ING Fixed Income Perspectives March 2013

Bond Market Outlook

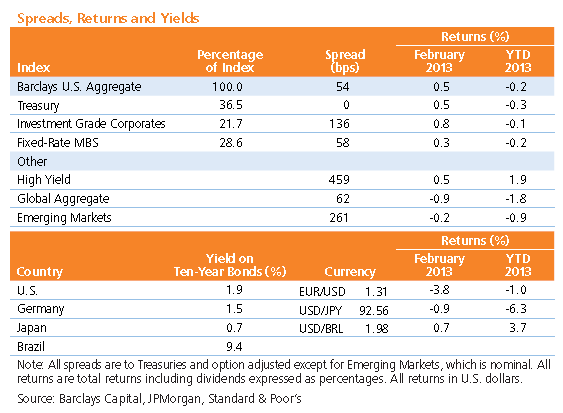

Global Interest Rates: Developed sovereigns are still broadly unattractive, but global central banks appear poised to ease.

Global Currencies: We prefer EM currencies that will continue to benefit from positive global growth and tolerate further upward pressure on the U.S. dollar.

Corporates: We are neutral on corporates, as profit growth is decelerating and debt is rising faster than cash flow.

High Yield: Spreads continue to compensate for default risk, though record all-in yields and high dollar prices limit upside.

Mortgages: Uncertainty surrounding the Fed’s exit strategy is a concern, but Bernanke continues to back bond-buying programs supportive of mortgages.

Emerging Markets: We remain positive on EMD, particularly in local currencies, despite recent spread widening and U.S. dollar strength.

Macro Overview

- Sequestration seemed like a no-brainer back in 2011: Establish automatic fiscal consequences so severe that even a bitterly divided Congress would have no choice but to come together in support of a less prickly path to deficit reduction before the cuts were triggered in 2013. But we’re familiar with what happens to the best laid schemes of mice and men; in the case of sequestration, things went awry on March 1 as partisanship trumped compromise. While the $85 billion of cuts slated for 2013 are expected to create fiscal drag of around 0.5%, it’s important to recognize sequestration for what it is: a reduction of incremental government spending, not an outright purge. Apparently, the time has come for Uncle Sam to join the rest of the population in doing more with less.

- While forced deleveraging is not the most elegant way to tackle our fiscal issues, sequestration does not spell curtains for the U.S. economy. With strong payroll numbers, steady wage growth, a continuously improving housing market and a renewal in M&A activity, there appears to be enough gas in the private sector’s tank to keep the economy rolling, especially given the Fed’s plan to keep interest rates low and the quantitative elixirs flowing.

- Belt-tightening also appears to be the strategy for the rest of the developed world, particularly our European brethren. The political stalemate in Italy is evidence that Monti’s austerity plan, while effective in stabilizing the economy, has been far from magnifico in the eyes of the voting public that bear its brunt. But the ECB — like the Fed, the Bank of Japan and the Bank of England — stands at the ready to do whatever is necessary to keep the region moving forward, even as deleveraging and political risks at times threaten to derail domestic and global economic momentum.

- As equities and other risky assets continue to climb northward, our outlook for global fixed income in 2013 remains the same: Don’t fight the central banks, but be wary of the risks. Valuations have richened, the margin for error has narrowed, and suboptimal political outcomes will induce bouts of heightened volatility. Active asset allocation coupled with prudent security selection and diversification across countries, sectors and currencies is a wise plan in this environment.

Sector Overviews

Global Interest Rates

- While Italy’s election results cheapened valuations and increased uncertainty, they did not change the country’s creditworthiness. While an anti-austerity victory in the next round of elections may unwind some of Monti’s reforms, we believe the ECB can contain sovereign credit risks regardless of periodic political turmoil. We tactically favor peripherals in general and Italy specifically.

- Developed sovereigns are still broadly unattractive, particularly in the U.S. given expectations of an eventual unwinding of quantitative easing and tightening of monetary policy. However, global central banks appear poised to ease as growth expectations slow. We maintain our negative view on developed market rates but expect supportive central banks in the near term. We continue to favor emerging market interest rate risk.

Global Currencies

- We maintain our strategic bias in favor of emerging market currencies. Given the recent strength of the U.S. dollar and a weakening yen and pound sterling, we prefer emerging currencies — such as the Brazilian real, Mexican peso, Philippine peso and Malaysian ringgit — that will benefit from global growth and can tolerate additional upward pressure on the U.S. dollar.

- Within developed markets, we have moved to neutral on the U.S. dollar but remain bearish on the Japanese yen and British pound. We favor Scandinavian currencies like the Norwegian krone and Swedish krona that offer higher yields and will continue to benefit from positive global growth.

Investment Grade Corporates

- Performance for investment grade credit was flat in February, and inflows into the asset class continue to be relatively healthy. We are maintaining our neutral outlook, however, based upon our concern that corporations — with credit spreads tight and macro uncertainties easing — will increasingly succumb to shareholder pressures to increase balance sheet leverage.

- Historically, rising volumes of stock buybacks, dividends and M&A activity have not been overly destructive to corporate fundamentals, as improved economic conditions have led to offsetting improvements in cash flow from higher earnings. However, profit growth is currently decelerating and debt is rising faster than cash flow; meanwhile, shareholder-friendly actions have already begun to negatively impact issuers within the energy, technology, communications and consumer non-cyclical industries. Financials and utilities offer investors a relative safe haven and have outperformed year to date.

High Yield Corporates

- High yield moved sideways in February as equity market volatility increased on macro concerns. Macro risks like political dysfunction in Italy and the U.S. are by no means unknown to market participants; the extent to which investors worry about them determines the action in high yield spreads

- As the severity of known macro risks continues to oscillate, credit quality appears to be trending down. However, while the destructive potential of rising leverage and weakening revenues and earnings are a concern, fundamentals remain solid and spreads continue to offer attractive compensation for default risk in the longer term. Record all-in yields and high dollar prices limit upside from current levels, though.

Mortgages

- Prepay expectations remain elevated, but the supply/demand picture remains favorable for agency RMBS, as the Fed continues to purchase $40 billion per month in addition to $25–35 billion as part of its “Reinvestment of Paydowns” program. Though Bernanke remains dovish, the lingering uncertainty surrounding the Fed’s exit strategy has become the chief risk for agency RMBS and will cause volatility from time to time.

- While regulatory clarity is still a concern for non-agency RMBS, its outlook continues to benefit from the housing market. CMBS underperformed in February, driven primarily by valuation concerns; going forward, there will be a premium on security selection as losses begin to materialize and valuations disperse. An easing of the new-issue pipeline should help stabilize spreads, and our outlook for CMBS remains positive.

Emerging Markets

- Hard-currency emerging market sovereigns, particularly higher-yielding names, sold off during February. Rising risk aversion led to U.S. dollar strength and emerging currency weakness, though interest rates remained stable. We expect emerging local markets to outperform external markets in 2013 thanks to more attractive yield opportunities and stronger economic growth.

- We remain cautiously optimistic on emerging corporate debt despite challenging valuations. Emerging high yield corporates have performed well this year, and new-issue supply has begun to stabilize after reaching a record high in January. Fundamentals are deteriorating in the face of slowing global growth, however, as cash balances are expected to decline and leverage is steadily increasing.

ING U.S. Investment Management’s fixed income strategies cover a broad range of maturities, sectors and instruments, giving investors wide latitude to create a new portfolio structure or complement an existing one. We offer investment strategies across the yield curve and credit spectrum, as well as in specialized disciplines that focus on individual market sectors. We build portfolios one bond at a time, with a critical review of each security by experienced fixed income managers. As of December 31, 2012, ING U.S. Investment Management managed $127 billion in fixed income strategies in the United States.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 6003