Feeding the Dragon: Why China's Credit System Looks Vulnerable

Prologue

For GMO’s asset allocation team, valuations are our first protection against losses. We generally believe that cheaper assets are more resilient against bad economic and financial events, and that if we focus on avoiding the overvalued assets, we should not only achieve higher returns over time, but more often than not do less badly when markets encounter difficulty.

From a valuation perspective, Chinese equities do not, at first glance, look to be a likely candidate for trouble. The PE ratios are either 12 or 15 times on MSCI China, depending on whether you include financials or not, and the market has underperformed MSCI Emerging by about 10% over the last three years (ending December 31, 2012). Neither of these characteristics screams “bubble.” And yet, China has been a source of worry for us over the past three years and continues to be one, affecting not merely our behavior with regards to stocks domiciled in China but the entire emerging world, as well as some specific developed market stocks, which we believe are particularly vulnerable should things in China go down the road we fear it might.

China scares us because it looks like a bubble economy. Understanding these kinds of bubbles is important because they represent a situation in which standard valuation methodologies may fail. Just as financial stocks gave a false signal of cheapness before the GFC because the credit bubble pushed their earnings well above sustainable levels and masked the risks they were taking, so some valuation models may fail in the face of the credit, real estate, and general fixed asset investment boom in China, since it has gone on long enough to warp the models’ estimation of what “normal” is.

Our fears have not stopped us from buying emerging stocks, or indeed some Chinese stocks, but they have tempered our positions relative to what they would be if we were not concerned about the bubbly aspects of China. Because this view has a real effect on our portfolios, it is important for us to continue to update our work to make sure we aren’t missing something important. The recent apparent strengthening of the Chinese economy is a potential challenge to our thesis, and as a result, Edward and others at the firm have been working hard to understand what is driving the rebound and understand whether it is sustainable or not. “Feeding the Dragon” looks at the utterly crucial issue of funding in China’s very credit-dependent economy.

Ben Inker, January 22, 2013

Introduction – The Credit Tsunami

Until the summer of 2011, China’s economic juggernaut seemed unstoppable. In September of that year, however, an acute credit crunch appeared in the city of Wenzhou on China’s eastern coast. Stories suddenly appeared of defaulting property developers, loan sharks disappearing in the middle of the night, work halted on half-completed apartment blocks, luxury cars abandoned in droves, property prices plunging, and credit drying up. China’s high-speed economy appeared to be running off the tracks.

* With special thanks to our colleague Eric Ikauniks for his insights.

Such fears have proven unfounded. Last year, the property market – perhaps the most important driver of Chinese economic growth – staged a remarkable recovery. Credit growth has also picked up strongly. As memories of Wenzhou fade, conventional wisdom holds that Beijing has pulled off yet another soft landing. Even if credit problems re- emerge, it’s widely believed that a number of policy options remain open: the PBOC can free up some RMB 18 trillion of bank credit by cutting the reserve ratio requirement.1 Regulators can also relax the cap on the banks’ loan to deposit ratio. And interest rates can be cut further. If need be, Beijing can simply borrow more. There’s no near-term limit to China’s financial capacity.

This white paper presents a brief account of China’s great credit boom and outlines some worrying recent developments in the financial system. In our view, China’s credit system exhibits a large number of indicators associated with acute financial fragility. These include:

- Excessive credit growth (combined with an epic real estate boom)

- Moral hazard (i.e., the very widespread belief that Beijing has underwritten all bank risk)

- Related-party lending (to local government infrastructure projects)

- Loan forbearance (aka “evergreening” of local government loans)

- De facto financial liberalization (which has accompanied the growth of the shadow banking system)

- Ponzi finance (i.e., the need for rising asset prices to validate wealth management products and trust loans)

- An increase in bank off-balance-sheet exposures (masking a rise in leverage)

- Duration mismatches and roll-over risk (owing to short wealth management product maturities)

- Contagion risk (posed by credit guarantee networks)

- Widespread financial fraud and corruption (from fake valuations on collateral to mis-selling of financial products)

Not only does financial fragility look to be on the rise, Beijing seems to be on the verge of losing control over the credit system. Savings are migrating from deposits in the state-owned banking system to higher-yielding nonbank credit instruments. Furthermore, rich Chinese are increasingly willing to evade capital controls and take their money out of the country. As a result of these developments, deposits in the banking system are becoming less stable. “Red Capitalism,” namely the ability of the Chinese authorities to direct the country’s enormous savings for their own ends, faces an existential threat.

A Credit Bubble

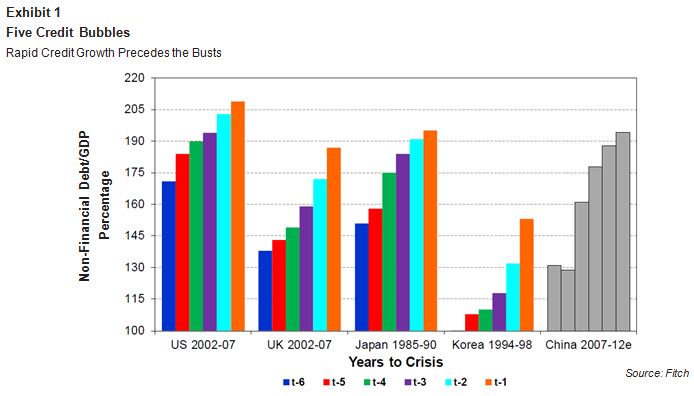

Economists have woken up to the fact that periods of rapid credit growth generally end badly. As one recent paper puts it, “credit [growth] matters, and it matters more than broad money, as a useful predictor of financial crisis.”2 China today seems to be in a similar predicament to several of the developed economies prior to 2008. Too much credit has been created too quickly. Too much money has been poured into investments that are unlikely to generate sufficient cash flows to pay off the debt. Last year, for instance, new credit extended to the non-financial sector amounted to RMB 15.5 trillion.3 That’s equivalent to 33% of 2011 GDP, although as Fitch Ratings notes, overall credit formation is running at an even faster rate when items missing from the official data are added in.4

The latest surge of credit follows the great tsunami of 2009, when China’s non-financial credit expanded by the equivalent of 45% of the previous year’s GDP. Since that date, China’s economy has become a credit junkie, requiring increasing amounts of debt to generate the same unit of growth. Between 2007 and 2012, the ratio of credit to GDP climbed to more than 190%, an increase of 60 percentage points. China’s recent expansion of credit relative to GDP is considerably larger than the credit booms experienced by either Japan in the late 1980s or the United States in the years before the Lehman bust (see Exhibit 1).

Most China commentators believe that rapid credit growth in China is not worrying because the debt is funded by domestic savings rather than by foreigners. The historical record, however, suggests that current account deficits don’t increase the likelihood of a financial debacle in an economy where credit has been growing rapidly (for instance, Japan’s “bubble economy” of the 1980s was funded domestically).5

It has also been argued that China has nothing to fear because total non-financial credit, at roughly 200% of GDP, is relatively low by comparison with the U.S. and other developed economies. Yet the total stock of credit is less predictive of future problems than its rate of growth. Furthermore, mature economies appear to have a greater capacity to shoulder debt. In economists’ parlance, “financial deepening” is correlated with the level of economic development.

In fact, China is rather heavily indebted relative to other emerging markets and has roughly the same amount of debt as Japan sported in the late 1980s (even though Japan’s per capita income at the time was much higher, as shown in Exhibit 2).

Many commentators also take comfort from the fact that China’s public debt is less than 30% of GDP. The trouble is that the official numbers are misleading. As is often the case in China, most of the debt is kept off balance sheet. Because the main banks are state-controlled and most of their lending is directed at state-controlled entities, a great deal of bank lending is quasi-fiscal in nature. In order to get a proper picture of China’s sovereign liabilities we must add back the loans to local government infrastructure projects, policy bank debt (issued by the likes of the China Development Bank), borrowings by the asset management companies (which acquire non-performing loans from banks and others), and debt issued by the Ministry of Railways to fund the roll-out of the expensive high-speed rail network.

When these on- and off-balance-sheet liabilities are combined, China’s public debt approaches 90% of GDP. Significantly, this is considered by economists to be an upper threshold for public indebtedness.6 Higher levels of public debt are associated with a prolonged decline in economic growth. Economist Andrew Hunt estimates that China’s true public debt has increased by around 60% of GDP since 2007. If Beijing were to attempt to repeat the credit-fuelled stimulus package of 2009, its true debt-to-GDP ratio would exceed that of Greece.

Debt and the Real Estate “Bubble”

Recent research suggests that credit booms are more likely to end in severe busts when they coincide with property bubbles.7 It’s difficult to prove using purely quantitative tools that China’s property market is in a bubble. There’s no doubt, however, that China has witnessed a tremendous residential construction boom in recent years. Miles upon miles of half-completed apartment blocks encircle many cities across the country. Official data suggest that the value of the unfinished housing stock is equivalent to 20% of GDP and rising.

Real estate collateral supports much of the country’s outstanding debt. Officially, the banks’ exposure to property

- through loans to developers and mortgages – is only 22% of their total loan book. The banks, however, are also exposed to real estate through their loans to local government funding vehicles and through sundry off-balance-sheet credit instruments. It’s probably fair to say that at least one-third of bank credit exposures are real estate related.

Developments in the infamous “ghost city” of Ordos, in Inner Mongolia, reveal the vulnerability of China’s credit system to an overblown housing market. The Kangbashi district of Ordos is a totem for China’s property excesses. Kangbashi has enough apartments to shelter a million persons, roughly four times its current population. Until recently, turnover in the local real estate market appears to have been driven by debt-fuelled speculators. Construction in Ordos came to a sudden stop in the fall of 2011 after property prices collapsed (Caixin magazine reports incredibly that prices declined by 85%). More than 90% of the building sites in Kangbashi were said to be idle.8

Debt problems soon emerged. A prominent developer in the neighboring city of Baotou hanged himself last June, leaving behind debts of RMB 700 million, according to the National Business Daily. Local property developers were revealed to have funded themselves in the underground loan market, where monthly interest rates range between one and three percent. The city government has run into difficulties after revenues from land sales fell by three-quarters. Local banks also reported an increase in non-performing loans.

Property-related debt problems have cropped up in other cities. In late 2011, funding difficulties at a Hangzhou-based real estate developer imperiled dozens of companies that had issued guarantees over its debts. Property trusts in Nanjing and Beijing have recently threatened to default. Last October, developers in the city of Changsha in Hunan province were reported to have both reneged on debts and sold the same properties to different buyers.9 Given the vast amount of residential construction in China (estimated at around 12% of GDP) and severe weakness in many property markets, it’s remarkable that real estate lending issues have been relatively contained.

Local Government Funding Vehicles

Moral hazard, or the belief that the government is underwriting financial risk, is another common feature of unstable banking systems. In China, the issue of moral hazard is accentuated by the state’s control of both the leading banks and the main recipients of credit, namely the state-owned enterprises. These arrangements have encouraged crony lending practices and the concealment of non-performing loans. In this respect, China combines the poor lending practices of the Indonesian banking system during the corrupt Suharto era with the propensity to roll over or “evergreen” non- performing loans, which was a marked feature of the Japanese banking system after its property and stock market bubble burst in 1990.

In recent years, the problems of moral hazard, related-party lending, and loan forbearance have been particularly prevalent in the area of local government finance. Local governments in China are restricted in their ability to borrow on their own account. To get around this law, they set up platform companies, commonly referred to as local government funding vehicles (LGFVs), to finance their investment activities. Loans to these platform companies mushroomed in 2009 and 2010 as the banks financed China’s infrastructure-heavy economic stimulus. The People’s Bank of China estimated LGFV debt at RMB 14.4 trillion, while China’s banking regulator came up with a figure of RMB 9.1 trillion. On these numbers, LGFV debt accounts for between 15% and 25% of outstanding loans in China’s banking system.

Although ostensibly commercial entities, much of the money spent by these infrastructure companies appears to have been wasted on extravagant trophy projects. The quality of the collateral held by the banks against their loans has been questioned. Collateral often comes in the form of land, which in some cases has been valued by local officials at a premium to actual market values. Moreover, guarantees issued by local governments in respect of LGFV debts may not be of much use. Not only is their legal basis dubious, these promises depend on continuing land sales. Because land sales and development taxes account for a large chunk of local government revenue, when the real estate market turns down, local governments in China face a potential cash crunch.

Loudi, a little-known city in Hunan province, serves as the poster child for LGFV excesses. According to Bloomberg, Loudi’s local government borrowed RMB 1.2 billion to finance the construction of a 30,000-seat faux Olympic stadium, gymnasium, and swimming complex. The land collateral for Loudi’s loan was valued at around four times the value of nearby plots zoned for commercial use.10

Early evidence that platform companies were struggling to repay their debts emerged in April 2011 when the Yunnan Highway informed its banks that it couldn’t meet the repayment schedule on RMB 100 billion of loans.11 In the summer of 2011 China’s banking regulator rescinded a previous instruction to the banks not to roll over non-paying local government loans. Since then, problems with LGFV loans have largely remained out of the headlines. As the banks’ balance sheets are laden with non-paying loans, capital is tied up that might otherwise have supported the extension of new credit to other entities. In the long run, the consequences of “evergreening” non-performing loans will be slower economic growth.

Shadow Banking

Although Beijing maintains a tight grip over the lending of the Big Four banks (Bank of China, China Construction Bank, Industrial and Commercial Bank of China, and Agricultural Bank of China), the most notable feature of the credit boom has been the rapid expansion of nonbank lending, in particular of so-called wealth management products. The explosive growth of China’s shadow banking system represents a de facto liberalization of the financial system. In a number of countries, financial liberalization has been associated with asset price bubbles and has been a leading indicator of banking crises (e.g., the appearance of the secondary banks in the U.K. in the early 1970s and the deregulation of the Nordic banks in the late 1980s).

Last year, Chinese banks’ share of total lending fell to only 52% of total credit creation, down from 92% a decade ago. In the fourth quarter of 2012, nonbank lending accounted for an astonishing 60% of new credit issuance. China’s thriving shadow banking system has much in common with the American version, which thrived before Lehman’s collapse: trust loans that finance cash-strapped property developers have a whiff of the subprime about them; wealth management products that bundle together a miscellany of loans, enabling the banks to generate fees while keeping loans off balance sheet, bear a passing resemblance to the structured investment vehicles and collateralized debt obligations of yesteryear; while thinly capitalized providers of credit guarantees are reminiscent of past sellers of credit default insurance.

Corporate Bonds and Trust Products

After China’s economy turned down in early 2012, there were calls for another economic stimulus. The banks, however, were reluctant to add to their LGFV exposure. So the local governments turned to the bond markets. Restrictions on the platform companies’ ability to issue bonds were relaxed, and a corporate bond boom was soon underway. Over the course of 2012, RMB 2.3 trillion of corporate bonds were issued in China, an increase of 64% on the previous year. Almost half of the funds raised went to local governments (see Exhibit 3).

In the past, China’s banks have purchased most new corporate bond issuance. This time, however, an increasing number of bonds have been bundled into wealth management products, which are sold on to the banks’ retail and corporate clients. Caixin quotes a source at a major bank claiming that many bonds, which purported to finance new infrastructure projects, were actually being used to pay off old bank debts.12 While this has allowed banks to reduce their reported exposure to local governments, it is possible they will have to make good any future losses suffered by investors on future bond defaults.

The worst investment decisions have generally been made when dumb money is chasing yield. Chinese savers who are looking for something more satisfying than the negative real interest rates available on bank deposits often end up choosing trust products. Borrowers whose operations are too risky for banks often resort to a trust company. However, over the last year LGFVs have emerged as the dominant borrower from trust companies.13 China’s trust industry has more than doubled in asset size over the past two years, controlling some RMB 6.0 trillion of assets at end September 2012.14 Given their generally low credit quality and widespread exposure to real estate, trust products can be seen as

China’s equivalent to subprime mortgage-backed securities.

Problems with the assets backing trust products are well documented. Bloomberg recently reported on the “Purple Palace,” a half built and abandoned luxury development in Ordos, which had been funded with trust loans.15 Trust investors, however, believe they are protected against loss. Because trust companies can lose their operating license if they impose losses on investors, they tend to make good any shortfalls with their own capital. The trouble is that trust operators are highly leveraged. The average leverage of the trust companies – defined as trust balance divided by net assets of the trust company – was 24 times, according to Yongi Trust Research Institute.16

To date, problems associated with trust products have largely been concealed from public scrutiny. Last year, a state- run asset management company, China Huarong, took over two property trusts that were on the verge of defaulting. Industry insiders have also alleged that on occasion the proceeds from new trusts have been used to pay off maturing loans.

Wealth Management Products

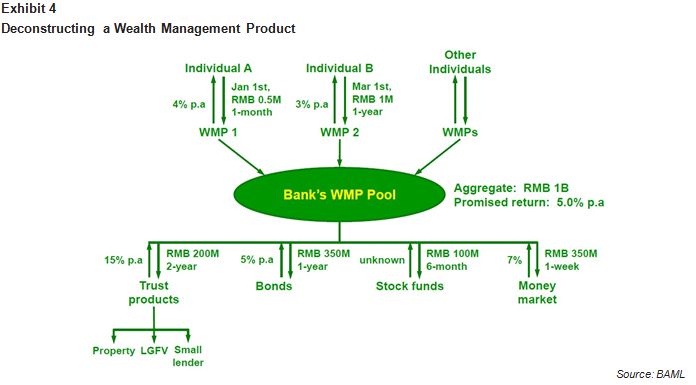

Wealth management products (WMPs) have been by far the most popular investment for Chinese savers looking for higher returns. These securities yield on average around 2 percentage points more than bank deposits, and are sold by banks to retail investors as low-risk investments. Ratings agency Fitch estimated that around RMB 13 trillion of WMPs were outstanding by the end of 2012, an increase of over 50% on the year.17

WMPs share some of the characteristics of both the Structured Investment Vehicles (SIVs) and Collateralized Debt Obligations (CDOs), which were used by U.S. banks before 2008 to keep loans off balance sheet. Central to the structure is the pooling of investor funds. Money raised from the sale of several different WMPs is aggregated into a general pool (see Exhibit 4). The general pool then funds a variety of assets, investing across the risk spectrum. Some money goes into trust products and LGFV bonds described earlier in this paper, and some is invested in less risky interbank loans.

These credit instruments pose a number of different problems. They often create a duration mismatch, as short-dated funds are invested in longer-dated assets, such as trust products supporting real estate development. Many WMPs are as opaque as the old SIVs and CDOs. The documentation provided to investors is typically short on detail with regards to the mix of assets funded. Some WMPs resemble blind trusts in which savers hand over their money without knowing what exactly they are investing in. A recent WMP sold by China Construction Bank, for instance, merely stated that it would invest up to 70% of the funds in debt and at least 30% in bonds and money market instruments.

WMPs contain a further twist. The buyers are typically required to sign a confirmation – which can be as simple as ticking a box on an online application – that they will bear the financial shortfall if assets funded by the pool fail to generate the expected returns. And, to be clear, most WMPs advertise “expected” rather than guaranteed or promised returns. So long as the returns are not guaranteed, WMP providers are able to hold off balance sheet both the liabilities raised from investors and the assets funded by them. Once again, buyers appear ignorant of the risks. Most likely, they assume that the issuing banks will backstop them should the funded assets fail to pay. After all, banks have their reputations to consider. They would be leery of starting a run on their WMP assets. And the government could be expected to lean upon them.

Ponzi Finance

Within China, some highly-placed officials have started raising concerns. “Many assets underlying the [wealth management] products are dependent on some empty real estate property or long-term infrastructure, and are sometimes even linked to high-risk projects, which may find it impossible to generate sufficient cash flow to meet repayment obligations,” Xiao Gang, chairman of the Bank of China, wrote in the China Daily in October.18 “China's shadow banking is contributing to a growing liquidity risk in the financial markets…[I]n some cases short-term financing has been invested in long-term projects, and in such situations there is a possibility of a liquidity crisis being triggered if the markets were to be abruptly squeezed.”

Xiao touches next upon a key vulnerability of WMPs. “In fact, when faced with a liquidity problem, a simple way to avoid the problem could be through using new issuance of WMPs to repay maturing products. To some extent, this is fundamentally a Ponzi scheme,” he writes. “Under certain conditions, the music may stop when investors lose confidence and reduce their buying or withdraw from WMPs.”

These comments were well-timed. Salesmen employed by banks have reportedly earned commissions by selling third-party products without their employers’ knowledge.19 Customers appear to have bought these third-party WMPs believing they came with a bank guarantee. In early December, the Shanghai branch of Huaxia Bank was beset by protesters after a WMP sold at the branch defaulted.20 This incident was the first in a number of scandals concerning shadow banking credit. In the same month, customers at a branch of China Construction Bank in the northeastern province of Jilin claim to have been sold a WMP with guaranteed returns but suffered a loss of 30% of their principal.21 Citic Trust Co, a unit of China’s biggest state-owned investment company, recently missed a bi-annual payment to investors on one of its trust products after a steel company missed interest payments on the underlying loan.22

As might be expected, sell-side analysts have reacted blithely to risks posed by shadow banking securities. A study by Merrill Lynch highlights so-called “collective trusts” – a type of high-yielding WMP originated by trusts rather than banks – as the most subprime-like subsector, but notes they are limited in size to RMB 1.7 trillion. “The risk for a systematic liquidity crunch seems very low for now,” Merrill concludes. While another broker concedes that “some collateral is used twice by different institutions,” he suggests that only 5% of loan-backed WMPs are likely to go bad.23 We are less sanguine. In our view, WMPs are providing a lifeline for the most marginal of borrowers.

Other Chinese Credit Curiosities

Credit guarantees

If the proliferation of WMPs in China’s financial system follows the originate-and-distribute model for credit popular in the U.S. prior to 2008, a further echo of the subprime era is sounded by China’s extensive network of credit guarantees. China’s credit guarantee businesses have enjoyed a long boom. There were 8,402 of them guaranteeing RMB 1.3 trillion of debt at the end of 2011, according to Merrill Lynch.24 Providers of credit guarantees, like sellers of credit default insurance, earn a small fee for their service. The danger is that when credit guarantors operate with insufficient capital, their losses can spread contagiously throughout the system.

Around a quarter of all bank loans in China carry some form of guarantee. These guarantees may come in the form of a mutual guarantee, where one company guarantees another’s debts against default. Alternately, a guarantee can be purchased from a dedicated guarantee firm. The latter are financial services companies engaged solely in the business of issuing guarantees against default. They typically charge 3% of the loan amount.

Credit guarantees are popular because regulations governing interest rates prevent Chinese banks from pricing credit risk. As a result, the banks prefer to lend to state-owned firms. Smaller privately-held outfits require a guarantee in order to access bank finance. It is commonplace for companies with trading relationships to guarantee each other’s debts, simply to grease the wheels of commerce.

Wenzhou’s credit crisis, which commenced in the late summer of 2011, was propagated by the collapse of a network of credit guarantees – the city’s guarantee firms later had to be bailed out by the government. The failure of Tianyu Construction, a Hangzhou-based developer, a few months later created a “credit crisis threatening banks and financial institutions that altogether issued about RMB 6 billion in loans to scores of companies,” according to Caixin.25 Sixty-two companies, “from furniture makers to import-export traders…were financially linked to Tianyu through a province-wide, reciprocal loan-guarantee network.”

As with sellers of credit default insurance in the era before Lehman’s collapse, many providers of credit insurance in China are thinly capitalized and poorly regulated. Consider the case of Beijing-based Zhongdan Investment Credit Guarantee Company, which has guaranteed more than RMB 3 billion in outstanding loans to nearly 300 companies. “Some of these companies,” reports Caixin, “had borrowed from banks with Zhongdan's guarantee and invested the money not in their businesses but in the latter's so-called wealth management schemes, which promised high returns through murky operations. In some cases, fraudulent contracts were used by Zhongdan and its client companies to obtain bank credit, most likely with bank officers' acquiescence, the investigation found.”26

Collateralized lending

The American economist Hyman Minsky warned that financial stability was undermined when lending becomes overly linked to collateral values rather than income. “An emphasis by bankers on the collateral value and expected value of assets is conducive to the emergence of a fragile financial structure,” wrote Minsky in Stabilizing an Unstable Economy (1986). Lending against collateral has the potential to create both virtuous and vicious cycles; as collateralized credit supports asset prices in the boom phase, whilst in the bust falling collateral values create credit problems.

Collateralized lending is especially popular in China for the same reasons as credit guarantees – banks want collateral because they are not allowed to charge for risk. By our estimates, more than 40% of all bank loans outstanding are collateralized, with residential mortgages accounting for around half of this amount. A curious feature of Chinese credit practices is that various inputs to the residential housing bubble – including commodities, such as steel and copper, and construction equipment – are often used as collateral to back loans. Concrete producers have been noted to purchase equipment on easy credit terms in order to use the machines as collateral against bank loans to finance their working capital. More machines have been purchased than were needed for purely operational reasons.27

The demand for copper has reportedly been buoyed by Chinese speculators, who have raised loans against stockpiles of imported copper and invested the proceeds in the property market. The same practice afflicts the market for steel.

Last summer, Shanghai-based steel traders began defaulting on their loans after the steel price slumped. “Chinese banks and companies looking to seize steel pledged as collateral by firms that have defaulted on loans are making an uncomfortable discovery: the metal was never in the warehouses in the first place,” reports Reuters.28 “As defaults have risen in the world's largest steel consumer, lenders have found that warehouse receipts for metal pledged as collateral do not always lead them to stacks of stored metal.”

An End to Financial Repression?

For better or worse, financial capitalism as practiced in China is rather different from the Western variety. The large banks are run by members of the Chinese Communist Party who receive instructions on how to allocate credit from their Party superiors. Loans are made at the behest of Beijing to state-owned enterprises and local government funding vehicles to meet public policy purposes. Credit quality is not a main concern.

These arrangements tend to generate large numbers of bad loans. “Red Capitalism,” however, has worked in its fashion because the regulators have guaranteed the banks’ generous net interest margins – the spread between what the banks pay on deposits and receive on their loans. Large profit margins have compensated the banks for making unproductive loans and provided them with the cash to conceal subsequent losses.

Chinese savers who have historically received low interest rates (often negative in real terms) on their deposits have footed the bill. They are the victims of what economists call “financial repression.” Until recently, however, they had no alternative to leaving their cash in state-run banks and capital controls prevented them from taking money out of the country. The emergence of the shadow banking system changed this state of affairs. As we have seen, savers now earn more from investing in WMPs than keeping their money on deposit. Some property trusts offer double-digit returns. Braver hearts can venture into China’s usurious underground loan market. (As shown in Exhibit 5, in Wenzhou prior to the September 2011 crisis lenders were charging up to 80% annualized rates in the underground market.)

Competition from China’s shadow banking world creates a problem for the banks. Wealth management products are now around a fifth the size of the banks’ total loan book. As money flows into the shadow banking system, the banks have on occasion run short of deposits. For long stretches over the last year and a half, deposit growth has been insufficient to cover new loans. Furthermore, the inflows of deposits into the banking system are becoming more volatile. Every quarter, deposits flow out of the banks to purchase wealth management products. Three months later, the money returns briefly to the banking system as these securities mature. The returning deposits allow the banks to keep within their regulated loan-to-deposit ratio (current maximum 75%).

There’s a wrinkle, however. More than two-thirds of WMPs mature in three months or less. Yet these financial instruments are often invested in assets with much longer maturities, including trust loans whose maturities stretch out several years. This asset-liability mismatch makes it crucial for the banks to be in a position to roll over the loans. The numbers are enormous and getting larger by the day – every quarter around RMB 3 to 4 trillion of wealth management products need refinancing.

The banks have been forced to turn to the interbank market to finance the roll-over. Interbank assets within the Chinese financial system have grown to roughly RMB 28 trillion at the end of September 2012 (up from RMB 11 trillion at the end of 2009).29 They now comprise a quarter of total bank assets. Although China’s banks report low loan-to-deposit ratios, the banking system is now more reliant than ever on market liquidity.

The dubious creditworthiness of many WMP assets means that defaults are an ever present possibility. A loss of confidence in China’s shadow banking arrangements could threaten a full-blown credit crunch. China’s shadow banking system has grown too big to fail, but it may also have become too big to control. Beijing is caught between a rock and a hard place. Recent moves by policymakers suggest a desire to limit local government borrowing and regulate growth of WMPs. However, if the authorities were to crack down on the shadow banking system, they risk creating a “credit crunch by accident.”30 As a result, most regulatory pronouncements remain a dead letter.

Capital Flight

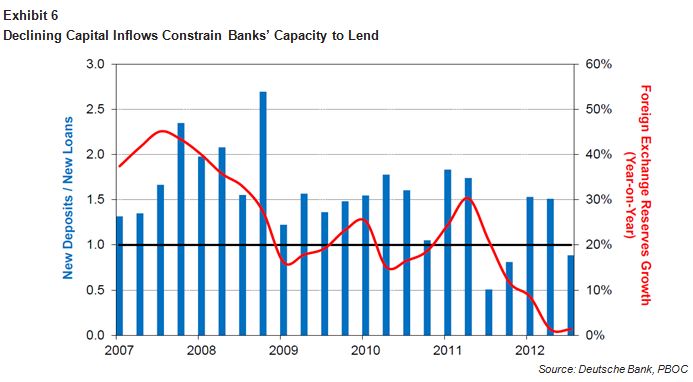

The state’s control over the credit system is threatened on another front. China’s vast trade surplus and substantial capital inflows over the last decade have required massive intervention by the central bank in order to maintain the exchange rate peg to the U.S. dollar. For every dollar entering the country, several new RMB have had to be printed. Capital inflows into China have thus boosted deposits in the banking system and underpinned the country’s credit boom. The corollary is that capital outflows would suck cash out of the banking system as savings fled the country. Exhibit 6 shows the ratio of new loans to new deposits moving in line with changes in China's FX reserves.

How realistic is the prospect of capital flight? Wealth is highly concentrated in China. Rich Chinese have many incentives to take their money out of the country – real estate is no longer a one-way bet, savings in the state- controlled banks continue to earn negative real rates, while the shadow banking system is stuffed with dodgy credits. There’s also a danger that the new administration may seek to appease the public’s anger toward rising inequality and corruption by confiscating windfall fortunes. The wealthiest 1% of households, according to Victor Shih of Northwestern University, control funds equivalent to two-thirds of China’s huge foreign exchange reserves.

If the wealthiest Chinese were to move a significant portion of their money offshore, liquidity in the banking system would be drained. Such a movement is already underway. The Wall Street Journal reckons that capital outflows in the twelve months through to September 2012 amounted to $225 billion.

The Art of Bank-Watching

There is a famous CIA paper, dating from the 1970s, entitled “The Art of China-Watching.” The anonymous author expresses frustration at the way in which important events in China are hidden from the eyes of Western observers and ends up by questioning whether logic even helps when analyzing Chinese affairs. An observer of China’s modern financial system is similarly handicapped and is in danger of reaching the same conclusion. Over the last year and a half, we have seen the sudden collapse in credit and, just as abruptly, a miraculous recovery.

There appears to be a large and growing gap between appearance and reality in China’s banking system. On the surface, China’s credit conditions are healthy. Yet the China-watcher gets an occasional glimpse of a rather different reality; of Ponzi finance practices across the financial spectrum; of loan sharks disappearing with the locals’ savings; of miscellanous entities exaggerating the value of their loan collateral and at times faking it; and of bank employees purloining funds from their banks or engaged in the mis-selling of financial products. China’s financial system simmers with incipient scandals.31

The public appearance is of a banking system with negligible levels of bad debts, ample liquidity, and low leverage. The reality, on closer inspection, looks rather different. While the banks continue to report low levels of non-performing loans, skeptical China-watchers suspect that bad loans are being “evergreened.” Red Capitalism resembles a shell game in which bad debts are shuffled from one entity to another, without any losses observed; this may involve trust companies selling dubious loans to state-run asset management companies or bank loans being turned into corporate bonds and stuffed into wealth management products.32

Low reported loan-to-deposit ratios of the banks also give a misleading impression. Deposits are increasingly unstable

- the banks look to attract deposits from maturing WMPs as the quarter ends but the money flies out the door shortly after. If the banks have no liquidity problems, asks the frustrated China-watcher, why over the course of the last year has the People’s Bank of China been injecting ever larger sums into the banking system?33

As we have seen, loans are being taken off the banks’ balance sheets and placed in shadow banking products. By law, these credit instruments are non-recourse. But skeptics suspect that the banks will be forced to compensate customers for any future losses. Bank loans are officially around 130% of GDP; add on interbank assets, other assets held on balance sheet, and various off-balance-sheet exposures, and the banks’ total credit exposure is close to 300% of GDP.

Perhaps the most profound gap between appearance and reality exists in the contrast between the booming credit markets and the lackluster demand for credit from the private sector. Despite the recent explosion of lending, there are curious signs of distress in the real economy. Chinese companies appear to be squeezed for cash – inventories and accounts receivable have been rising. A recent poll by China Reality Research found the appetite for borrowing among private manufacturers across 50 cities had fallen to an all-time low. Despite near-record credit growth this last year, economic growth continued to weaken.

Local governments, on the other hand, have an insatiable demand for credit. They have needed money to offset the fall in land sales revenue, finance ongoing infrastructure projects, and, on occasion, to bail out large employers in their districts (in July the city of Xinyu in Jiangxi province agreed to spend RMB 500 million paying off the debts of LDK Solar).

Local government demand for credit may even be crowding out other borrowers. A recent trip to China revealed that virtually every credit provider we came across – including banks, trust companies, and asset management companies

- were actively engaged in lending, sometimes at double-digit rates, to local governments. They professed little interest in providing loans to private enterprise whose credit was not back-stopped by the state. “Moral hazard in China is state policy,” one analyst told us.

A considerable amount of recent lending has gone to roll over existing local government debt with interest. It is noticeable that city and rural banks that have lent profusely to local governments have been particularly heavy issuers of wealth management products. Rolling over bad loans doesn’t generate much in the way of economic growth.

Of course, every credit bubble involves a widening divergence between perception and reality. China’s case is not fundamentally different. In this paper, we have documented rapid credit growth against the background of a nationwide property bubble, the worst of Asian crony lending practices, and the appearance of a voracious and unstable shadow banking system. “Bad” credit booms generally end in banking crises and are followed by periods of lackluster economic growth. China appears to be heading in this direction.

- www.pbc.gov.cn/publish/html/2012s04.htm

- See Alan M. Taylor, The Great Leveraging, NBER, 2012.

- Total social financing (TSF) is the PBOC’s measure of overall financing flows extended to the non-financial sector. It was designed to capture credit extended by the shadow banks, and the banks’ off-balance-sheet lending activities, as well as regular bank loans, although it does not fully capture the first of these. TSF includes a small amount of equity issuance by non-financial corporates, which we excluded from this calculation of credit issuance.

- Fitch Ratings compiles an adjusted measure of TSF, adding in certain items not captured in the official data, including loans issued by Hong Kong banks to the mainland and certain forms of trust lending. For the most recent update see: “Chinese Banks – Issuance of Wealth Management Products Heats up as Year-End Approaches”, December 5, 2012.

- Alan M. Taylor, The Great Leveraging, NBER, 2012: “Credit booms and busts can be driven just as easily by domestic savings as foreign saving.”

- Carmen Reinhart, Vincent Reinhart, and Kenneth Rogoff, “Debt Overhangs: Past and Present,” NBER, April 2012

- Borio, C and P Lowe: “Assessing the risk of banking crises,” BIS Quarterly Review, December 2002.

- Caixin: Tall order in Ordos: Giving a Ghost City Life, August 31, 2012.

- China Anatomy Special Report: Changsha Property Bust, Guosen Securities, Andy Collier, October 3, 2012.

- Bloomberg News: China Cities Value Land at Winnetka Prices with Bonds Seen Toxic, July 13, 2011.

- Caixin: Trouble on the Highway, June 29, 2011.

- Caixin: Trusts, Bonds Lead Surge in Credit “Gambling,” October 26, 2012.

- The China Trust Industry Association breaks out trust products issued by “categories of target market.” In recent quarters, the “basic industries” category has witnessed rapid growth and now represents 23% of trust products outstanding, around twice the amount of real estate trusts. A recent study found that of the top 20 “basic industry” trust products issued by size over the past 12 months, 17 were issued by LGFVs. See Bank of America/Merrill Lynch: China: Focusing on the trusts, January 17, 2013.

- http://www.xtxh.net/Trust_Statistics/13130.html

- Bloomberg News: Purple Palace Abandoned Shows China Shadow-Banking Risk, November 19, 2012.

- Data from slide deck accompanying conference call with Yongyi Trust Research Institute, hosted by Credit Suisse, August 11, 2011.

- Fitch Ratings: Chinese Banks – Issuance of Wealth Management Products Heats up as Year-End Approaches, December 5, 2012.

- China Daily: Regulating Shadow Banking, October 12, 2012.

- Bank of America/Merrill Lynch: Shanghai noon, December 11, 2012.

- Reuters: Huaxia Bank blames investors’ panic on sales by rogue worker, December 4, 2012. This credit instrument, which reportedly promised annualized returns of up to 13%, had provided loans to a pawnshop in Henan province. The bank claims that an employee sold the product without its knowledge, but soon came under pressure from the local authorities to make its customers whole.

- FT: China investment products draw complaints, December 27, 2012.

- Bloomberg News: Citic Trust Misses Payment for Product Based on Steelmaker Loan, December 24, 2012.

- UBS: Assessing hidden risks in wealth management products, January 8, 2013.

- Bank of America/Merrill Lynch: Financing Guarantee, struggling for profitable growth, July 16, 2012.

- Caixin: Domino Risk Grips Zhejiang Borrowers, June 26, 2012.

- Caixin: Beijing Loan Firm Teeters On The Edge, August 14, 2012.

- Jefferies: How real is concrete machine demand; the ingenious China machinery financing, May 2, 2012.

- Reuters: Ghost warehouse stocks haunt China’s steel sector, September 17, 2012.

- Morgan Stanley: China Banks – Tougher balance between liquidity & bank risks in 2012, December 10, 2012.

- See “The Central Role of Credit Crunches in Recent History,” Albert Wojnilower, Brookings Institute, 1980. Wojnilower argues that credit booms only end with an interruption in the supply of credit, “such interruptions may be prompted, intentionally or accidentally, by the destruction of lenders’ incentives through regulatory rigidities, such as ceilings on interest rate, or the emergence of serious default problems in major institutions or markets.”

- Yunnan Highway, the only large LGFV borrower to have publicly defaulted, has recently issued corporate bonds with a credit rating provided by a local agency only a couple of notches below the U.S. government’s.

- China’s banks generate a seemingly endless flow of fresh scandal. The latest to appear in the press involves a former employee of the Shanghai Pudong Development Bank who was allegedly moonlighting as a loan shark, funding his activities by borrowing RMB 6.4 billion from the bank’s customers (South China Morning Post, January 12, 2013).

- In 2012, the PBOC provided a net RMB 1.4 trillion of liquidity to the banks.

Mr. Chancellor is a member of GMO’s Asset Allocation team focusing on capital market research. He has worked as a financial commentator and consultant and has written for the Wall Street Journal, New York Times, Financial Times, and Institutional Investor, among others. He is the recipient of the 2007 George Polk Award for financial journalism. Mr. Chancellor is the author of several books including “Crunch Time for Credit” (2005) and “Devil Take the Hindmost:

A History of Financial Speculation” (1999), a New York Times Notable Book of the Year. Prior to joining GMO in 2008, he worked as deputy U.S. editor for Breakingviews.com in New York and for Lazard Brothers. Mr. Chancellor earned his B.A. in History from Cambridge University, and his Master of Philosophy in Modern History from Oxford University.

Mr. Monnelly is a member of GMO’s Asset Allocation team focusing on research and portfolio management. Prior to joining GMO in 2009, he was a research analyst for Kynikos Associates. Previously, he was a financial journalist for Breakingviews.com. Mr. Monnelly earned his B.A. in Classics and Modern Languages from The University of Oxford.

Disclaimer: The views expressed are the views of Mr. Chancellor, Mr. Monnelly, and Mr. Inker through the period ending January 22, 2013 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security. The article may contain some forward looking statements. There can be no guarantee that any forward looking statement will be realized. GMO undertakes no obligation to publicly update forward looking tatements, whether as a result of new information, future events or otherwise. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to securities and/or issuers are for illustrative purposes only. References made to securities or issuers are not representative of all of the securities purchased, sold or recommended for advisory clients, and it should not be assumed that the investment in the securities was or will be profitable. There is no guarantee that these investment strategies will work under all market conditions, and each investor should evaluate the suitability of their investments for the long term, especially during periods of downturns in the markets.

Copyright © 2013 by GMO LLC. All rights reserved.

© GMO