In today’s low-yield environment, investors need a fresh approach to managing their portfolios for higher income. Liquidity tiering provides a framework that can help you achieve both principal stability and yields sufficient to meet your goals.

Finding Balance in an Unbalanced Market

These are exceptionally challenging times for income investors. With the Federal Reserve (Fed) holding short-term rates unusually low for the foreseeable future and possible structural changes coming for money market funds, investors are increasingly challenged to balance their income and liquidity goals.

Fearful of continued market volatility, investors still have significant holdings in ultraconservative investments, parking their money in low-yielding U.S. Treasurys, money market funds and bank deposits. But this strategy presents its own risks — namely that the paltry yields these investments offer will make it difficult for investors to meet their financial and personal goals.

Fortunately, the tiering of fixed income investments according to liquidity can provide a flexible solution, helping to satisfy the short- and intermediate-term needs of investors while putting their assets to work in more effective ways.

How Safe is Safe?

In 2008, the Federal Reserve cut the target federal funds rate, a key benchmark for short-term interest rates, to a record low range between 0.00% and 0.25%. The Fed’s goal was to help pull the U.S. economy out of its financial crisis and deep recession, with the expectation that once the economy stabilized rates would return to more normal levels.

The reality is that while U.S. Treasurys represent the so-called “risk-free” rate, given their low yields, these investments are all but certain to result in negative returns on an inflation-adjusted basis.

An investment in money market funds is neither insured nor guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. Although money market funds seek to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in these funds.

However, more than four years have passed and persistently high unemployment and continued uncertain economic recovery recently prompted the Fed to state that it intends to keep its benchmark interest rate at near-zero levels until the U.S. unemployment rate falls to at least 6.5%. This has continued to suppress the yields on short-term investments, such as certificates of deposit (CDs), bank deposits, money market funds and other short-term bond funds.

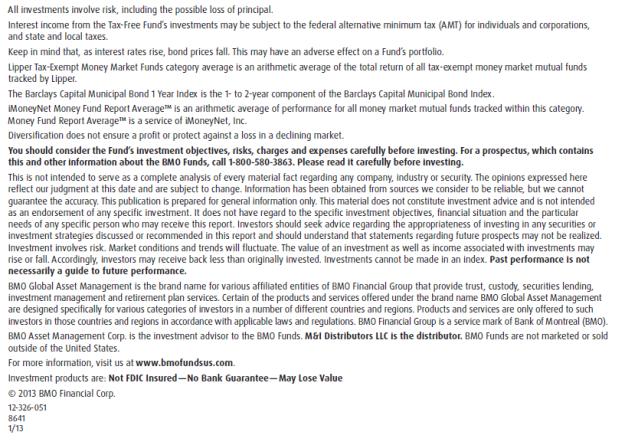

In fact, as Figure 1 demonstrates, yields on short-term investment securities have declined dramatically in recent years. For example, as recently as 2007, the three-month U.S. Treasury Bill yielded more than 5.00%. Today, that same Treasury yields less than 0.10%.1 In real terms, this means a $100,000 investment would have generated annual income of over $5,000 in 2007, compared with less than $100 today. Interest rates have also declined in other sectors of the bond market beyond Treasurys. Corporate bond yields and tax-free municipal bond yields have also fallen over the last several years. While the equity market has rebounded to pre-recession levels, many of these investors continue to be far more concerned with principal protection and liquidity than about yield. However, limiting a portfolio to cash, money market funds and U.S. Treasurys presents its own risks — namely that investors may be locking in yields that are too low to meet their larger financial goals or to keep pace with inflation.

Putting Fixed Income Portfolios to Work Now

Fortunately, there are short- and intermediate-term fixed income investments that offer more attractive yields without undue risk, some of which also can provide tax-advantaged income. These investments typically either have slightly lower credit ratings or slightly longer maturities than money market funds and other traditional cash holdings.

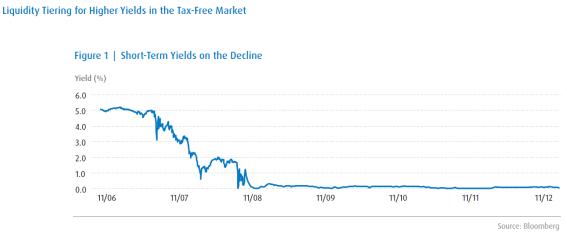

Generally speaking, the lower the credit quality, the greater the spread between yields relative to a higher quality. Similarly, when two fixed income investments have different maturity dates, the one with the longer term typically will pay a higher yield. Figure 2 on page 3 illustrates that by both extending out maturity dates and/or investing in lower quality bonds investors can be rewarded with higher yields. The light blue line shows the various yields for a AAA rated tax-free municipal bond at various maturity dates. The dark blue line illustrates the yields for a lower quality A rated tax-free municipal bond at the same maturity dates.

With yields hovering near or at historic lows, many investors are growing increasingly concerned that interest rates and inflation have nowhere to go but up. As a result, they’re reluctant to venture beyond cash deposits and other investments that offer daily liquidity. But remember, there’s an opportunity cost to limiting a portfolio’s exposure to only the shortest and most liquid securities.

For retail investors the average tax-free money market fund yield is approximately 0.02%. For comparison, a one-year AAA rated tax-free security offers a yield of over 0.20% and a five-year is yielding over 0.80%, as of December 20, 2012. What this suggests is that investors who are willing to take on a little more risk and principal volatility may be able to boost their overall portfolio returns by moving just slightly out on the yield curve. For example, over the last five years, the Barclays Capital Municipal Bond 1-Year Index returned 2.58% annually versus 0.63% average annual return for the Lipper Tax-Exempt money market category.

Past performance is no guarantee of future results. U.S. Treasurys are backed by the full faith and credit of the U.S. Government, whereas mutual funds are not. Bank and thrift deposits are insured by the Federal Deposit Insurance Corporation (FDIC). Credit Union deposits are insured by the National Credit Union Administration.

Why Duration Matters

Gauging the risks posed by rising interest rates isn’t an easy task, even for financial professionals. In general, as interest rates go up, the value of debt securities goes down. How much so? Duration, which is expressed in years, measures an investment’s sensitivity to rising or falling rates and is an important tool investors use to evaluate their exposure to interest rate risk. The rule of thumb is that for every one percentage-point increase in yields, an investor can expect to lose an amount equal to the fund’s duration.

This means that if interest rates rose 1%, investors in a bond fund with duration of five years could see their principal value fall as much as 5%, before considering the income they would receive. Duration matters less for investors in shorter maturity investments. That’s because the shorter the average time to maturity, the less sensitive the fund’s value to interest rate changes.

Enhancing Returns by Tiering Liquidity

The decision of whether to reach for yield by moving down the credit-ratings ladder or stepping out on the yield curve depends largely on an investor’s risk tolerance and his or her liquidity needs. For example, if cash is needed to cover everyday expenses, it makes sense to focus on low-risk money market funds and cash deposits that offer a constant net asset value. Conversely, if cash is intended to fund longer-term needs, such as college tuition in five years, an investor may be able to ride out some degree of short-term volatility in exchange for a higher yield.

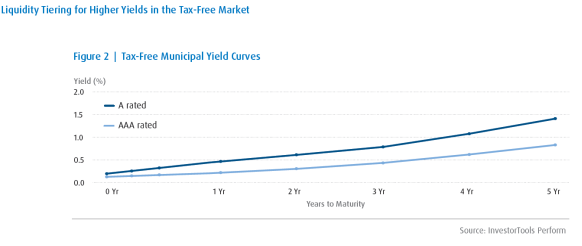

As shown in Figure 3, liquidity tiering is a simple framework that can help investors create more effective fixed income portfolios by allocating their assets into four distinct segments based on their short- and intermediate-term requirements. Each tier becomes progressively more aggressive, allowing investors the opportunity to increase their overall return while maintaining a measure of stability and liquidity in historically conservative positions.

Liquidity tiering is a method of dividing cash and other fixed income assets into distinct categories and investing each set in appropriate strategies in order to optimize the potential for return.

Tier 1: Operating Cash

The purpose of the first tier is to meet immediate day-to-day cash needs. These funds should be invested in traditional money market strategies and/or FDIC-insured bank accounts to help ensure capital preservation and daily liquidity.

Tier 2: Core Reserve Cash

The aim of the second tier is to provide liquidity for ongoing funding needs. Tier 2 assets still should be invested conservatively; however, moving a step further out in duration opens the door to investment in high-quality debt with maturities beyond one business day, such as an enhanced cash or an ultrashort bond fund, that can potentially enhance yield and better match intermediate cash liabilities.

Tier 3: Short-term Assets

The third tier would consist of assets intended to help meet spending needs a year or more into the future. This portion of the fixed income allocation could be invested in short-term and low duration bond strategies to provide a higher potential return while maintaining principal preservation.

Tier 4: Strategic Assets

Finally, the fourth tier would consist of assets intended to meet longer-term needs. Tier 4 assets could be invested in an intermediate-term fund, which may provide an attractive tradeoff between interest rate risk and the potential for higher returns.

The Advantage of a Liquidity Perspective

The management of cash to meet spending needs has grown more complex since the recent credit crisis. How can investors maximize the income available from their bond portfolio in today’s lowrate environment while remaining well-positioned for whatever comes next?

An experienced financial professional with access to cash management expertise can show you a more effective approach to managing your fixed income portfolio by helping you to match your holdings with your liquidity needs. Equally important, he or she can help you select an investment management team that has successfully managed cash and bonds across market cycles — one that offers a choice of actively managed solutions to help boost the effectiveness of your portfolio while safeguarding against the challenges of today’s uncertain markets, including:

• Tier 1: Operating Cash Solutions that provides daily liquidity to meet current needs.

• Tier 2: Core Reserve Cash Solutions that use a slightly longer duration to enhance yield.

• Tier 3: Short-Term Asset Solutions that seeks to maximize total return consistent with current income by focusing on intermediate-term investment grade bonds and notes.

• Tier 4: Strategic Asset Solutions

Seeks to provide a high level of current income that is free from federal income taxes, consistent with preservation of capital by focusing on high-quality municipal bonds. Each of these funds benefit from active management of credit, duration and sector positions, enabling them to take advantage of structural opportunities that currently exist in so-called “safe spread” sectors of the fixed income market.

These short-term and low duration strategies have potentially higher yields because they invest in securities with slightly longer maturities and lower credit ratings than money market strategies. The fixed income markets are always changing. With a diversified portfolio allocated according to liquidity needs, investors have the potential to achieve an optimal balance between stability and yield, regardless of market conditions.

1Daily Treasury Yield Curve Rates. U.S. Department of the Treasury Resource Center. www.treasury.gov.