Look at the Bears! Look at the Bears!

ING Investment Management

F.I.R.S.T.

Fixed Income Research and Strategy Trends

February 1, 2013

Christine Hurtsellers, CFA

Chief Investment Officer, Fixed Income and Proprietary Investments

Matt Toms, CFA

Head of U.S. Public Fixed Income

Mike Mata

Head of Multi-Sector Fixed Income

Look at the Bears! Look at the Bears!

Those who were not completely blinded by Brad Pitt’s lustrous locks likely remember the 1994 exercise in miserabilia Legends of the Fall as a dark comedy rather than the epic drama that Netflix claims. After 133 minutes of depicting what World War I, Prohibition and other forms of devastation can and will do to people, the film ends with Brad’s now-aged frontier heartthrob getting the short end of hand-to-hand combat with a grizzly bear. To which the narrator concludes, in perfect deadpan, “It was a good death.” Roll credits — and die laughing!

Maybe we are short-changing the power of symbolism here. There was probably something really deep about how beautifully full-circle it was to have the bear-like nonconformist spirit embodied by the protagonist get — honorably — clubbed to death by a bear the size of a Buick. But a good death? Thanks, Hollywood, but a bear attack — artistic countenance or otherwise — is never a “good” way to go. Just ask anyone who owned fixed income back in 1994, a bear of a year for bonds. In fact, that year saw the most horrific onslaught on bond values in history.

Flashback to January 1994. After almost three years of economic expansion, bond yields were historically low and — with wage growth non-existent at the time — inflation was a distant threat. In February, however, Alan Greenspan and the Federal Reserve began nudging short-term interest rates higher in response to the strengthening economy. More than $600 billion was lopped off U.S. bond values in the seven months that followed. Once the impact of bearish interest rate sentiment and rising long-term interest rates swept across the globe, the worldwide hit to bond values was somewhere in the ballpark of $1.5 trillion. In short, bear attacks, Brad, are in fact not “good”.

Fast-forward to January 2013. As the tide of uncertainty surrounding Europe, China and the U.S. has receded in recent months, it appears that the lows on developed market sovereign rates are in the books; the ten-year U.S. Treasury yield, for instance, likely hit its rock bottom near 1.4% back in July. As market sentiment re-prices and re-characterizes the world as a safer place, the value of safe-haven assets has begun to diminish, and yields, in turn, have started to creep higher. This is a natural and, frankly, warranted occurrence: investors are selling low-risk, overvalued assets like Treasuries and buying riskier assets that appear less fully valued, like stocks. But given the fantastic bull run bonds have had in recent years amid the ubiquitous monetary stimulus that has kept interest rates artificially low, is a 1994-esque bear attack lurking on the horizon?

The short answer is no; this is not 1994 all over again. Yes, the grumbling of bond bears is reverberating in Treasury yields, but that sound isn’t the death knell of a grizzly; at this point, the closest ursine analogue is Boo-Boo Bear. You remember Boo-Boo, right? He was the titular character’s companion on The Yogi Bear Show. Sporting his little bow tie, Boo-Boo served as the voice of reason for the impulsive Yogi and tried to steer him clear of trouble, typically in the form of Ranger Rick. A modest upward correction in interest rates at this point is like little Boo-Boo tugging at your side: a gentle warning — not a cause célèbre — that normalization, as opposed to another legendary 1994-style melee, is underway.

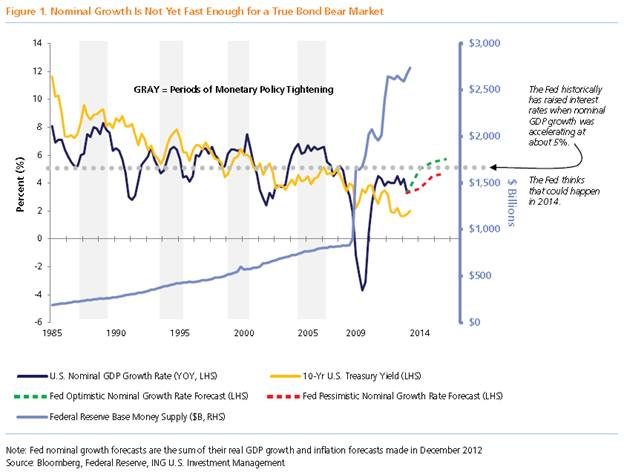

But what will normal look like and is the path there free from danger? Unless the U.S. economy starts to grow at a much faster pace than we’ve seen in the past few years, the path to higher interest rates is unlikely to be fraught with grave dangers of the principle-eroding kind. Figure 1 depicts the pace of nominalU.S. economic growth (that’s real GDP growth plus inflation) and the level of U.S. Treasury bond yields since 1985. The shaded boxes reflect periods during which the Fed was raising the fed funds rate in an effort to slow the U.S. economy via tighter monetary policy. The Fed historically has tended to start raising interest rates when nominal spending was growing at a pace of 5% or better, happy to bide its time coming out of recessions before tightening monetary policy when both real growth and inflation were low. In all four of the tightening periods shown, U.S. bond yields rose in response to higher short-term rates.

These may sound like the normal rules of engagement to anyone who invested in fixed income before 2008 (and who therefore likely remembers both the young Brad Pitt and Boo-Boo). But what is normal now? Strange times called for unorthodox measures post-2008: Traditional rules were thrown out the window during the 2009 recession when nominal spending fell by 4% after the housing bubble burst and the banks almost went broke. The Fed had to write a new set of rules for interest rates, starting with a 0% fed funds rate and rolling right into multiple rounds of quantitative easing and Treasury market interventions.

With nominal GDP growth in the U.S. struggling to stay above 4% — pulled by the opposing forces of a blossoming housing-led recovery and robust private sector demand on one side and ongoing, long-term fiscal retrenchment on the other — those unconventional rules are likely to be in place throughout 2013 and beyond. Of course, there is a possibility that the normalization of interest rates could begin sooner; the Fed’s own forecasts for real GDP growth and inflation suggest a potential 2013 return to the 5% rate of nominal growth should things break right for the U.S. economy (see Figure 1). Such a move would be enough to send the unemployment rate back down toward 7% and would be like a round of Winstrol shots and bear growth hormone for Boo-Boo as the market begins to question the need for the Fed to continue its aggressive pace of bond purchases that are keeping yields artificially low.

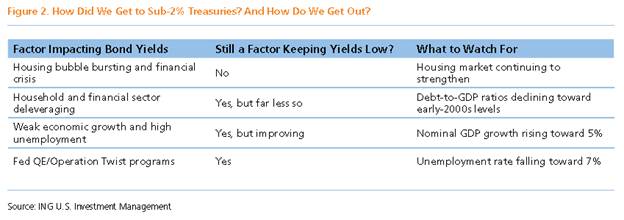

But this is not 1994 all over again — or any other period like it, for that matter. The Fed of modern day has all its chips in the center of the table in an attempt to spur growth and to fight deflationary pressures by managing both the short and long ends of the yield curve through unprecedented open-market operations. Figure 2 summarizes the myriad factors that have driven the Fed to engage in these measures and for bond yields to fall to current levels. It also lists the metrics that could forewarn of a more meaningful rise in rates.

If you read the fine print of the Fed’s exit strategy, though, the central bank has been explicit about what needs to occur before a tightening cycle will begin (6.5% unemployment, for one). And unless you’ve been living in Jellystone Park for the last few years, the mantra for fixed income investors has been and continues to be don’t fight the Fed. The ominous growth-inhibiting effects of debt and deleveraging cycles that are keeping interest rates low take time — years, in fact — and fiscal deleveraging has only just begun in the U.S. Business spending is weak, as is wage growth, and unemployment levels are still stubbornly high.

Yogi Bear reportedly got his name from longtime Yankee Yogi Berra, who despite his Hall of Fame credentials is perhaps better known for his often perplexing quotations; among his more profound offerings is “When you get to a fork in the road, take it.” Applied to your bond portfolio, the fixed income market is at an inflection point. Though the bull run in bonds is over, the bond bear is only sidekick-sized right now; while rates can start to move higher, the blunt-force trauma of a rapid, Fed-induced spike in interest rates — à la previous tightening cycles — is off the table for the foreseeable future given the multitude of factors keeping bond yields low across the curve and expectations of moderate economic growth. Aging demographics and fiscal spending cuts await the developed world once bonds yields find their way out of the cellar and establish a new baseline.

Interest rates will gradually and naturally rise in this environment. At some point, however, central banks will begin to reverse course and present a real threat to bond portfolios; the best way to avoid a mauling down the road is to resist passivity in your fixed income asset allocation now. As we described in last month’s F.I.R.S.T., this means that active sector rotation and prudent, bottom-up security selection will be the necessary tools if you want to leave the “good deaths” to Hollywood.

This commentary has been prepared by ING Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors. Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

© ING Investment Management