During a recent interview on February, 27th on CNBC Warren Buffett described a phone call he got from the late Apple CEO Steve Jobs. Mr. Buffett gave this account , "It was an interesting conversation because I hadn't talked to him in a long time. He said, 'We've got all this cash. What should we do with it?' So we went over the alternatives. It was kind of interesting." Mr. Buffett often comments in his annual letters about the options for deploying cash and he did again in this interview. He stated there are only four things a company can do with its cash: stocks buybacks, dividends, acquisitions, or "sitting with it."

Mr. Buffett went on to describe the phone call with Jobs on the subject of Apple’s cash hoard: "I went through the logic of each thing. He told me they would not have the chance to make big acquisitions that would require lots of money… And then I asked him the question, I said … 'I would use it for buybacks if I thought my stock was undervalued.' And I said, 'How do you feel about that?' The stock was 200 and something. He said, 'I think my stock is very undervalued.' I said, 'Well, what better to do with your money?' And then we talked awhile. And, he didn't do anything, and of course, he didn't want to do anything. He just liked having the cash. It was very interesting to me because I later learned that he said I agreed with him to do nothing with the cash. He didn't want to repurchase stock although he absolutely felt his stock was significantly underpriced at two-hundred and whatever it was then."

As an interesting interaction between two iconic CEOs, this conversation has many fascinating components that could be analyzed, such as the personality dynamic between a billionaire from the “Greatest Generation” and a billionaire from the “Baby Boom Generation” or the relationship between a value investor who relies on quantitative measures and a tech guru who relies on an Eastern style intuition. However, being value based investors ourselves and also Apple Inc. investors we are concerned with analyzing the practical advice Mr. Buffet gave to Mr. Jobs.

The timing of this conversation was probably sometime in 2010, given Mr. Buffett’s mention of the stock price in the $200s. The stock has roughly doubled since then but Apple’s cash and marketable securities position has also increased by $70 billion since FY 2010, which is also almost double. The amount of liquidity Apple has on its Balance Sheet has grown with its stock price from FY 2010 to FY 2012. So, we now have a company with over $400 billion in market cap and no debt and it still has the same liquidity as when it was half its size. Going back to Mr. Buffett’s stated options for a company with excess capital -- “ stocks buybacks, dividends, acquisitions, or ‘sitting with it’ ” -- the choices can become limited by the size of the entity.

Apple is often said to be hampered now by the “rule of large numbers.” This idea suggests that as already one of the largest companies in the history of Earth, Apple cannot do anything to meaningfully increase its business in percentage terms. This proposition seems to be true when looking at strategic acquisitions for Apple. Could making a large acquisition in the $30- $40 billion range meaningfully increase Apple’s Operating Income and Earnings per Share? Perhaps, but in the technology world this increase is even more of a challenge than in other industries due to the amount of intellectual property and the small size of most of the companies in the sector.

Another Buffett option for Apple’s excess capital “is sitting with it.” This is always a viable option that aims to protect the Balance Sheet. Mr. Buffett describes it in his 2011 Shareholder letter as his primary tenet when examining conditions for share repurchases, “ first, a company has ample funds to take care of the operational and liquidity needs of its business. ” Looking at Apple’s Balance Sheet from its Q1 2013 it is clear they have a glut of liquidity. Apple has Total Assets of $196 billion of which only $15 billion is Property Plants and Equipment (Net) and $137 billion is Cash or Marketable Securities. Apple’s Balance Sheet carries almost 70% of its Total Assets as cash-like instruments. Apple has ample cash to run and reinvest in its business and still be awash in a sea of excess capital.

Dividends are always a practical option for any company and should be considered in conjunction with all other options. Indeed, Apple has recently instituted a quarterly dividend with a healthy yield that is currently above the 2.30% for the S&P 500 Index. Apple may also consider a special dividend to payout a large portion of its cash to shareholders. Again, this is a reasonable approach but it ignores the advice from Mr. Buffett to Mr. Jobs. The advice is explained further in Mr. Buffett’s 2012 annual letter, “ repurchases – is sensible for a company when its shares sell at a meaningful discount to conservatively calculated intrinsic value. Indeed, disciplined repurchases are the surest way to use funds intelligently: It’s hard to go wrong when you’re buying dollar bills for 80¢ or less. ” This dictum is even truer in today’s ultra-low interest rate environment where investors are starved for yield and return.

So what about Mr. Buffet’s last option: share repurchases? Is Apple’s stock cheap enough for the company to repurchase it in the open market if we follow the Buffett-Munger share repurchase guidelines for Berkshire Hathaway? Mr. Buffett often discusses his and Charlie Munger’s criteria for share repurchases in his annual reports. The first rule of ample funds has already been analyzed. The second criterion from his 2011 letter is that the stock should be selling in the market at a material discount to a conservative estimation of the company’s intrinsic business value. “Intrinsic Value” is the classic Buffett-Munger metric and it is more subjective and can be very different from Book Value. Intrinsic Value tries to capture the worth of the business to its owners and is not simply an accounting of Assets and Liabilities. It is elementary to conclude that a business owner is most concerned with the operating income and earnings of the enterprise. For Berkshire Hathaway both Mr. Buffett and Mr. Munger list “three key pillars” to measuring intrinsic value to see if their stock is cheap enough to repurchase.

They are the value of the investments, the value of non-insurance earnings, and the more subjective measure of how the company will deploy retained earnings. When discussing Apple the first measure is not relevant since Apple’s investment portfolio is mostly a proxy for cash. Looking at the third pillar we will rely on Apple’s market position, brand, and past innovations to examine how they will deploy retained earnings. It appears that Apple has more than enough retained earnings to continue with its organic innovations.

It is the Buffett-Munger second metric of intrinsic value that is most quantitative and relevant for Apple and its shareholders. As shareholders and business owners of Apple we look at our share of its profits using basic valuations for a guide to company share repurchases.

We will estimate Mr. Buffett’s conservative intrinsic value by using a conservative estimate of profits: Cash from Operations. This metric largely discounts subjective accounting items and shows what the company’s checking account looked like after a year of business operations and not one-time charges. To estimate the equity owners’ future share of Cash from Operations we are going to use a basic present value of money model. This model will estimate the future Cash from Operations by looking at the different revenues numbers we input and take the past 5 year average of Cash from Operations/Revenues which is about 28%. This operating margin is expected to be under pressure but our value is 7% lower than the FY 2012 margin. Also, Apple expenses much of its R&D when it could be capitalized on the Balance Sheet over many years. This expensing of R&D has a direct impact on margin. We then discount the Cash from Ops for different implied revenue growth to arrive at a net present value for 5 years operations. Year 5 is then used as the terminal value. That terminal value is given a 5 times multiple which is close to the multiple that Dell is being acquired for by private equity investors. Apple with its innovation and R&D should trade at higher multiple than a company like Dell which looks more of a manufacturing company selling a commoditized product. That Terminal present value is added to our 5 years of Cash from Ops. This should get us to a number that we could conservatively expect as the cash we would be entitled to as Apple’s owners for 10 years. We will then add the present value of the calculated Cash from Operations to cash and marketable securities currently on Apple’s Balance Sheet to arrive at an equity value. Of course, any model is only as good as its inputs.

The other major input in the model is the Weighted Average Cost of Capital. This will be held at 4% which is the level Mr. Einhorn has recently suggested that Apple preferred shares would easily yield and it is over 60 bps higher than the current 10 year JPM Investment Grade Credit Index yield. Apple with its fortress Balance Sheet and current free cash flows could almost assuredly fund lower than the index rate but we are maintaining the Buffett-Munger conservative mantra. In academics much higher WACCs are used but in today’s market, to model any yield higher quickly goes from conservative to ridiculous.

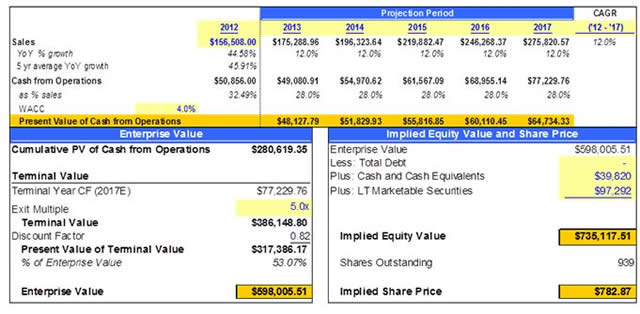

The cautioning of “garbage in; garbage out” is extremely important in models that use compounding and time value of money calculations. To be consistent with the conservative intrinsic value we will use conservative inputs for our model and heed Mr. Buffett’s warning on share repurchases from his 2011 letter, “what is smart at one price is dumb at another.” The argument has been made that Apple is a mature and large company that is on its way to selling a commoditized product like IBM or Microsoft. As value investors we are not aiming to look into our crystal ball and predict incremental sales growth changes so we will start by simply plugging in an IBM like sales growth of 2% per year to our model. Below is a table of Apple’s projected Cash from Ops with IBM like sales growth for 5 years.

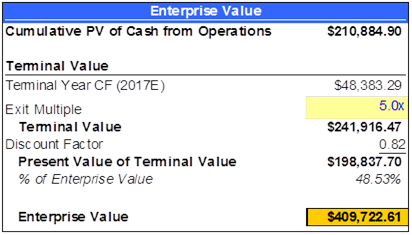

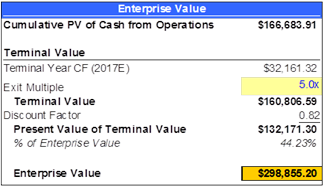

Below we have the present value of our 5 years of operations plus a terminal value of that cash to arrive at an Enterprise Value. This is only based on the cash from the company’s operations and not investments that the company holds. $409 billion is an enormous amount of cash to kick off but let’s not forget what makes the majority of Apple’s Balance Sheet; cash and cash like instruments.

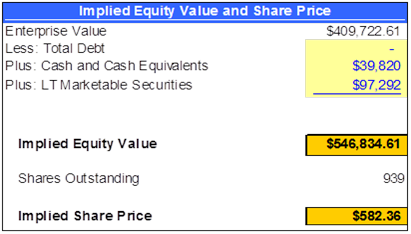

In the next table, we have added our 2% forecast-growth Enterprise Value to Apple’s Cash and Long Term marketable Securities. We then take that Implied Equity Value and divide it by the shares outstanding to arrive at a share price of $582.

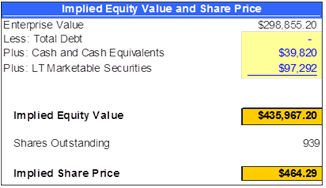

With 2% growth, our intrinsic value is about 25% higher than the current share price. These numbers meet Mr. Buffett’s target for investing and as he states it is like “ buying dollar bills for 80¢ or less.” Investing in Apple at the current share price of $464 with an intrinsic value 25% higher would also fit the description for a great investment that Mr. Buffett attributes to one of Berkshire’s Directors, “it’s like shooting fish in a barrel, after the barrel has been drained and the fish have quit flopping.”

We do want to be confident in our investment and to appease the “Apple is all done” crowd we ran this model with 0% sales growth.

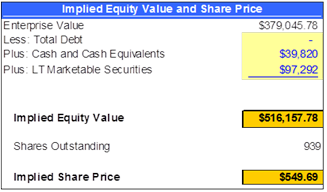

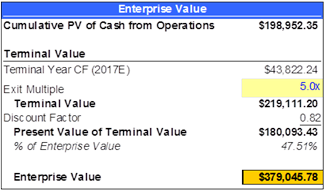

We still get an intrinsic value far above Apple’s current price and 100 day moving price average in the $504 range. This 0% growth forecast of $550 intrinsic value still is over 18.5% higher than where Apple shares currently trade. As value investors this is the case were we are most attracted. When we examine only historical cash generation we see a great and profitable business. When we look at that with current valuations we see an attractive investment without the need to peer into a crystal ball to guess at future sales growth rates. We would be very happy under this scenario if Apple simply maintained its profitability.

In homage to Charlie Munger we must as the Algebraist Jacobi said, “Invert, always invert.” After all, we are not buying a sales growth rate. Rather, we buy shares at a dollar price. So, to invert, we looked to our model to answer what is the implied sales growth at the current stock price? Wait: do not answer because there is no answer. Or in the words of famed investor and professional wrestler Rowdy Roddy Piper, “Just when they think they know the answers, I change the questions!” What is the forecast year over year sales declines for Apple at the current stock price?

There are a few ways to arrive at the current share price of $464 but the simplest is to use a 6% year over year decline in sales for every year for the next 5 years. Two key pillars to our investment thesis are to look for profitable businesses that are undervalued. To quote Charlie Munger, “I would rather buy a great company at a fair price than a fair company at a good price” means we should always think of profitability and value as two sides of the same coin. Apple has been a well-run and extremely profitable company for many years and its stock is now trading at a great price according to our work. We are very comfortable buying into this business if our test for a profitable investment is if Apple achieves higher sales rates than declines of -6% year over year.

Mr. Buffett was a student of famed investor and teacher Ben Graham. Graham looked for deep value in the Balance Sheets of companies. This is how Mr. Buffett was trained to look at the world but great values are not only visible on the Balance Sheet. Buffett’s current practice of looking at valuation combined with a good business is something that he credits to Charlie Munger. For the last 10 years, Apple has been the kind of profitable company Mr. Munger covets. The rest of the financial statement, the Income Statement and the Statement of Cash Flows shed light on the profitability of the business operations. Apple has had great success there but there is now an ironic downside to that success. Apple has been so profitable that the fruits of that profitability; the retained earnings sitting offshore and domestically are now the subject of much consternation to many shareholders. Despite this concern, the past operational performance gives us the confidence that Apple sales will not begin shrinking to the tune of 6% a year going forward when they have grown sales at an average 40% a year for the last 10 years.

When running this same model for Apple’s recent growth rates we get some drastic numbers and we agree that Year over Year Sales Growth is coming down from the recent Himalayan 45%. Those sales growth rates are how we got the flurry of 4 figure stock price targets last autumn.

The analyst consensus for Apple’s sales growth is closer to 12% and below are our numbers run with those increases. We should note that the analyst community is notoriously fickle and 12% can become 20% as fast as it can become 2%. The good news for the value investor is that we do not have to concern ourselves with incremental basis points of sales growth to see Apple’s stock as being below intrinsic value. A steady Apple is a very profitable Apple.

Looking again at valuation and Warren Buffett it is worth discussing Apple’s Price to Book Ratio. Mr. Buffett has recently stated that he will not pay more than 1.20 times book value for Berkshire’s shares. So, with Apple having a Price to Book Ratio of close to 3 how can we say that Buffett and Munger would approve of share repurchases? The answer is that a technology company such as Apple and an industrial and financial conglomerate like Berkshire Hathaway are very different businesses that use their Balance Sheets in very different ways. Industries that require more infrastructure and assets on the ground usually trade at lower price to book values because the replacement cost of these assets is integral in their business. When examining Apple’s Balance Sheet it can be seen that to profitably run its business, Apple conservatively needs only $50 billion in capital consisting of cash, short term investments, inventories, PP&E net, and a few extra billion for loose change. Apple’s current 25% return on assets is a return mostly on cash and investments Apple does not need to run its operations. The real ROA on needed assets is drastically higher than the stated figure and not far below 100%. Also, a company such as Apple does not reflect what could be its greatest asset on its Balance Sheet. That asset would be its competitive or economic moat. Apple’s brand name, intellectually property, market position, pricing power and customer loyalty are all money making assets that are not reflected accurately on its Balance Sheet. These stealthy intangible assets show their worth on the Income Statement. Looking at Apple’s assets on the Balance Sheet it could be said that the hard assets needed for business operations are overstated and the stealthy and profitable intangible assets are far understated. This gives us confidence when buying in at Apple’s current book value.

Of the four things Mr. Buffett suggests companies can do with excess cash we clearly favor one. It even looks as if there are 4.5 things to do with the cash if we listen to David Einhorn. He has presented a unique and intelligent idea with his iPreferred concept but for two reasons we favor share repurchase over iPreffereds. First, the iPreferred sounds and feels too much like 2006 financial engineering. We are still feeling the hangover from over engineered credit instruments. Second, we feel that Occam’s Razor is an appropriate guide. The simpler of two ideas is usually the better. Following that thinking, in 1977 a new computer company adopted the motto, “Simplicity is the ultimate sophistication.”

In conclusion, let us put ourselves in good company and echo Warren Buffett’s advice to Steve Jobs by urging Apple Inc. to use a material amount of its sea of cash to repurchase their stock. We favor the simple sophistication of the Buffett-Munger approach for Apple’s corporate share repurchase. In an odd reality, the size of Apple means there is no company that can be acquired to meaningfully help Apple shareholders, save one; Apple. Additionally, in our current low return world any return close to what the intrinsic value forecasts show would be welcome. For all of these reasons Apple Inc., its CEO, and Board should adopt a plan to deploy a large amount of the excess cash the company holds to repurchase its shares on the open market as soon as possible. In our opinion, the tax consequences of repatriating any income for that purpose pale in comparison to the upside opportunity of repurchases. As always, Mr. Market may remove this windfall opportunity in Apple stock as investors regain their composure over its business and raise the stock price closer to our intrinsic value. What is not opinion but fact is that repurchases will increase the ownership percentage of the equity holders who do not sell and they will own a greater share of the future corporate profits. Even with a 0% growth rate Apple looks more like an ATM than a computer company. We see Apple as trading well below intrinsic value or to use another of Warren Buffett’s expressions; Apple is a few hundred billion dollar bills that are trading for less than 80 cents.

Please note that Mr. Bonner and Carne Capital own Apple Inc. shares in the client accounts they manage.

Mr. Sean Bonner is the Chief Investment Officer at Carne Capital and the Carne Large Cap Value Fund Portfolio Manager.

Mr. William Bonner is a senior at St. Joseph’s University in the Honors Finance Program.

© Carne Capital