Animal Spirits: F.I.R.S.T.

F.I.R.S.T.: Fixed Income Research and Strategy Trends

“I am not a destroyer of companies. I am a liberator of them! The point is that greed, for lack of a better word, is good. Greed is right, greed works. And greed, you mark my words…will save that other malfunctioning corporation called the USA.”

— Gordon Gekko, Wall Street

Call it what you will — a dog-eat-dog world in which you’re wearing Milk-Bone underwear or an example of capitalism at its finest — an M&A cycle is heating up. This activity may be signaling the rebirth of what British economist John Maynard Keynes originally referred to as “animal spirits”, much to the delight of fictional corporate barbarian Gordon Gekko and his real-life analogues, who require little prompting to act on Keynes’ “spontaneous urge to action”. In the voracious search for yield — and with borrowing costs held artificially low by the Fed for the foreseeable future — the appeal of gobbling up undervalued assets is palpable and could very well be the next natural and exciting progression in America’s virtuous recovery.

Hey, it’s been working wonders for the housing market, so why not the corporate sector? A leveraged buyout here and a little operational expansion and cost-cutting there, the next thing you know organic growth percolates earnings, multiples expand, and the debt load eventually becomes more manageable. This is good for equity returns and, in turn, for a sputtering U.S. economy in desperate need of growth. On one hand, liberating dormant, defensive liquidity in pursuit of higher-yielding, offensive ends could contribute to a cyclical upturn in economic growth, just as it has for the recovering housing market. On the other hand, when a spirit of ebullience turns to one of greed — well, you don’t have to re-watch Wall Street to see where that can lead you.

Animal spirits last wreaked their destructive side effects in 2008 — the peak of the previous M&A boom that started in 2003. The swell in M&A activity we are witnessing today appears to be in its nascent stages, far from the “big hat, no cattle” days of the post-9/11 leveraged-buyout surge. But let’s face it: All M&A activity is not created equal. Michael Dell putting up a significant portion of his own personal fortune to take his company private and work toward the preservation of his and its long-term legacy is one thing; the Oracle of Omaha Warren Buffett and Berkshire Hathaway joining forces with a Brazilian private-equity firm to squeeze some ketchup out of HJ Heinz is another.

Regardless of their motivations — legacy preservation or the urge to unlock cash flow — these and other M&A deals could be a collective positive, compelling expressions of how the return of leverage can help investors and America achieve productive ends. But the significant pickup in high yield debt and leveraged loan issuance so far in 2013 as a result of the increased M&A activity has raised concerns that the vigor and velocity with which money in search of yield is being enticed into corporate debt funds may potentially spawn a credit bubble. We’ve seen this movie before, and these concerns are certainly warranted.

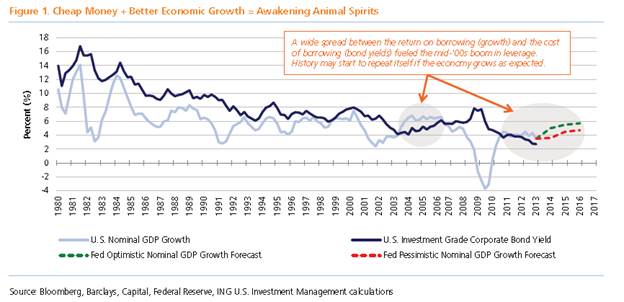

Nominal GDP growth, which is highly correlated to corporate revenue growth, has been above the average borrowing rate for investment grade U.S. corporate issuers since the middle of 2010, a function of the Fed’s extraordinary suppression of U.S. interest rates (as discussed in February’s edition of F.I.R.S.T.). Going back to the secular peak of U.S. interest rates in 1980, there was only one other sustained period during which the economy was growing faster than the average borrowing cost for higher-quality companies: 2003–06, which became a boom time for every kind of leveraged transaction imaginable — CLOs, CDOs, LBOs and, eventually, the dreaded subprime mortgage-backed security.

Greed was good; the spread between rates of return and costs of capital was large, and borrowers of all flavors and credit quality took advantage of the cheap money bacchanal, culminating with nearly $800 billion in LBO activity during 2006 and 2007. Greed turned out to not be so good, however, when U.S. house prices and economic growth both began to decline, ruining the aggressive return assumptions built into all that leverage.

Roll the tape to 2013: What do we see? High-yielding debt and loan issuance are both ahead of last year’s pace and would surpass the 2007 peaks if they continue at their current clips (see Figure 2). So we ask: Is all this cheap money reviving the animal spirits that John Maynard Keynes so famously wrote about nearly eight decades ago? And, if so, is greed perhaps exactly what the U.S. economy needs right now?

While the strong demand for corporate credit has boosted both the price and new supply of corporate debt, the end-usage of that debt has hardly been aggressive. Just over 70% of new bond and loan issuance has been used to refinance existing debt — much of which was debt that was issued during the pre-2008 credit boom — while less than 25% has been used for M&A or LBO activity (compared to 50% in 2007). Said another way, it looks like companies are still working to improve their profitability via cost reductions (interest costs, in this case), which is a reflection of current modest economic growth rates. Borrowing when the economy is growing at 4% or less is not as exciting as when the economy is growing at 6% or more. Saving money via refinancing, however, is merely a short-run solution to a longer-term problem of inadequate growth.

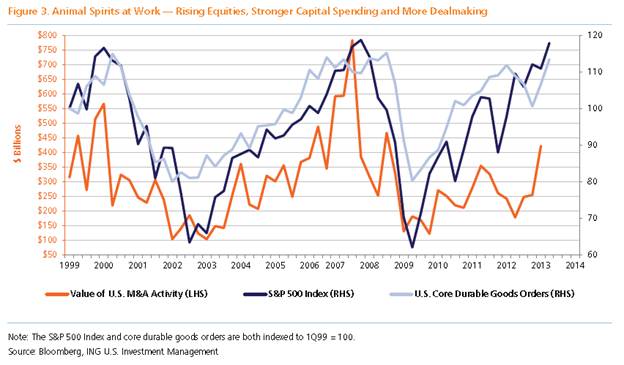

As the economy continues to improve, more companies will hopefully look to improve profitability by taking their dormant cash down higher-yielding avenues, like real investment and the building of businesses. However, a time will come when the combination of cheap money, rising asset values and improving economic growth will inspire a new breed of Gekkos to hunt for an increasing number of badly managed companies from which to extract cash or “shareholder value” with little regard for anything but a buck. Given the strong improvement in U.S. equity values, the rebound in capital spending and the increasing number and size of M&A transactions (Figure 3), this process looks be underway already; greed, however, appears to be behaving itself for now.

But even if the animal spirits nowadays don’t all subscribe to the anti-Gekko philosophy that concludes Wall Street — “Stop going for the easy buck and produce something with your life” — the transition from a defensive application of excess liquidity to an offensive one could be the spark the economy needs to create growth and achieve productive ends, liberating our malfunctioning economy from the destructive forces of deflation in the process.

This commentary has been prepared by ING Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors. Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 5874

© ING Investment Management