With the end of a historically challenging year for alternative investment strategies, signs emerge of a potentially more favorable environment.

OVERVIEW

One by one, the uncertainties that hampered economies and roiled markets in 2012 seemed to recede a bit in the fourth quarter. It started with the central bankers: Chairman Mario Draghi's 03 announcement of unlimited sovereign debt purchases by the European Central Bank (ECB) dramatically reduced the short-term tail risk of a Eurozone break-up. The result: A quarter that, unlike the previous three, was not driven by a steady stream of market-moving, crisis-related news from the European Union.

Across the Atlantic, US stocks spent the early weeks of 04 on a stimulus high, fueled by the Federal Reserve Bank's announcement of open-ended quantitative easing under OE3 in September. The event that disrupted that rally in the short-term-the US presidential election actually helped set the market on more solid long-term footing, as investors found some measure of certainty in the reelection of Barack Obama. Renewed fears that US politicians would fail to reach a compromise to avoid a plunge over the so-called "fiscal cliff" pushed equities lower in the last week of 2012, but stocks rallied on the final trading day on word that a deal was at hand.

In spite of these developments, sentiment at year-end had not yet turned entirely positive. Investors are keeping a wary eye on some contrary indicators, including a 04 downturn in commodities markets that seems out of place if the global economy is truly in recovery mode. Additional fiscal battles loom in Washington as well.

More broadly, the market has yet to receive convincing data indicating that the good news in 04 has enticed companies to resume capital expenditures. Investors are therefore left to wonder if the improving picture reflects real fundamental strength, or merely a market riding an unsustainable tide of stimulus.

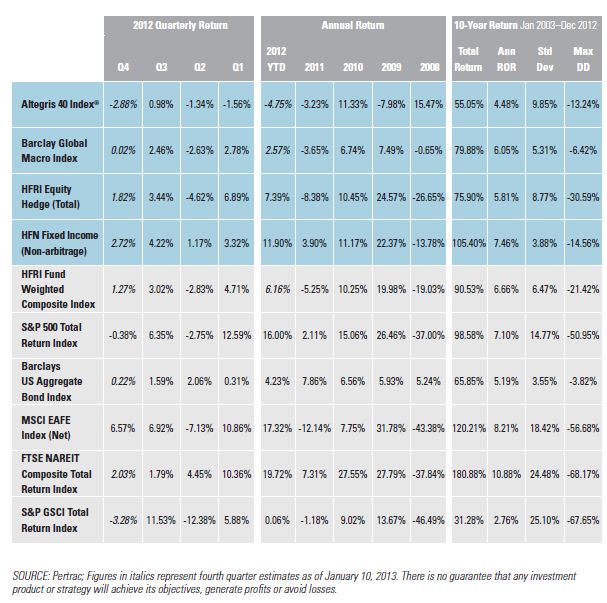

As shown in Figure 1, equities (S&P 500Total Return Index) were down -0.38% in 04, and bonds (Barclays US Aggregate Bond Index) were up a modest 0.22%. Among alternative investment strategies, managed futures (Aitegris 40 Index®) were down -2.88% during the quarter, while global macro (Barclay Global Macro Index) was up 0.02%. Long/short equity (HFRI Equity Hedge [Total] Index) was up 1.82% and long/short fixed income (HFN Fixed Income [Non-Arbitrage] Index)

was up 2.72%.

FIGURE 1.

ALTERNATIVE INVESTMENT INDEX PERFORMANCE VERSUS TRADITIONAL INDICES I (G42012)

Mixed performance by alternatives and major indices during the fourth quarter.

WITH EUROPE QUIET, THE US AND JAPAN TAKE CENTER STAGE

The fourth quarter of 2012 was particularly notable for a lack of headlines from Europe. The ECB's 03 commitment to unlimited sovereign bond purchases defused the Eurozone crisis at least temporarily by removing the near-term risk of a breakup of the European Union.

With those concerns moved to the side, four other developments drove market direction and sentiment in 04 2012:

1. The victory of President Obama over Mitt Romney in the US presidential election, which triggered a brief but sharp equity market selloff.

2. Continued stimulus from central banks in Europe and the United States, including a December announcement by the US Fed that it would maintain historically low interest rates as long as the US unemployment rate was above 6.5% and inflation below 2.5%.

3. The "fiscal cliff': the looming combination of automatic tax increases and government spending cuts that acted as a drag on economic and investment activity in the US throughout the quarter.

4. The return of the Liberal Democratic Party (LDP) to power in Japan and the subsequent assumption that the Bank of Japan (BoJ), one of the last holdouts for tight monetary policy, would join the major Western powers in their historic stimulus binge.

CENTRAL BANKS AND POLICY EXPECTATIONS SET THE TONE

Freed from the Eurozone-related volatility that had whipsawed markets for the prior year, activity in 04 was largely driven by stimulative policies put in place by central banks the previous quarter. After a difficult October in the equities market, stocks continued to sell off in November in the wake of Obama's victory over Romney and the assumption that tax increases were inevitable. Hit hardest were the stocks that had performed especially well in 2012, including many blue-chips, as investors took profits ahead of the expected expiration of Bush-era tax cuts. As expected, US interest rate futures rallied as the stock indices faltered. That selloff proved transitory, however, and the traditional late-year "Santa Rally" took hold before the Thanksgiving holiday. In December, the Fed provided the market with even more fuel by announcing that, for the first time in its history, it was explicitly linking its interest-rate policy to specific quantitative metrics of unemployment and inflation-feeding into a late-quarter equity market recovery. Accordingly, interest rate futures reversed course and yields rose from mid-November through mid-December.

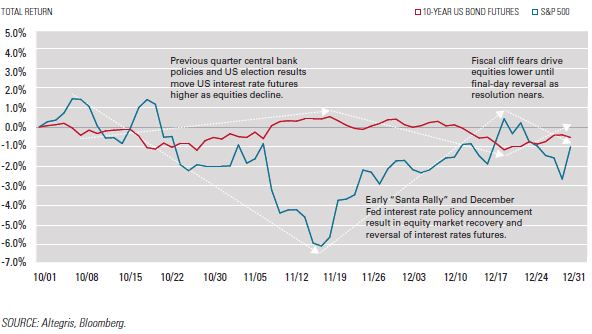

Hanging over all this was the fiscal cliff-which the US Congressional Budget Office estimated could knock half a percentage point off US GDP in 2013 if allowed to take effect. There is no doubt that concerns about the fiscal cliff acted as a drag on economic and investment activity during the quarter. The approaching end-of-year deadline for congressional action actually stopped the equity rally in its tracks and the S&P 500 TR notched five consecutive losing days, culminating with a -1.1% drop on Friday, December 28. Interest rate futures rose as equity markets fell, but the movement in rates was relatively modest in comparison. By the time domestic equity markets opened the following week, word had begun to spread that a deficit deal was imminent and the S&P 500 TR rose 1.7% on the final day of trading for 2012, while interest rates fell in nearly the same proportion. Interestingly, as represented in Figure 2, it appears as if equity and interest rate markets were nearly negatively correlated, moving in almost exactly the opposite direction as macro sentiment ebbed back and forth.

The final major market driver in 04 was Japan, where the ascendency of the LDP and presidential candidate Shinzo Abe convinced investors that the Bank of Japan's foray into monetary stimulus would not only continue, but accelerate in 2014. Throughout the presidential campaign, Abe called on the BoJ to double its inflation target from 1% to 2%. When the central bank announced its third round of stimulus in the past four months in the wake of Abe's landslide election victory as Prime Minister in

December, it also signaled that it would indeed set a higher target at its January meeting. While the BoJ's actions were certainly a direct response to signs that a fledgling economic recovery might be flagging, Abe's role in pushing the bank to move has called into question the bank's historic independence. These developments-and Abe's promise to deliver a big fiscal stimulus package to jump-start the economy-threatened and ultimately did send the yen into a tailspin.

FIGURE 2.

CORRELATION OF EQUITY MARKETS AND INTEREST RATE MARKETS I Total Returns (042012)

Equities and interest rate futures moved in opposite direction on central bank policies, US election results and the fiscal cliff.

PRIMARY MARKET EFFECTS

The impact of the events described above was most obvious in currency markets. The achievement of at least temporary stability in Europe opened the door to a strong November recovery in the euro that caught many managed futures managers off guard. An early November decline in the euro seemed to indicate that the short euro trade was still solid. But as Europe found its political footing and markets shifted to more of a risk-on environment, the euro rallied hard in late November and into December. The rapid appreciation of the euro against nearly every other currency in the world erased prior gains from short positions and made the euro a negative attributor for a number of managed futures managers.

Many macro managers were long the yen moving into 04. But troublingly weak data releases and the increased certainty that Abe would be swept into office with a mandate for both monetary and fiscal stimulus sparked a selloff, with the currency falling 10% against the dollar and 12% against a recovering euro over the three months. Among managed futures managers nimble enough to put on short positions ahead of the dramatic move, the short yen trade proved to be one of the quarter's biggest winners.

Long/short equity managers faced a challenge in the form of the post-election downturn in US stocks, in which names that had traded up strongly in the first three quarters of the year sold off disproportionately as investors took profits ahead of seemingly unavoidable tax increases. Included in that list of losers were many companies classified by managers as long-term holds. A rebound in US stock indices later in the quarter made up some of the lost ground.

If there was one asset class that stood out in 04 as a potential cause for concern about future market direction, it was commodities. Commodity futures essentially traded sideways through the first three quarters of 2012, with a few notable exceptions, such as the drought- driven rally in grains in 03. In 04, however, that rally reversed course and grains joined other commodities in a downturn. This reversal represented a pain point for macro and managed futures managers, and, perhaps more importantly, raised an interesting yet possibly troubling question: If the global economy is gaining strength, why are commodities selling off?

Against this backdrop, following is a detailed assessment of the managed futures, global macro, equity and fixed income markets.

© Altegris Advisors