rally in the euro will also present a headwind for an economy dominated by its export complex.

The latest forecasts for 2013 predict continued recession in Europe. The IMF’s World Economic Outlook predicts an aggregate 0.1% contraction in 2013, following an expected 0.7% contraction in 2012. A survey of economists aggregated by Bloomberg also sees the Eurozone’s economy shrinking by 0.1% this year.

Lackluster growth is sparking concerns that the region’s austerity centric approach is failing to reduce sovereign indebtedness. A recent study by the IMF noted that their economists underestimated the multiplier effect of fiscal austerity on economic growth. While forecasters initially worked under the assumption that a 0.5 fiscal multiplier would be in effect, subsequent research has shown the multiplier to be closer to 1.5. This implies that for every $1 cut in government spending, the economy is losing $1.50 in output.

Meanwhile, policy initiatives have yielded only incremental progress. The region’s bailout fund, or European Stability Mechanism (ESM), is scheduled to come online in mid 2013. But squabbling over how to fund the program persists. As of the end of 2012, the Fund housed approximately just a fraction of the €500 billion lending capacity available for troubled sovereigns. Even when fully funded, the mechanism’s capacity to actually bail out a nation as large as Spain or Italy is in question. Some estimates peg those countries’ financing needs in 2013 and 2014 at €670 billion. The potential liability is clearly larger, with continued weakness in countries like Portugal and Greece; France also lurks as a more serious threat. Despite their vow to not fund the deficits of debtor nations, the ECB remains the lender of last resort for the region.

The recently agreed upon banking union also has serious flaws. Political leaders have determined that the ECB will act as a singular banking authority for only the largest institutions in the monetary union. Small institutions remain under the purview of the national regulators. But the link between the sovereign and its banks remains, as the local authority will be responsible for backstopping any failing banks – precisely the problem that has belied the crisis for much of the past three years. Indeed, The Economist labeled the resolution “a measly triumph.”

Despite these grim realities, investors should take stock in the fact that global sentiment toward Europe has improved. Much as any bank depends on the faith and confidence of its depositors to continue operations, Europe’s financial system succeeds or fails based on the confidence of market participants. Improvement in sentiment has reduced stress in the system as capital has returned to the region’s financial institutions. This certainly buys Europe more time to right its many structural issues, but the relative calm does beg the question: how quickly will politicians move to act, now that their feet are no longer held to the fire? Europe could return to the front pages quickly if this borrowed time runs out.

the week ahead

The coming week holds plenty of announcements to digest. Existing home sales for December are released Tuesday, while new home sales data follows on Friday. Various regional manufacturing reports are released throughout the week.

On the corporate front, numerous companies report earnings, including notables such as Google, Delta, DuPont, IBM, Johnson & Johnson, Apple, Netflix, Lockheed Martin, Starbucks, and Procter & Gamble.

Globally, the topic du jour will be the World Economic Forum in Davos, Switzerland. A number of corporate and political luminaries gather to discuss the state of world affairs. The event is widely reported on, but rarely results in new proposals.

Central bankers will be busy with 10 central banks announcing policy decisions, including Canada, Argentina, Turkey, Japan, and South Africa.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

For more information, please visit our website at http://www.Fortigent.com.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent