In this report, we highlight benchmark changes in a major player, a potential substitute (with cheaper fees) for another major player, a new player with an innovative weighting scheme and provide an overview of the Emerging Market ETF space available to investors.

The Implications Of Largest EM ETF Switching Benchmark Indexes

Vanguard’s FTSE Emerging Markets (VWO) and BlackRock’s iShares MSCI Emerging Markets (EEM) are by far the two largest EM ETFs, with $60 billion and $52 billion US in assets under management respectively as of December 2012. To put that into perspective, the Emerging Market ETF universe we track is composed of 202 ETFs, with total assets under management of $192 billion US. Any changes to these two EM ETFs is big news. Up until late last year, both ETFs tracked the MSCI Emerging Market Index; however, Vanguard has announced it is switching the benchmark of VWO to the FTSE EM Index. This transition will be gradual, occurring over the first six months of 2013. But what does this mean for investors?

- The Future Performance Divergence Of These Two Popular Emerging Markets ETFs.

With this change of index, the VWO and EEM will no longer be twins. Well before the change, the only differences between the two were the fee structure and the number of holdings. VWO has lower expense ratio (18 bps after a recent cut versus EEM’s 66 bps), and it employs a real full replication strategy (VWO has almost always held more stocks than EEM). Despite these differences, the two ETFs have performed similarly over time, though EEM slightly outperformed over the past five years due to its more successful sampling strategy.

As VWO and EEM start tracking different indices, investors should note their different country inclusion rules. The FTSE EM index does not include South Korea (which is a 16% weights in MSCI EM index), resulting in higher weights in other larger EM countries such as such as Brazil, Taiwan, South Africa and India. It also includes a couple of smaller markets not in MSCI EM index: Pakistan and the United Arab Emirates. With different country weights, the two underlying indices should see different performance going forward.

If choosing between the EEM and the new VWO, we prefer the EEM for two reasons. First, we think that, despite its GDP per capita and other economic measures identifying it as an outlier from other emerging countries, South Korea has strong economic ties with its neighbors, most of whom are emerging markets. The corporate earnings of South Korean companies could well correlate with its regional and domestic economic conditions. For the same reason, our in-house Emerging Market stock universe includes South Korean as well as Hong Kong and Singapore listed companies.

Second, the MSCI Emerging Market Index is still the more broadly tracked performance benchmark index, not just by ETF providers, but by other active portfolio managers. For that reason, the new VWO incurs additional tracking error for investors who desire beta exposure. (We are referring to the performance deviation of VWO from the more popular EM benchmark, in additional to the deviation from its own underlying tracking index compiled by FTSE).

The New Lower Cost Emerging Market ETF Tracks A Broader Universe

The second development in this space is the recent launch of the “iShares Core MSCI Emerging Markets ETF” (ticker: IEMG). This ETF tracks the MSCI EM Investable Market Index (IMI) not the more popular Emerging Market index. The difference? The new ETF includes many more small cap stocks. (And instead of charging 0.66%, it has an starting expense ratio of 0.18%.)

- What to Choose? EEM, IEMG or VWO?

As long as the most popular EM performance benchmark remains the MSCI EM Index, and as long as this index includes South Korea, it does not make much sense for “beta exposure” investors to buy the new VWO without South Korean stocks. The future performance divergence between the EEM and VWO could be significant due to their different country weightings, and using VWO could require a lot of explanation down the road if your yardstick for performance is the MSCI EM index.

But between the EEM and IEMG, we vote for the latter. The IEMG tracks the whole MSCI-defined investable EM universe of more than 2600 stocks, while the EEM tracks the largest 800 or so stocks in the same universe. Comparing the holdings of EEM and IEMG, we found that almost all of the holdings of EEM are included in IEMG, and these Large and Mid Cap companies account for more than 88% of the IEMG portfolio weights. The IEMG adds a large number of small caps, whose weight contributes 12% of the ETF portfolio. Since positions of both ETFs are cap weighted, the performance of the two ETFs tracks each other closely. Obviously, the addition of a large number of small cap companies has marginal impact on the performance.

But here is where BlackRock hands you a bargain. Instead of paying 0.66% for EEM, you can buy IEMG for the same performance but at a much lower expense ratio. Why would BlackRock do this? The most likely reason is BlackRock is competing with other lower cost EM ETF providers, including Vanguard. By offering an alternative product to its own EEM at competitive prices, BlackRock is hoping to gather new assets that would otherwise go to other low cost EM ETF providers. This is better than cutting the price on their existing flagship EEM. Our guess BlackRock is crossing its fingers that current EEM holders will stick around, failing to see just how similar the two are (except in the pricing structure of course). But for someone willing to do a little bit of investigation, the switch makes a lot of sense.

- IEMG’s Potential Impact on Emerging Market Small Caps

While including small caps might not have much impact on the performance of IEMG, it could have a significant impact on the small cap names it holds. The obvious benefit is the buying power. When BlackRock keeps creates new shares for IEMG, it supports the prices of these small cap companies. (though when BlackRock has to dissolve shares, the selling pressure could upset the small caps on the downside as well). However, we expect the migration of investors from EEM to IEMG and the ramping up phase of IEMG will boost small cap names in the Emerging Markets. Additionally, even if the support of prices is a two-way street, the improvement in liquidity will not hurt either.

A New Emerging Market ETF With A Different Sector Weighting Scheme

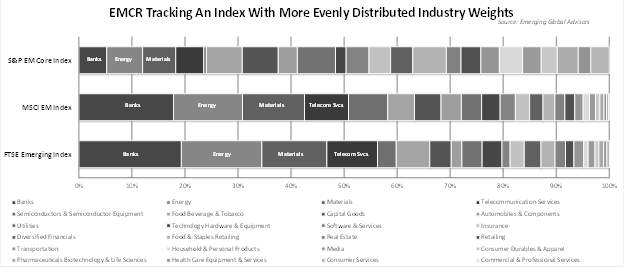

The last development is a new product from a much smaller ETF provider: Emerging Global Advisors. In the past, we’ve highlighted several of their innovative Emerging Market ETFs, including their ten Emerging Market sector ETFs. The company recently launched a new ETF called the EGShares Emerging Markets Core ETF (ticker: EMCR),which tracks the S&P Emerging Market Core Index and addresses the sector/industry concentration of traditional Emerging Market indices.

We’ve previously discussed the MSCI EM benchmark’s concentration in more mature sectors and its underweight of the Consumer Discretionary and Health Care sectors. The FTSE EM Index has the same issue, if not worse. The top three sectors for both indices are Financials, Energy and Materials, accounting for more than 50% of overall index weights.

The bias is more evident when the 10 sectors are broken into the 24 GICS Level II Industry Groups. The top three (Banks, Energy and Materials) Industry Groups account for more than 40% of the MSCI EM Index and close to 50% of the FTSE EM Index. Buying the ETFs tracking these two indexes gives you a lot of exposure to these mature sectors and industries.

By using a different weighting scheme, the underlying index of EMCR evenly distributes the industry weights, and the combined weights of the top three industries are cut by more than half. The chart below from Emerging Global Advisors illustrates the differences between the three indices in terms of industry weight distribution (the first Index is the underlying Index for EMCR).

- Is EMCR A Good Fit for You?

EMCR is not a traditional “tracking the broad Emerging Market” type of product. The performance of EMCR could deviate significantly from the commonly used EM benchmarks due to its unique sector/industry weighting. (For example, the YTD performance of EMCR is almost flat while EEM is down –2.6%.) By dramatically changing the industry weighting scheme, this product deemphasizes more mature, mostly state-owned industries such as Banking, Energy and Materials in the Emerging countries, while highlighting the smaller, more entrepreneurial, and more domestic consumption-driven industries. We share a similar philosophy in terms of long-term industry bets in the Emerging Markets, and are pretty happy there is an alternative to the majority of the EM ETFs loaded up with financials or energy companies.

On the country allocation level, the EMCR is different from the EEM and VWO because it does not include Taiwan and South Korea. According to the provider, the rationale for stripping off the two more developed countries from the EM space is the same as it is for lowering the weightings of the more mature industries. This significant deviation makes EMCR essentially an active product as it inherently places active bets on both the country and industry levels versus the commonly used EM benchmarks.

All in all, the EMCR could be a good choice for investors with different country and industry views from the MSCI EM benchmark, but it might be too innovative for investors who only wish to have beta exposures. Either way, this is by far the most interesting Emerging Market ETF we have seen recently, and it is definitely worthy of consideration.

Conclusions On The Recent Changes

We compared the two most popular EM ETFs (VWO and EEM) and two new EM ETF offerings (IEMG and EMCR). With an index switch slated in the first half of this year, the VWO will no longer closely track the performance of the EEM due to its different country weightings. We conclude the new IEMG is a better alternative for “beta exposure” centric investors, as it provides competitive pricing, while still closely tracking the most commonly used EM Benchmark: the MSCI EM Index. On the other hand, investors with different industry views from this benchmark (like us), the EMCR provides a very good option.

With the changes and launches of EM ETFs, we see smaller EM companies/industries starting to gather more attention. Throughout this article, we’ve provided our EM stock rankings based on our proprietary EM stock model. Additionally, we also argued that VWO’s large scale index switching could mean a trading opportunity in South Korea stocks, and a list of companies which might see higher impact is provided as well.

Mapping The Emerging Market ETF Space

As of December 2012, our quarterly updated EM ETF database is comprised of 201 ETFs (181 Equity ETFs and 20 fixed income ETFs). These 181 Equity ETFs can be further categorized into broad exposure ETFs, regional/country focus ETFs and specialty ETFs (we define specialty ETFs as any ETFs with sector/industry focus or style focus such Growth/Value or Small cap, etc.).

- Broad Exposure ETFs

ETFs in this category track broad emerging market indexes without region, sector or style focus. Due to the dominance of VWO and EEM and cut-throat competition on pricing, new entrants are unlikely. In addition to the five plain vanilla broad exposure EM ETFs (EEM and IEMG tracking the MSCI EM indices, the SCHE and now VWO tracking the FTSE EM index, and the GMM tracking the S&P EM index), there are two levered ETFs and three inverse ETFs.

A short note on the leveraged and inverse ETFs. All five in this category have the MSCI EM Index as their underlying index, but it is no surprise that none delivered the performance indicated by their names. For example, the EDC is the Direxion Daily Emerging Markets Bull 3x Shares with the underlying MSCI EM Index. But while the EEM was up 10.9% for the past three years, the EDC was not up (3x10.9%) but instead down 30%! Leveraged ETFs or inverse ETFs only promise daily returns relative to the benchmark; the EDC only promises to deliver three times the daily return of the MSCI EM index. Because of the up and down nature of the market, over the long term, compounding the 3x daily index returns will never get you anywhere near the 3x holding period returns. Unfortunately for EDC holders, compounding that 3x daily index return after 3 years landed them down 30%, not up 30%.

We’re not getting into a detailed discussion of why leveraged ETFs or inverse ETFs could deviate from the performance indicated by their name. But an article published by Morningstar gives some pretty detailed illustrations. (http://news.morningstar.com/articlenet/article.aspx?id=271892). Just remember, leveraged and short ETFs are only for day traders, not long term investors.

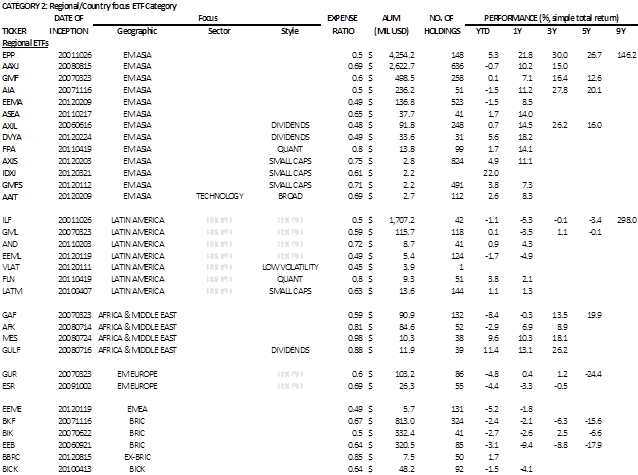

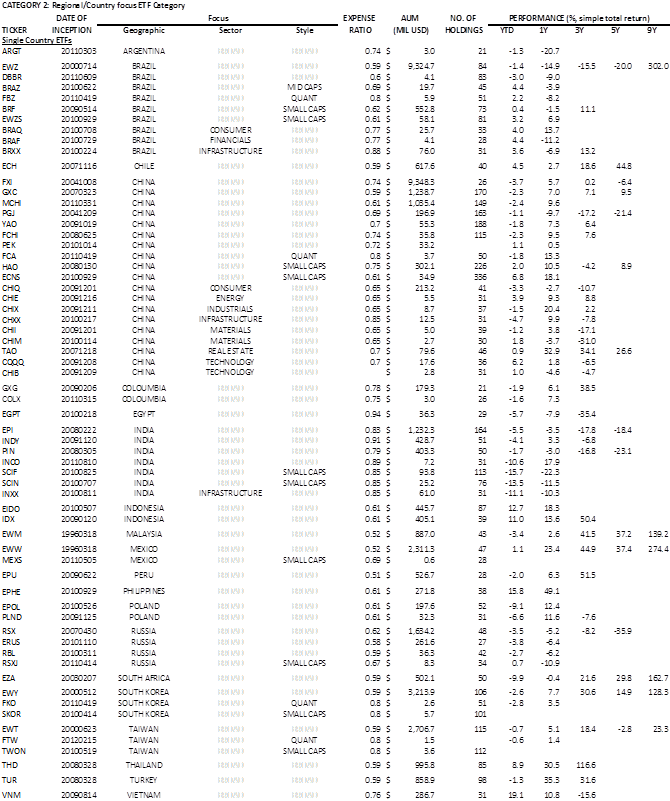

- Regional/Country Focus ETF Category

ETFs in this category track a specific country or region. Unlike broad exposure EM ETFs, investors can utilize these ETFs to express their regional and/or country views. This category can be further broken down by broader regions (table below) and single countries (next page). Some ETFs in this category also have sector/style tilt in additional to their geographic focus.

It is worth mentioning there are two regional ETFs and four country ETFs based on a quant factor screened “enhanced index” (marked “QUANT” in style focus column in the tables). They all track Standard & Poor’s indices then apply a quant screen (including growth factors, valuation factors and price momentum factors) to narrow the broader index universe down to a smaller group of attractive stocks. These ETFs have outperformed corresponding ETFs tracking the unscreened broader market indices (however, only short term performance is observed).

- First Trust Asia/Pacific ex-Japan Fund (FPA) outperformed SPDR S&P Emerging Asia Pacific ETF (GMF)

- First Trust Latin America AlphaDEX Fund (FLN) outperformed SPDR S&P Emerging Latin America ETF (GML)

- First Trust China AlphaDEX Fund (FCA) outperformed SPDR S&P China ETF (GXC)

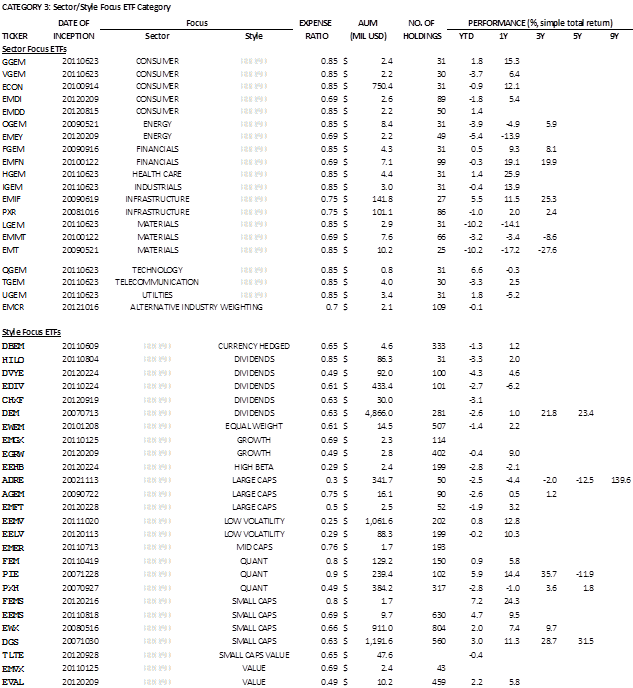

Sector/Style Focus ETF Category

ETFs in this category track the broad emerging markets, but focus on either a particular sector or investment style (Value versus Growth, Large versus Small Caps, etc.). These ETFs are options for investors wishing to have exposure to all emerging countries while emphasizing certain sectors or investment style.

Published By The Leuthold Group, LLC…..Distributed By Weeden & Co., L.P.

The Leuthold Group, LLC provides research to institutional investors. The material herein is based on data from sources we considered to be reliable, but it is not guaranteed as to accuracy and does not purport to be complete. Any opinions expressed are subject to change.

Weeden Investors, L.P., Weeden & Co., L.P.'s parent company, owns 22% of Leuthold Group’s securities. An Executive Managing Director of Weeden & Co., L.P. is a member of The Leuthold Group, LLC board of directors. Weeden & Co., L.P. member FINRA, NASDAQ, and SIPC.

© Leuthold Weeden Capital Management