Japan’s new Prime Minster Shinzo Abe made more of an impact on the market than anyone else last month. In what the market has dubbed “Abenomics,” Abe not only launched a new fiscal stimulus, but also pushed the Bank of Japan to raise its inflation target from 1% to 2% AND agree to a new open-ended QE program. The reluctance on the BoJ’s part is clearly visible because the new open-ended QE will not start until 2014 and there is no commitment to asset purchases after 2014. Shortly afterwards, the BoJ governor said he would step down, a clear sign of disagreement. In the last two months, the Yen has weakened over 13% due to “Abenomics.”

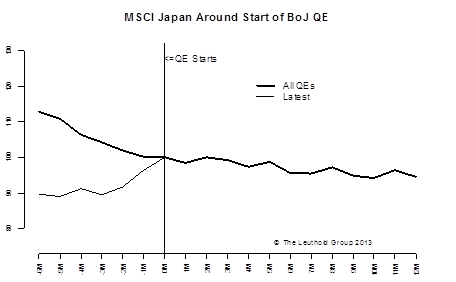

To its credit, “Abenomics” has revived investors’ optimism towards Japan. Japanese stocks have rallied strongly in the last three months, which contrasts sharply with the general downtrend preceding the previous announcements of QE.

Although the decisiveness and the swiftness of Abe’s policy actions feel like a breath of fresh air in a slow-moving, reactionary, consensus-driven government, the policy tools employed so far are nothing more than old medicine in a new bottle. We are highly skeptical that “Abenomics” can produce significantly different results this time.

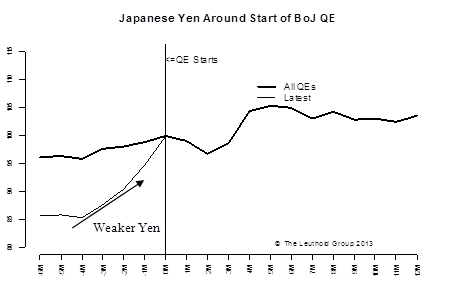

The market’s reaction to Abe’s new policies was most pronounced in the movements of the Yen. The sharp sell-off from around 80 to over 93 was much quicker than the historical norm. Historically, the Yen has tended to weaken only marginally after QE.

The weaker Yen is a key transmission channel for “Abenomics,” as it is believed to make Japanese products more competitive in the global marketplace. We believe this is only a very near-term effect; the longer-term problems with Japanese products are more about the lack of competitiveness in terms of innovation and quality than pricing. After decades of recession, Japanese companies have cut costs to the bone, often at the expense of maintaining their previously high levels of R&D. Due to deflation, the compensation incentives for innovation have suffered greatly in the last decade. In other words, a weaker Yen is unlikely to have material longer term impact on competitiveness.

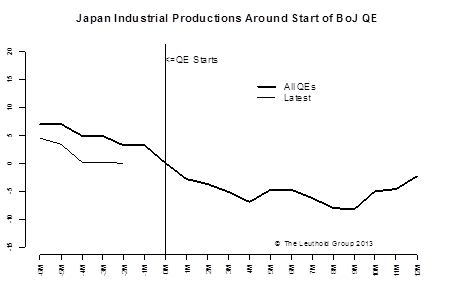

Despite the fancy new name, these policies have been tried and failed in Japan before, and our doubts are justifiable given Japan’s poor record. Historically, Japan’s economy has not gained significant traction after QE. The bottom chart on the previous page shows a very anemic response to QE in terms of industrial production.

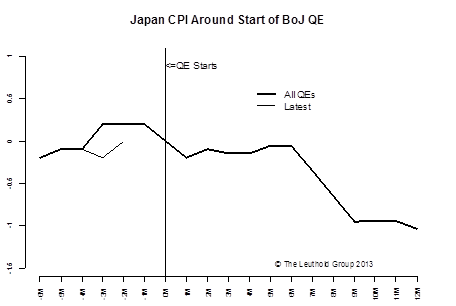

For QE to have a sustainable impact on the currency, it needs to change inflation expectations. Here again, Japan’s historical record doesn’t lend comfort to investors hoping for a dramatic increase in inflation. As the chart above shows, it is very hard to break out of the deflation trap.

Another reason for our skepticism is the political motivation behind “Abenomics.” The goal is to win the Upper House in the upcoming summer parliamentary election. This largely explains the extraordinary swiftness and decisiveness of the policy actions so far. But what happens after the election can be a totally different story. We need to see a lot more evidence before we can say this time really is different. In other words, unless we see a Swiss Franc-style direct FX market intervention, the recent QE-induced slide in the Yen has gone too far too fast. We are not convinced that QE alone can make the Yen much weaker going forward.

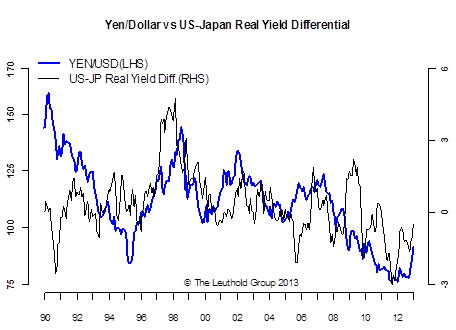

Having said that, we do believe the Yen should and will be weaker in the longer term due to deteriorating interest rate differentials. The chart below shows the 10-year real yield differential between the U.S. and Japan; the Yen/USD rate follows the real interest rate differential closely. As U.S. real yield differentials increase (or get less negative) over Japan, the Dollar typically strengthens against the Yen. This is happening right now, and we believe this trend is likely to continue in the foreseeable future as the U.S. economy is far more competitive than Japan’s.

© Leuthold Weeden Capital Management