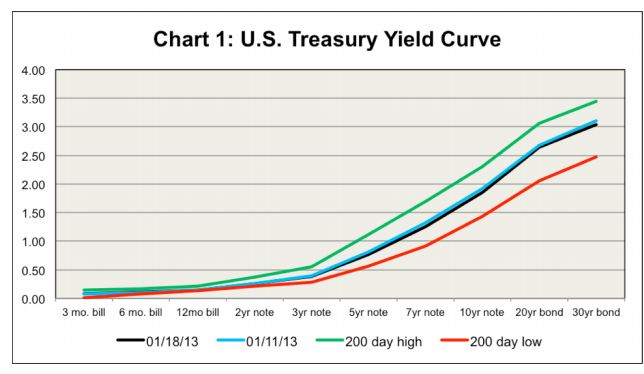

Last week Treasury yields were nearly unchanged out to three years and down 4-7basis points further out the yield curve (Chart 1).

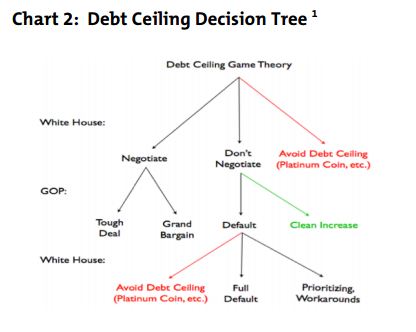

Games People Play. Last week Administration officials, including the President, clearly ruled out using extraordinary legal measures to avoid defaulting on Treasury’s financial obligations in the absence of a debt ceiling hike by Congress. The two legal measures most discussed, going back to the summer 2011, were invoking the 14th Amendment and minting a trillion dollar platinum coin. The coin idea was dismissed as Fed officials commented that the central bank would not honor the coin as a deposit, and the amendment idea has been shelved a number of times. Ruling out these methods has lopped off two branches (shown in red) of the debt ceiling decision tree shown in Chart 2. The President’s demanded outcome, a debt ceiling raised independently of spending cuts legislation, is shown in green – the “clean increase.”

Following the two paths left to the White House (i.e., negotiate or don’t negotiate), we see the GOP has three options: Negotiate a 1) tough deal, 2) a grand bargain or 3) allow default to occur. If the GOP allows default, the White House now has two options remaining: 1) allow a full default or 2) prioritize payments and discover last second workarounds to avoid full default.

We all know the problem with a full default, so we will let that outcome go uncommented. In the absence of a debt ceiling raise, GOP lawmakers have said (as in 2011) that Treasury could prioritize and make timely payments on about 60% of the money due.2 The GOP position is to obtain heavy spending cuts (but not for GOP-favored programs) and, if that was to fail, then place the political blame on the White House by making Treasury pick the winners and losers of whom will get paid once the cash shortfall hits.

A partial default via payment prioritization, however, has significant technical and legal issues that Treasury pointed out during the 2011 debacle. Operationally, Treasury estimated it makes over 80 million payments a day. As Treasury never expected partial defaults as a part of operations, no one programmed the payment systems to do it. There is no evidence Treasury has made any such programming changes since the near default of 2011. Over and above technical issues, Treasury legal counsel warned that there is no legal precedent to pick winners and losers in a partial default scenario.

At this point, the White House and the GOP House have been engaged in a stare-off and are very far apart on negotiating anything substantive. If recent history holds, nothing may be accomplished for a few more weeks, at least until Treasury warns sometime in February of the imminent cash crunch. And remember, with bond bears de-clawed by the Fed, and Treasuries offering liquidity in a storm (even if the storm is much about paying on Treasury debt), it may be up to the stock market to signal the financial markets’ displeasure and fear to politicians.

Late last week, though, the GOP added a new wrinkle as it signaled interest in passing a temporary debt ceiling limit in order to tie it to the sequester and government budget authority expiration that will occur in March. This tying of the debt ceiling to these issues is exactly what the White House does not want. If this House action occurred, and passed the Senate, the President would get a “clean increase” in the debt ceiling to sign into law. But the catch would be that it would last for under three months. If so, how would White House then respond? If the temporary debt ceiling increase was not signed by the President, the GOP might have successfully shifted the blame for a default onto the White House.This all reminds us of The Spinners soul classic “Games People Play.”3 The chorus of the song summarizes things pretty nicely:

Games people play Night or day they're just not matchin' What they should do Keeps me feelin' blue Been down too long Right, wrong they just can't stop it Spendin' all day Thinking just of you

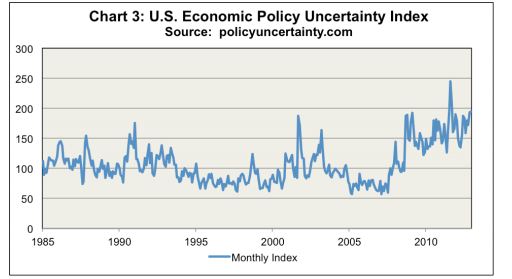

This is all unfortunate because it not only dampens domestic economic growth, which is primed to increase if lawmakers make the right choices, but influences the global economic outlook and weakens US political power abroad. Chart 3 shows the policyuncertainty.com economic policy uncertainty index through December: The December reading was the second-highest on record, and eclipsed readings around the Lehman collapse (2008), the two Gulf wars, 9/11, the 1998 global financial crisis and the debt defaults of major US corporations (2002). The December reading trailed only the reading from August 2011 when Treasury nearly defaulted.

We could be surprised. GOP leadership and the rank and file may conclude that Mr. Obama is serious and better positioned politically. They might bear major responsibility for seniors not receiving their pension checks on time. The debt ceiling increase could be passed independently of spending cuts legislation as the President has demanded. Or perhaps the President will blink (again). But, the whole purpose of the White House lopping some branches off the decision tree is to in essence paint the White House and the GOP into a tighter corner.

While we hope for a peaceful solution for the good of the economy and financial markets, we expect a window of market volatility to open sometime in February (or in March if a short-term increase in the debt ceiling is passed into law). This timeframe may offer a window of buying opportunity during a selloff in risk assets. In preparation for this expected window opening, although we retain our core bias to be short benchmark pure interest rate duration, we are relatively less short than usual. And, while we also retain our core bias to be long to benchmark corporate credit spread duration, we are relatively less long than usual.

I’m the One. The Fed is not the only central bank buying increased amounts of US Treasuries. From the Swiss central bank (the SNB) to the Bank of Japan (BOJ) to China (PBOC), a number of major central banks have increased US Treasury purchases as a result of economic policy.

In the case of the SNB, Treasury purchases come from dollars swapped for euros. Switzerland since September 2011 has engaged in a policy of pegging the Swiss franc (SF) at a minimum floor of 1.2 SF/EUR. Swiss leaders believed the SF too strong, a result of flight from the euro crisis, and that this hurt the Swiss economy, for example export competitiveness. Despite the strength of the SF and zero-to-negative interest rates, inflation is barely measurable.

One result of this policy has been a massive expansion of the SNB balance sheet, one that dwarfed the balance sheet growth (as a percent of GDP) by the ECB, the BOJ, the Bank of England and the Fed. At the end of the third quarter of 2012, the SNB balance sheet was SF 503 billion and GDP was SF 551 billion. The balance sheet equated to 91% of GDP4 compared to about 33-35% for the BOJ and ECB. If the Fed buys $1 trillion in government bonds this year, the balance sheet would equal about 24% of US GDP at year’s end. We can see, the SNB action made the other major central banks look like pikers. The SNB has conducted in many ways the most radical monetary policy of the major central banks.

As this balance sheet growth was accomplished mainly through creation of SF to sell against euros, the SNB ended up holding a massive amount of euros. Selling some of these for other currencies was prudent and US dollars were purchased as part of this strategy. For example, in the third quarter of 2012, the SNB increased its holdings of US dollars in its SF430 billion foreign exchange (FX) reserves account by 6 percentage points to 27.6% of total FX reserves. That equals approximately $27 billion reallocated to US dollars. When a central bank buys US dollars, it most often parks them in treasuries. At the end of November, Swiss holding of US Treasuries was $187 billion, up a net $61 billion y/y. Switzerland is the 7th largest holder of treasuries, up from 9th a year ago.

This Q3 reallocation came after SNB officials caught their collective breath. The upward pressure on the SF relaxed as risk appetite returned after ECB chief Draghi’s pledge to defend the euro monetary union in July. So for now we expect the SNB to stay in watch and wait mode unless the euro crisis re-ignites.

Across the globe, Japan’s new Prime Minister (Shinzo Abe) recently pledged to consider a $550 billion US dollar equivalent (¥50 trillion) fund to buy foreign securities. A lot of that presumably would find its way into Treasuries. Japan already has steadily boosted its holdings of treasuries. Presumably, Japan eventually would unseat China as the top foreign holder of Treasuries if this $550 billion fund were to come into play.

The Fed, China and Japan are the top three holders of marketable Treasury debt, collectively totaling $3.8 trillion, or 35% of the $11 trillion outstanding. Most of the Treasuries held by China are held by official institutions. In Japan, many of the Treasury holdings are with official institutions. Therefore, clearly most of the Treasuries held by the three top holders are used for economic or monetary policy purposes and will not be traded anytime soon. Further, the amount of Treasuries purchased and held for policy purposes is on the increase. This phenomenon remains a bullish influence helping to hold down US long term interest rates.

And that, readers, reminds us of the chorus to the ripping Van Halen tune “I’m the One”, about the joy of being on stage, playing to a wild audience.”5

I'm the one, the one you love Come on baby, show your love

Focus on Fixed Income Will Return on February 11, 2013

1Source: Mike Konczal (a.k.a. Rortybomb) at nextnewdeal.net.

2Treasury finances 40% of its budget through debt issuance and this source would vanish with no debt ceiling hike.

3Games People Play. Jefferson, Hawes and Simmons, Atlantic Records, 1975.

4This extreme is a reason we pay attention to the risk that the small but financially important country like Switzerland could one day run into some trouble.

5I’m the One.E. Van Halen, A. Van Halen, Anthony and Roth, Warner Bros., 1978.

NEWER OR IN-USE FEDERAL RESERVE POLICY FACILITIES

LSAP – Large-Scale Asset Purchases.

TDF – Term Deposit Facility.

SECURITIES ACRONYMS:

ABS – Asset-Backed Securities. Can be a reference to the broad securitized markets but usually refers to non- mortgage assets such as credit cards and auto loans. ARS – Auction Rate Securities.

BAB – Build America Bonds.

CDO – Collateralized Debt Obligation.

CLO – Collateralized Loan Obligation.

CMBS – Commercial Mortgage-Backed Securities. Large commercial property-backed securities.

CREL – Commercial real estate whole loans.

MBS – Old acronym for government-guaranteed RMBS.

REMIC – Real Estate Mortgage Investment Conduit. Re-REMIC – A restructuring of an existing REMIC. Repo – Repurchase agreement - a short term loan collateralized by securities.

Reverse – Reverse repurchase agreement - a short term borrowing using securities as collateral.

RMBS – Residential Mortgage-Backed Securities.

Tri-party Repo or Reverse – A repo or reverse that uses a clearing bank custodian in the middle.

VRDN – Variable Rate Demand Note.

OTHER USEFUL ACRONYMS, WORDS OR PHRASES

CDS – Credit Default Swap.

CPD – Cumulative Probability of Default.

EFSF – European Financial Stability Facility.

EMU – The economic and monetary union of Europe. Also called the euro area or eurozone.

GGYC – Great Global Yield Chase, from 2002 to 2007.

GGYC II – The yield chase since 2009.

IOER – Interest On Excess Reserves. The interest rate the Fed pays on excess (not required) bank reserves at FRB’s. This is as yet a hypothetical rate.

IOR – Interest On Reserves. The interest rate the Fed pays on required and excess bank reserves at FRB’s. This rate was set at 0.25% on December 16, 2008.

LTRO – The ECB’s Long Term Refinancing Operation. OMT – The ECB’s Outright Monetary Transactions program.

OT or Op Twist – The Fed’s Operation Twist program.

PIG – Portugal, Ireland and Greece.

PIIGS – Portugal, Italy, Ireland, Greece and Spain.

QE – Quantitative Easing

SFP – US Treasury’s Supplementary Financing Account Program. T-bills issued on behalf of the Fed to soak up excess bank reserves.

SMP – The ECB’s Securities Market Program.

SOMA – System Open Market Account, i.e. the New York Fed’s government securities portfolio.

SPV – Special Purpose Vehicle.

TBTF – Too Big to Fail.

TITF – Too Interconnected to Fail. The Troika – The EU, ECB and IMF. ZIRP – Zero Interest Rate Policy.

Due to the technical nature of this publication, it is intended for broker/dealers, financial planners, institutional investors and other sophisticated investors. The information herein has been obtained from sources that we believe to be reliable, but we .do not guarantee its accuracy or completeness. All opinions expressed herein are subject to change without notice. Calvert Investment Management, Inc., its affiliated companies or their respective directors, officers and/or employees, may have a position in the securities discussed herein. Calvert may have acted upon this research prior to or immediately following publication. Copyright, 2013. Calvert Investments, Inc. All rights reserved. MC10004