Markets Near All-Time Highs

A strong Friday finish propelled equity markets into positive territory for the week. The S&P 500 rose 0.7% while the Dow Jones Industrial Average gained 0.8%. Both indices experienced their best January return in years, posting gains of 5.2% and 5.9%, respectively. Stock markets are closing in on all time highs, reaching their highest levels in five years.

A series of positive economic reports and corporate earnings results have led to a robust start to 2013. Investors continue to pile into equities, with the biggest four-week inflow since 1996 occurring in January, according to Lipper data. According to the Wall Street Journal, January’s net flow of $34.2 billion was more than the flows for all of 2012.

Earnings continue to roll in at a positive clip. Through last Friday, 234 companies in the S&P 500 reported and 70% have beaten consensus estimates, according to data from FactSet. This is slightly above levels seen in prior quarters. On the revenue front, companies have bounced back from a weak third quarter with roughly two-thirds topping expectations.

Earnings growth picked up considerably last week as 100 more companies reported. The S&P 500’s blended growth rate advanced from 2.6% to 4.0%, with the increase primarily driven by energy sector results. Major energy companies including Chevron, Valero, and Exxon Mobil reported significant upside earnings surprises last week, boosting the headline index.

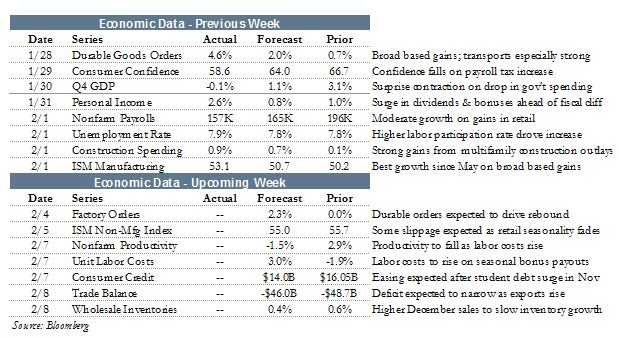

Several important economic indicators were released last week, covering a broad swathe of the economy.

On Wednesday, the Bureau of Economic Analysis (BEA) released the first estimate of fourth quarter GDP. The quarter’s 0.1% decline was the first contraction in more than three years, and was well below even the most pessimistic estimate.

Below the surface, however, the report was actually quite encouraging. Consumption – which makes up some 70% of domestic output – increased 2.2% in the quarter. Other important sources of growth included nonresidential and residential investment. These are all pillars of sustainable growth in the US economy, and suggest the country is on stable footing.

Declines were concentrated in inventory investment and government spending, specifically defense spending. In fact, the 22% drop in defense spending was the biggest decline since 1972, and illustrative of the belt tightening that has occurred in the public sector in anticipation of Congress’ looming sequestration. Overall, however, investors can view the initial Q4 GDP report in a favorable light, despite weakness at the headline level.

Personal incomes jumped considerably in December, rising 2.6%. This was the biggest gain in eight years. The increase was attributable to accelerated bonuses and special dividends, as companies sought to distribute capital ahead of potential tax hikes in 2013.

Spending was also positive, although slightly below expectations with a 0.2% increase. Negative spending growth for nondurables, specifically gasoline, weighed down the headline level. Consumers’ saving rate did spike higher in the month, suggesting most of the surge in incomes did not immediately pass through.

The Institute of Supply Management (ISM) reported on Friday that its manufacturing index accelerated to 53.1 in January. This was a jump of nearly three points, and ends a string of reports that hovered around the 50-line (which demarcates expansion/contraction in the sector). New orders improved by 3.6 points, returning to expansionary territory and boosting the headline index. At 53.3, new orders are solidly in positive territory and foreshadow sustained growth moving forward.

In Uncertain Environment, Jobs Grow Tepidly

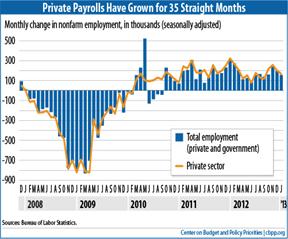

For the 35th consecutive month, private payrolls registered positive growth. It was hardly the robust report economists would prefer, but the labor market continues to mend. However, there are still plenty of reasons to be concerned, especially with sequestration on the horizon.

In January, nonfarm payrolls expanded by 157k and private payrolls grew 166k. Consistent with the post-recession environment, the strongest growth occurred in the retail, business services, education & health, and leisure sectors.

Source: Center on Budget and Policy Priorities

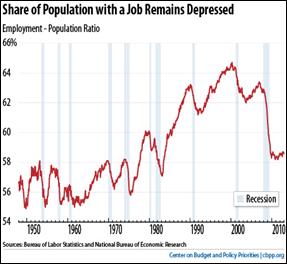

Less encouraging was the unemployment rate, which ticked higher by 0.1% to 7.9%. The household survey showed a modest rise in labor force participation. At the same time, the share of the population currently employed remains historically low at 58.6%.

Source: Center on Budget and Policy Priorities

There was a relatively dramatic shift in the length of unemployment for many individuals in the latest report. In some cases, the duration of unemployment fell by more than 2 weeks, according to the Center for Economic and Policy Research (CEPR). CEPR believes that many of those workers simply saw their benefits expire and chose to stop looking for employment.

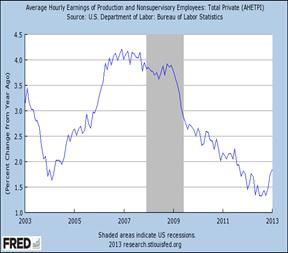

Wages continue to remain muted for workers. Private sector wages rose 0.3% in January and are up 1.8% in the past year. That is faster than the 1.5% rate for all of 2012, but still below pre-crisis levels.

Source: Federal Reserve Bank of St. Louis

The January jobs report was in line with the post-recession trend, but suggests an economy unable to break free from stall speed and onto more sustainable ground. The upcoming sequestration talks have the potential to derail job growth and bears close watching by investors.

the week ahead

After a busy week, there are few economic data reports to digest this week. On Tuesday, ISM releases its non-manufacturing index, which measures productivity and expansion in the US service sector. On Friday, international trade data is scheduled for release.

On the central bank front, the Bank of England and the European Central Bank meet this week. No major change in policy is expected. Other rate announcements include Serbia, Romania, Australia, Poland, and Czech Republic.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

For more information, please visit our website at http://www.Fortigent.com.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent