F.I.R.S.T.: Made in the U.S.A.

Not just the preamble for the “machine-wash-in-cold-water-and-eat-celery-only” instructions on the inside of your skinny jeans, “Made in the U.S.A.” is a brand in vogue these days as the Stars and Stripes looks to dawn a manufacturing renaissance to go with that snazzy new housing recovery everyone’s been talking about. Just watch a Chrysler commercial on YouTube for a glimpse of the new American couture. Clint Eastwood’s Dirty Harry and “Imported from Detroit” — the auto giant turned underdog’s bold and defiant attempts post-2008 to turn a U.S. auto-manufacturing swan song into a power ballad, reviving a little of that Motown swagger for America’s quintessential car-producing capitol by proclaiming to the world that good-old-fashioned auto manufacturing is coming back to Detroit . Make our day, China!

Turn down the hyperbole and there are underlying notes of truth in Chrysler’s claim that “Made in the U.S.A.” is back in style. Thanks to a post-concession United Auto Workers union and pent-up demand for more fuel-efficient vehicles in a cheap-credit environment, the cost structure in the United States has become more competitive with the nonunion plants of foreign automakers. This new competitiveness is supporting the domestic expansion of companies such as Ford and even the “re-shoring” of auto manufacturing from lower-cost countries such as China and Mexico.

The appeal of “Made in the U.S.A.” is not just limited to automobile production. In a growth revival the likes of which have not been witnessed since the 1990s, U.S. manufacturing has added more than 500,000 jobs since the beginning of 2010, driven primarily by a narrowing U.S. labor-cost gap with countries such as China, where wages have risen sharply, and by technological advances in natural gas production that have made the U.S. more competitive in the global energy marketplace. An important contributor to GDP, the U.S. manufacturing sector is still the largest in the world and supportive of broader employment given its strong linkage to other sectors of the economy along the proverbial assembly line.

We discussed in last month’s F.I.R.S.T. the positive ramifications of “animal spirits” in this low-interest-rate environment: forcing dormant, defensive liquidity toward more offensive, efficient ends. With the U.S. housing market in a healing phase and the spark of animal spirits ready to revive business spending and capitalize new ideas, perhaps a revival of U.S. manufacturing and the demand for goods made in and imported from the U.S. will be the engine of growth needed to assure that a strengthening U.S. economy isn’t just a fleeting fashionable fad but a long-term style staple.

A U.S. manufacturing renaissance has a nice ring to it, but before we buy into the hype and hitch America’s fate to the “Made in the U.S.A.” bandwagon, consider two overwhelming facts about our economy:

- The cost of American labor is still much higher than that of emerging market producers of globally traded goods.

- The bulk of U.S. economic output comes from services, not manufacturing.

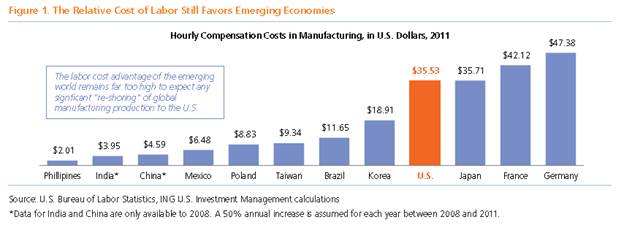

Comparisons of global labor costs can be tricky, but statisticians in Washington do as good a job as any of measuring the international competitiveness of American workers — at least they did before sequestration cut their funding1. Figure 1 shows a selected comparison of the hourly cost per manufacturing worker in the U.S. The average U.S. factory worker earns nearly $36 per hour, which includes wages, bonuses and benefits. That is two to three times more expensive than a Korean or Brazilian factory worker and nine times more expensive than a Chinese worker.

The Conference Board estimates that two-thirds of the labor-cost gap relative to China can be attributed to a more productive U.S. worker. Though U.S. productivity has been on the rise, it is unlikely that the average American worker is nine times more productive than the average Chinese worker, so there is still an enormous cost advantage to producing goods in the emerging world. While U.S. labor costs are more competitive on the margin, largely due to lower U.S. wage growth and the cheapness of the U.S. dollar, we think the long-term labor-cost gap is simply too large to expect a major relocation of global manufacturing to the U.S. Sorry, Clint.

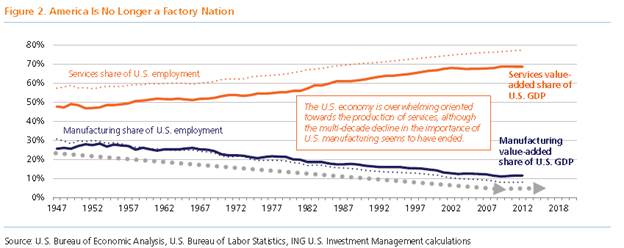

Because even if labor-cost differentials continue to narrow in favor of the U.S. and further incentivize companies in cost-sensitive sectors such as autos to increase their U.S. production and build new plants, a manufacturing-led revival in U.S. growth would still be difficult to achieve, as it would be cutting against the grain of nearly a half-century of off-shoring momentum and structural change in the U.S. economy. Figure 2 shows the shares of U.S. economic activity and employment in manufacturing and services sectors since World War II. The trends are obvious. Services, which span a wide range from hairstyling to software design, are now responsible for around 70% of U.S. economic output and jobs, up from 50% in the 1950s and 1960s. U.S. manufacturing has been in decline until recently and now represents around 10% of output and jobs.

The good news is that the structural decline in the relevance of manufacturing has stopped, which is exactly what you would want to see as a sign of improving competitiveness. The bad news is that even strong growth in manufacturing activity cannot create as many jobs or as much output as it once did.

So how does the “Made in the U.S.A.” brand capitalize on its renewed cachet in this still highly globalized economy? The same way we always have — through innovation and ingenuity. The U.S. continues to rank among the world’s leaders in the creation and development of new technologies and products, as measured by indicators such as research and development (R&D) spending and patent/trademark applications2. It is on this platform where the U.S. can strut. America’s true growth advantage over the rest of the world is its manufacturing leadership in software, information services, telecommunications, finance, entertainment and many other service industries that create long-term value and wealth.

Capital spending focused on innovation can lead to higher labor productivity growth in these areas and therefore higher long-term growth potential for the economy. Figure 3 below illustrates this relationship since the 1990s. During this period, when the United States was investing more in capital equipment than in housing, labor productivity subsequently surged. The opposite happened in mid-2000s when our myopic focus on housing and consumption resulted in a sharp decline in productivity growth that preceded the crash of the housing bubble. This relationship has flipped back, with capital spending now potentially leading the way to higher U.S. productivity growth. How much higher depends on where the next great and groundbreaking innovations come from. For example, there is evidence that significant productivity gains can come from the use of new technologies in older industries. A 2011 study by the McKinsey Global Institute concluded that the use of large-scale data management on global manufacturing supply chains can boost manufacturing profit margins by two to three percentage points, while the application of so-called “big data” analytics can reduce R&D and product development costs by 20–50%3. Thus, investing in R&D now potentially can lower the cost of R&D in the future! In our view, this sort of forward-looking innovation is what the country needs to get back to more balanced growth and sustainable wealth creation.

The recent upturn in U.S. manufacturing is a stylish accoutrement adorning the larger U.S. growth trend. But to spark a renaissance that truly impacts the long-term U.S. economic growth picture will require not only that we refine “Made in the U.S.A.” classics like autos, but define new ideas, products and services that are unavailable anywhere else. In short, we need a little more Chrysler and a lot more Google.

1 As a result of the spending cuts enacted by the U.S. government sequester, the Bureau of Labor Statistics has been forced to stop measuring global labor costs. The ongoing U.S. fiscal retrenchment is the main reason why cutting U.S. corporate taxes — among the highest in the world — is not currently a viable solution to boost investment and productivity.

2 According to the OECD, nearly 40% of U.S trademark applications are in service-related industries, while only 10% of China’s trademarks are in services, showing that China remains heavily focused on moving up the manufacturing value-added chain while continuing to “borrow” services and ideas from the rest of the world.

3 “Big data: The next frontier for innovation, competition, and productivity”, McKinsey Global Institute, May 2011.

This commentary has been prepared by ING Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors. Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 6071