“I don’t pay you to write a newsletter, I pay you to manage my money.”–Anonymous Client

Please pardon the tardiness of this Q1 commentary about the whacked-out, overpoliticized, central-banker-meddling investment environment we currently live in. January and February were a challenge for our rebalancing process as the equity markets celebrated their best January since 1994, and our focus on repositioning the portfolios required that we redouble our normal diligent attentiveness to the markets.

I predict the Ides of March will find us in a continued sequestration, and Congress will use the time between now and the debt ceiling deadline on March 27th to debate the merits of true tax reform as opposed to governing by crisis. In the end, though, the reform conversation will revert to governance by crisis, with another stop-gap measure to avoid government shutdown during Holy Week and Easter, which will tide us over to the elections of 2014. Do you expect any different?

Let's look at what we have learned from the 2012 election: 21 of 22 incumbent senators were re-elected, as were 353 of 373 incumbent members of the House. The American people thus re-elected 94 percent of the incumbents to an institution that has an approval rating of about 9 percent. In other words, nothing has changed. This indicates that, as an electorate in desperate need of leadership and change, we are a nation of idiots. We're now stuck with the useless, dysfunctional government that we deserve. The only good news is that the investment markets seem to be blithely ignoring the US government’s ineptness, and the Dow averages are surpassing their 2007 all-time highs as I write.

I have remarked in prior first-quarter newsletters that the passing of the New Year is about the only time of year when most people reflect on the past, ponder the present, and plan for or try to predict the future. The New Year always brings with it the crystal-ball question, “Cliff, where do you see the markets over the next year?” Like most market pundits I am tempted to answer with absolute numbers, but experience has taught me that these types of predictions tend to prove me far smarter or dumber than I deserve. There are, however, several themes we have identified that will affect our asset-allocation discipline for 2013. As I commented in November, the market risks are geopolitical and the sentiment is driven by government policies. Our themes for 2013:

- The Slowest Train Wreck: Europe

- Buzz Lightyear International Monetary Policy

- Energy Is the Answer

- Main Street versus Wall Street

The Slowest Train Wreck: Europe

In 2011, Jean-Claude Juncker, the prime minister of Luxembourg, denied attending a meeting about the restructuring of Greek debt. When that falsehood was exposed, Juncker responded, “When things get serious, you just have to lie.”

Which pretty well sums up the consensus of elected officials in dealing with the massive deleveraging and insolvent banks of the EU. The eurozone –an amalgamation of 17 countries, 100 political parties, and 20 different languages – is hobbling along without fiscal union, political union, or banking union created by a central bank charter. The force that holds the euro together is Germany, which, since the creation of the euro and the institution of trade agreements to open borders, has enriched itself, with the unintended consequence of impoverishing its southern EU neighbors. Germany now has to make the unenviable decision whether to support the euro and with it Mario Draghi and the European Central Bank, or to play the world’s biggest game of chicken in the global currency markets. I do not see a clear direction emerging from Germany regarding euro support until after the German elections in the fall. Therefore, in the near term, I expect a continued kicking of the well-dented monetary can down the road, through a combination of the ECB’s ability to purchase Greek, Italian, and Spanish bank debt and plenty of rah-rah rhetoric from Draghi.

Eventually, however, Germany will no longer be willing, in order to back up the euro, to prop up banks that would otherwise fail in Greece, Spain, and Italy. While the euro will not disappear, there will be fierce resistance from France, Italy, et al. to a central bank charter with Germany in control. And yes, Germany will either assert control or opt out of the discussion regarding a central bank charter and establishment of the equivalent of a US Federal Reserve as part of the ECB.

Evidence of Germany’s intent to take control of the ECB is seen in their announcement on January 16th that they would repatriate their physical gold from US and French bank vaults. The Bundesbank indicated its intent to withdraw 674 tonnes from US vaults over a seven-year period; however the 374 tonnes in France is to be transferred as soon as possible. Taking back their gold from the French is a sign that Germany is going to stop playing Mr. Nice Guy to France and is prepared to assert more leverage over the future of the Euro. Germany is fighting for control of the ECB against a group of mostly southern states, led by France; and the outcome will impact debt markets, unemployment, and social stability. Holding Germany’s gold in the US, England, and France post-WWII was a quasi-insurance policy that Germany would not start another war. However, since the Germans have already conquered all of Europe economically, the war now will be for control of the shared currency, banks, and trade.

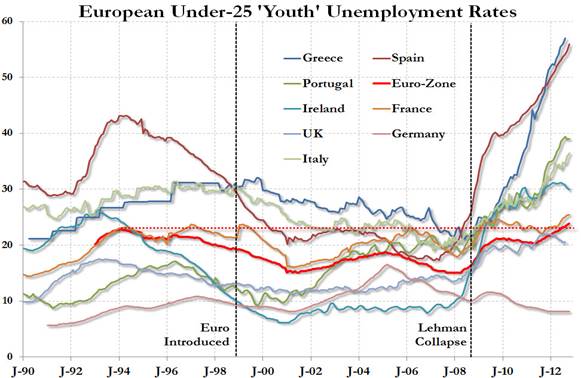

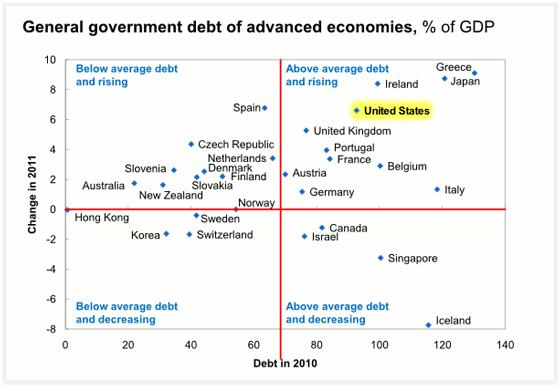

Two scary charts:

When you get massive unemployment of the type being experienced in Greece and Spain, particularly among those 25 and younger, combined with severe austerity measures imposed by the “German Oppression,” then the time is ripe for revolution, or at least for the restructuring of entire government systems. The problems in Spain and Greece have not gone away. And, the recent election results in Italy point towards Southern Europe’s unwillingness to remain under the German boot. But make no mistake, for the Germans to continue supporting the ECB, they will demand further austerities from Spain, Greece, and Italy.

Although Mario Draghi has been successful in restoring confidence in the euro by resorting to the same bazooka tactics as his Keynesian Kousin Bernanke, the ECB’s charter still lacks the basic tenets of a central bank. Germany, known for its silver bullet trains and on-time efficiency, is about to engineer the slowest economic train wreck the world has ever seen.

This link is to GMO’s James Montier and his commentary on “Hyperinflations, Hysteria and False Memories”.

I encourage you to read his analysis, but I will attempt to summarize Mr. Montier’s plausible case that hyperinflations are not simply the result of central banks printing money to finance government debts. According to his thesis, three other conditions need to accompany the printing of money:

- A large supply shock – the most common event that causes this is war. There needs to be a significant interruption of a country’s ability to produce goods and services. The scarcity of goods leads to rapidly rising prices, which leads to printing even more money.

- Large debts denominated in foreign currencies – leads to currency devaluation. In the case of the US, we would have to owe debts issued in yen, euros, or yuan that would be payable only in the foreign currency, not in US dollars. In Europe, they would owe debts in US dollars or yen, for example. When your currency is falling versus other currencies, you print more money.

- Distributive conflict/transmission mechanism – without which hyperinflations flare out.

In the conclusion of his article James states:

On the basis of these preconditions, I would argue that those forecasting hyperinflation in nations such as the US, the UK, or Japan are suffering from hyperinflation hysteria. If one were to worry about hyperinflation anywhere, I believe it would have to be with respect to the break-up of the eurozone. Such an event could create the preconditions for hyperinflation (an outcome often ignored by those discussing the costs of a break-up). Indeed, the past warns of this potential outcome: the collapse of the Austro-Hungarian Empire, Yugoslavia, and the Soviet Union all led to the emergence of hyperinflation!

Again, I recommend taking time to read Mr. Montier’s commentary; his history lesson of the various hyperinflations is enlightening. The potential breakup of the euro is, in my opinion, the most serious economic risk on the horizon.

Buzz Lightyear International Monetary Policy

My sons are now 21 and 17 years of age, and so it has been some time since I had to sit through a lot of animated movies. However, memories linger. The first feature-length computer-animated film, released in 1995, was Toy Story, featuring Woody and Buzz Lightyear. “To Infinity and Beyond!” was yelled in my home for weeks on end, to the point where the movie was almost banned from our VCR.

Now, Japan, the United Kingdom, the eurozone, and the US seem to have adopted a monetary policy that embodies Buzz Lightyear’s mantra. Or perhaps they are taking up Captain James T. Kirk’s promise to “boldly go where no man has gone before.” Either motto is a perfect fit as our intrepid global leaders set out for the Keynesian frontier they are so eager to explore. Why have the US, Europe, and now Japan so enthusiastically embraced John Maynard Keynes’ recommendations for government intervention, while ignoring Ludwig von Mises’ Austrian model, Irving Fisher’s work on debt deflation, and even the more recent challenge by Milton Freidman to naïve Keynesian economic policies that promote the government’s role in free markets? Since we can’t answer that one, perhaps we’d better just ask, how do we manage our investments in a market environment so dependent on Keynesian monetary stimuli, where predictions of future macroeconomic and geopolitical behavior are nigh on to impossible?

Although we have been assured by Mr. Bernanke in his latest testimony before Congress that the Fed has its thumb securely in the dike of inflation and stands willing to transform QE should inflation start slopping over the top, he also countered that statement by saying that the risks of killing the recovery far outweigh the risks of inflation. Keep in mind that this is the same individual who in 2006 commented that the prices of houses simply reflected the overall strength of the economy and had nothing at all to do with a financially engineered bubble in housing or with abuses such as NINJA loans granted with government guarantees from Fannie and Freddie – no income, no job, no assets, but your government would like to give you a 100%, no-equity loan for a house you cannot afford.

The Fed’s current behavior can be viewed as a symptom of continued problems in the banking system, particularly with regard to housing and real estate. Bubbles when they burst don’t repair themselves quickly. As Mr. Bernanke reiterated in this past week’s Congressional testimony, the Fed can do little to stimulate the economy, but it can create inflation and reassure the investing world that the Bernanke Put is still good.

Nevertheless, it seems to me the Fed’s top priority in the months ahead will not be inflation or jobs but rather continuing to prop up the banking system and to provide back-up liquidity to the US Treasury. In the long term, direct monetization of Treasury debt will tend to weaken the US dollar, boost oil and gasoline prices, boost money supply growth, and spur domestic inflation. In the short term, the dollar is still the cleanest dirty shirt in the currency closet and is appreciating, while stocks will act as inflation hedges, bonds will continue to return paltry yields relative to their risk, and government entities will continue to kick the can of fiscal responsibility down the road as long as the central bankers are willing to bail them out.

For now, you cannot fight the Fed, the Central Bank of Japan, and the ECB with their ongoing parade of cheap money. The excess liquidity being pumped into the investment world will have to go somewhere, and it will pour primarily into stocks and bonds, as investors and bankers around the world remain reluctant to buy or loan money on illiquid assets. The world is all too aware that any sudden shift in monetary policy could cause a reaction in the markets overnight, and so adequate liquidity is required.

The unintended consequence of the market’s Keynesian high is another “Minsky moment” is in the making; I just cannot tell you when or where. Paul McCulley of PIMCO coined the phrase to describe the 1998 Russian financial crisis. A Minsky moment comes after a long period of financial prosperity and increasing value of financial assets lead to speculation and investors willing to use borrowed money. At some point the markets reverse, and indebted investors are forced to sell assets to pay back loans. The concept ties into von Mises “Austrian School,” which theorized that the prolonged use of low interest rates by central bankers leads to excessive credit expansion and economic bubbles. The longer the markets remain complacent about low rates and the willingness to use leverage, the bigger the bubble grows and the louder the pop when it bursts. When that moment will arrive this time around is anyone’s guess; but for now, don’t fight the Fed.

Energy Is the Answer

The USA is a blessed country. Despite our political issues, debt issues, future entitlement liabilities, and seemingly unsustainable healthcare system, our country is blessed with three assets that are unmatched by those of any other single country in the world: energy, water, and food. The US economy enjoys a distinct advantage over the next two largest economies, China and Japan, and that is that we do not have to worry about our supply chain for food, water, and energy. We have competitive advantages that China tries to offset with cheap labor and Japan through a cheaper currency. However, energy and food are keys.

The recent boom in US natural gas production has driven the price down from $11 per million BTU two years ago to under $3 in 2012. The chart below is a sampling of the costs of natural gas around the world in July of 2012, by the Federal Energy Regulatory Commission. The thing that leaps out from this chart is the low cost of US gas versus the cost in the rest of the world. Because of the US boom in natural gas supply, there is an opportunity for public/private partnership between the US government and the gas producers, which would be a win-win for everyone in the game of exporting. Obama could, with thoughtful export policies and taxation of the export facilities, potentially pay for future entitlement and healthcare spending for the next twenty to thirty years. Such a program will require compromise, and with the recent appointment Ernest Moniz as Energy Secretary, we may see initiatives in 2013 to convert LNG import facilities to export facilities. On January 13, 2013 a bipartisan group of US Senators introduced legislation to amend Section 3© of the Natural Gas Act in order to expedite Dept. of Energy review processes. In my opinion this indicates a willingness by Congress to promote the exporting of natural gas.

A Global Perspective on Natural Gas Prices

World Natural Gas Price Samples 7-9-2012, Data in $US/MMBtu. Image Credit: Federal Energy Regulatory Commission.

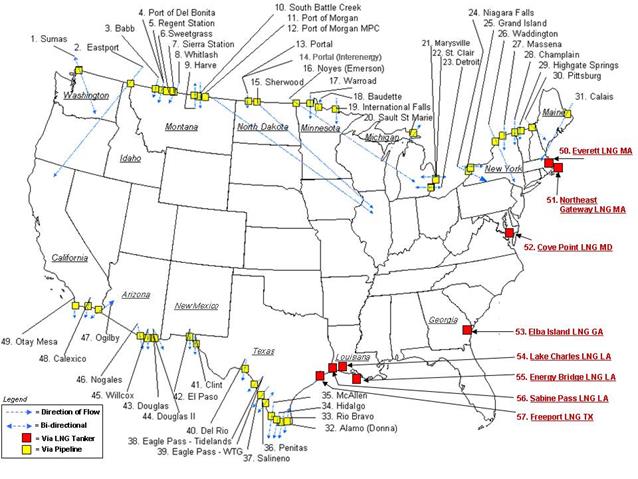

US Natural Gas Import/Export Locations as of 12/31/2008

Converting an LNG import facility to an export facility is not as simple as flipping a switch. Lots of permitting (read: government revenue) is required, including engineering studies and environmental impact reports; and retooling the import facilities will take time and money, lots of money.

The US is capable of becoming a net exporter of energy, thereby promoting jobs and GDP growth for years to come. The resources are within our grasp to enhance tax revenues and help pay for the future expenses of Social Security and healthcare. And I am not even discussing the potential for further oil exploration beneath federal lands such as ANWAR in Alaska. Before I get the environmentalists screaming that all oil companies are evil, hydraulic fracturing should be banned, and the potential contamination of groundwater outweighs the merits of providing healthcare and Social Security benefits to our citizens, I need to state that I am not a chemical engineer. I have limited understanding of the issues involved in fracking, offshore drilling, and drilling on federal lands. I acknowledge there are right ways and wrong ways for things to be done. Corporations will cut corners and EPA enforcers will overreact, but we have to find ways to compromise. There is a tremendous opportunity for the US to right its fiscal ship without taxing the general populace out of their homes. For without the revenues and jobs that future oil and gas exports could bring, I do not see a way out of the systemic mess the last 50 years of misguided federal spending have gotten us into.

Main Street versus Wall Street

That was then, this is now:

October 9, 2007 versus March 5, 2013

- Dow Jones Industrial Average: then 14164.5, now 14164.5

- Regular Gas Price: then $2.75, now $3.73

- GDP Growth: then +2.5%, now +1.6%

- Americans Unemployed (in Labor Force): then 6.7 million, now 13.2 million

- Americans on Food Stamps: then 26.9 million, now 47.69 million

- Size of Fed Reserve's Balance Sheet: then $0.89 trillion, now $3.01 trillion

- US Debt as a Percentage of GDP: then 38%, now 74.2%

- US Annual Deficit: then $97 billion, now $975.6 billion

- Total US Debt Oustanding: then $9.01 trillion, now $16.43 trillion

- US Household Debt: then $13.5 trillion, now 12.87 trillion

- Consumer Confidence: then 99.5, now 69.6

- S&P Rating of the US: then AAA, now AA+

- 10-Year Treasury Yield: then 4.64%, now 1.89%

- EURUSD: then 1.4145, now 1.3050

- Gold: then $748, now $1583

- NYSE Average LTM Volume (per day): then 1.3 billion shares, now 545 million shares

Main Street is not sharing in the wealth of Wall Street. While the Dow sits at all-time highs, most of Main Street still suffers from high rates of unemployment, with future layoffs coming in the wake of the sequestration and declining consumer spending from higher taxes that kicked in on January 1, 2013. Main Street investors also have not participated in the rise of stocks over the last five years, as shown by this chart from Ryan Detrick:

Wall Street is getting richer; Main Street is getting poorer. This is an unintended consequence of the Fed’s zero-interest-rate policy. Low interest rates have killed middle- and lower-income retirees and savers, as they don’t think they can afford the risks of stocks, yet CDs and other “safe-yield” vehicles give them only a fraction of the income they earned from investments five years ago. I see nothing in the policies of the President, Congress, or the Federal Reserve that is going to change the continuously widening separation between the wealthy and the poor in this country.

Summary

In our opinion, in the current economic environment, yields simply cannot go any lower. Austerity policies will persist in Europe and eventually come to the US. The Fed stimulus has lost its ability to impact unemployment; and the economy is running out of steam, because consumer spending is being hit as a result of the FICA and Obamacare tax increases that went into effect on January 1.

We will remain disciplined in our approach to the markets, as protection of principal and the recognition of risks are the foundation of our process. Our tactical allocation process does have a “value” bias, and while this has its virtues, very few people have the temperament to stay disciplined. The reason they don’t is that, when you take this approach, there will be times when others are making more money than you, and while you’re at the plate patiently waiting for the fat investment pitch, the owners and fans are screaming, “Swing, you bum!” To endure the ridicule of not keeping up with the market and to lose business in the process is never easy. It is particularly challenging to connect with the arc of opportunity in today’s environment, with the ever-shifting winds of regulatory policy, tax and monetary policy, and currency wars that reshuffle the scoreboard of winners and losers on a monthly basis. Discipline and patience are tough to maintain when the markets are snorting monetary cocaine, ignoring valuations, ignoring inept governments, and embracing risk to avoid earning zilch in money markets and short-term “safe” investments. At Excelsia, we will stay the course. Good luck out there.

Cliff

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Excelsia, Inc.), or any non-investment-related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Excelsia, Inc. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Excelsia, Inc. is neither a law firm nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Excelsia, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.

© Excelsia Investment Advisors