S&P Reaches record High

The first quarter closed out in positive fashion, as the S&P 500 eclipsed its high watermark of 1565 on the final day of March. The S&P’s previous high was set in October 2007, underscoring the depth of the market’s drawdown in the 2008-2009 period. The index needed a gain of 129% from its March 2009 low of 638 to recapture its peak level.

The first quarter ended as one of the strongest in years, as the S&P 500 gained 10.6% and the Dow Jones Industrial Average increased 11.9%. It was the biggest first quarter gain since 1998 for the Dow.

Interestingly, market performance in the US was led by more traditionally defensive sectors in the first quarter. Within the S&P 500, healthcare (+15.8%), consumer staples (+14.6%), and utilities (+13.0%) posted the strongest returns of any market segment. This may have been partially driven by the higher yield characteristics of those stocks. Cyclical sectors including materials (+4.8%) and technology (+4.6%) were the market laggards.

In the holiday-shortened week, economic data was generally positive.

On Tuesday, the Census Bureau reported durable goods increased 5.7% in February, well above consensus estimates. The series rebounded from a disappointing January when orders contracted 3.8%. Month-to-month volatility was driven by the index’s transportation component, as the sub-index jumped 21.7% in February following a 17.8% decline. Nondefense aircraft and parts, driven primarily by orders for Boeing products, has generated much of the sharp swings in the dataset.

Despite the volatility, durable goods orders have expanded in five of the past six months. Core levels were more disappointing in February, however, as the series posted a modest contraction of 0.5%. Core new orders have averaged 1.3% over the past six months though, underscoring the general uptrend in the US manufacturing sector.

Home prices rose at the fastest rate since 2007, according to Case-Shiller data released on Tuesday. Based on year-over-year data, the 20-city index rose 8.1% in January, with positive increases seen in every city. Housing prices also defied typical seasonal weakness in January, increasing 0.1% on a non-seasonally adjusted basis. Following seasonal adjustment, January’s monthly gain translated to a 1% increase.

Housing prices continue to be supported by low inventories and historically low mortgage rates. Existing home sales data indicated that the nation’s existing home stock stood at 4.3 months in January, the lowest rate seen since 2005. Likewise, new home sales data last week indicated supply remains constrained at 4.4 months. This low inventory has been a headwind for new home sales, which dipped to a rate of 411,000 in February, but prices remain firm. New home prices increased 3.0% in the February report.

The final estimate of fourth quarter GDP was released on Thursday. As expected, the series was revised higher, although slightly less than expected, to a seasonally adjusted annual rate of 0.4%. The preliminary reading in late January indicated the US economy contracted by 0.1%. The Bureau of Economic Analysis indicated that the increase was due to upward revisions of nonresidential fixed investment and to exports; these gains were partially offset by a downward revision to personal consumption expenditures.

A raft of consumer data released last week indicated the consumer remains fairly healthy, in spite of the reinstatement of the payroll tax and the automatic spending cuts known as sequestration.

Personal incomes grew 1.1% in February, well above the expected 0.9% rate. Consumer spending also surpassed expectations, expanding by 0.7% in the month.

Incomes rebounded from a sharp period of volatility in December-January. Incomes spiked in December due to employers accelerating dividends and bonuses ahead of an anticipated tax rate change in 2013. This pulled forward much of the seasonal activity in January, causing a deep month-over-month plunge in incomes. February’s 1.1% increase may indicate a normalization of the data.

Spending, on the other hand, has not been impacted by the volatility in income. It increased for the fourth straight month in February, although the data was partially skewed by sharply increasing gasoline prices. A measure of real spending, which deflates the results for inflation, came in at 0.3%.

Finally, consumer attitudes appear mixed, as the consumer confidence and consumer sentiment surveys indicated diverging results last week. While the Conference Board’s consumer confidence measure fell eight points to 59.7 in March, the University of Michigan sentiment report indicated consumers were much more optimistic in the month. The sentiment index finished the month at 78.6. Weakness in the Conference Board report appears to be at odds with “hard” data such as retail sales and personal spending, but it may be more a result of future outlooks than current conditions. Both reports report softness in expectations, illustrating continuing uncertainty as a result of new policy measures out of Washington.

Is The Vix Still An Adequate Measure of Risk?

The 30-day implied volatility index for the S&P 500 calculated by the Chicago Board of Options Exchange (CBOE), known as VIX, has long been used as an indicator of market sentiment. Commonly referred to as the “fear index,” the VIX often portends periods of stress in equity markets, as options traders price in higher volatility in the future. The shape of the VIX futures curve, in particular, has historically been used as an indicator of future volatility levels.

More recently, however, one can question the effectiveness of the VIX as a measure of future volatility. That is because of a wave of new investors in the volatility space, potentially causing new artificial pressures on the measure.

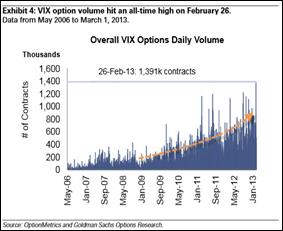

The number of options trading on the VIX has reached record levels in 2013. According to the Wall Street Journal, the number of call options on the VIX reached 7.7 million in early March. This is 19% above the prior record set in January, and 83% above the levels seen in March 2012. The daily volume of VIX options has risen sharply to 1.4 million contracts, a record high. For comparison, in 2007 the daily average volume was 92,000 contracts – less than 15x that seen today!

Source: Goldman Sachs

The reasons for the surge in interest in the volatility markets are multi-fold. Observers generally point to the devastating capital losses of 2008 as the primary culprit. Many institutions, in particular, are paying for so-called “tail-risk protection,” protecting the value of their traditional assets with equity and volatility options. This constant presence in the market has increased the influence of a relationship not unlike the traditional hedger-speculator relationship in commodity futures markets: the hedger, in this case the institution, is willing to pay an “insurance” premium to the speculator to protect the price of an underlying asset.

The result of this phenomena is not a persistently high VIX index level, which measures implied volatility over a shorter time frame. Indeed, the VIX has fallen to post-crisis lows and has been entrenched at those levels for months. Instead, the structural shift in institutional behavior is apparent in the term structure of the VIX. The futures curve of VIX contracts continues to trade very steeply, as the protection premium paid by institutions has been priced into longer-dated options. This in itself has made the VIX futures curve less useful in predicting future volatility, as the long end of the curve may be unduly influenced by irrational pricing behavior.

Source: Goldman Sachs

Pressure on the front end of the VIX futures curve may be due to another source: namely, investors’ thirst for yield in a low-yield environment. Many investors are increasingly interested in the yield, or premium, that can be derived from selling options on underlying equities or the VIX contract itself. While being short volatility can be extremely risky, investors have been increasingly flocking to these types of strategies to pick up additional sources of income. Option writing strategies tend to focus on front month options, which may be putting excessive downward pressure on the front part of the curve. In other words, rising demand for selling volatility may be suppressing volatility and indicators like VIX that measure it.

The availability of many new exchange traded products (ETPs) has exacerbated these effects. These instruments sell near-term contracts and buy later dated contracts as the near term options expire, steepening the VIX futures curve. They have also facilitated the entry of retail investors into the space, despite studies such as Deng, McCann, & Wang (2012) that discredit these products’ ability to hedge stock portfolios (primarily because of negative roll yield associated with the contangoed volatility futures markets). Nevertheless, volume in these products has exploded, with assets of more than $3.1bn in 34 different ETPs, according to the CBOE. As average daily trading volumes of these products increase, pundits and traders alike question the influence these new instruments are having on volatility markets.

Investors should remain aware of these new developments in volatility markets when looking to the VIX as a market indicator. While the VIX will continue to be a coincident indicator of a market drawdown, the underlying drivers of the VIX futures curve have become muddied. The VIX futures curve may no longer be as useful in predicting volatility as it is in reflecting underlying supply/demand dynamics from a broad new range of market participants.

The Week Ahead

Several important economic indicators are slated for release this week, headlined by the Employment Situation report on Friday. Economists expect the US economy added 193,000 jobs in March and that the unemployment rate will remain unchanged at 7.7%.

Other important reports include the twin releases from the Institute of Supply Management (ISM). The manufacturing index is due out on Monday, while the non-manufacturing index is released on Wednesday.

Several important central banks meet this week, including the Bank of Japan, Bank of England, and the European Central Bank. Russia, Turkey, and Thailand also provide updated policy guidance.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

For more information, please visit our website at http://www.Fortigent.com.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent