Surprise! 2013 Rally Pales in Comparison to 2012 “Stealth” Rally

Executive Summary

- Despite the hoopla over first quarter market performance, it paled in comparison to the first three months of 2012.

- Driven in part by an extremely accommodative Fed, the U.S. economy is gaining traction, but Europe continues to flounder.

- After their first negative print in three years during the third quarter, S&P 500 companies returned to positive earnings growth in the fourth.

- A broad, globally diversified portfolio is the best way to balance the desire for wealth accumulation with an appreciation of volatility.

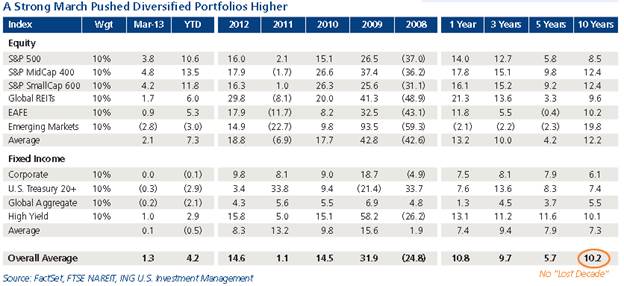

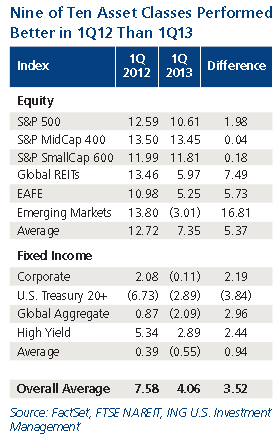

Despite all the hoopla over market performance in the first quarter, the period actually represented a marked disappointment compared to the first three months of 2012. While an equal-weighted global portfolio of ten asset classes returned a respectable 4.2% in first quarter 2013, that figure falls well short of first quarter 2012’s astounding 7.8%; nine of these ten asset classes underperformed their first quarter 2012 results, with only U.S. Treasuries able to beat the year-ago quarter. Emerging markets were notably weak during the period, underperforming first quarter 2012 by 17%.

Despite this disparity, why does it seem like this year’s bull market is so much better than last year’s? Many investors were on the sidelines during 2012 — as they had been since the onset of the financial crisis five years prior — and the overriding sentiment at the time was very bearish. Observers called 2012 a “stealth” rally, implying that many investors were either unaware of the gains being generated by the equity markets or unwilling to expose themselves to the perceived risks. Today, however, the nouveau bulls are out in force. Have attitudes truly changed? Or are these greenhorns merely “gaming diversification”, whipsawing from extreme risk avoidance to extreme risk indulgence rather than building broadly diversified portfolios meant to withstand the vicissitudes of markets over time?

U.S. Has Growth; Europe Hopes for Growth

Driven in part by the extreme accommodation measures of the Federal Reserve, the U.S. economy is gaining traction as Europe continues to flounder. Remember “eurosclerosis”? It was a derogatory term coined in the late 1970s/early 1980s to describe the consistently disappointing growth trend that gripped much of Europe for years. The region’s policymakers sought to combat this malaise and compete with the U.S. via the establishment of a common currency, the euro. As it turns out, giving a country all the benefits of a common currency without the accompanying accountability can cause lots of problems; most recently, we’ve seen Cyprus nearing financial collapse, Italy without a government, Spain with 26% unemployment, and France and the U.K. teetering on the brink of recession.

On this side of the pond, the U.S. is prospering as a result of tremendous natural and structural advantages emanating from what we call “tectonic shifts” in the global economy. These trends include:

- Global trade through our trade ports on both the Atlantic and Pacific coasts

- Energy, as we benefit from our abundance of natural gas, coal and oil resources

- Technology, where we lead the world in productivity gains driven by new innovations such as Big Data

- Frontier markets in which U.S. companies are poised to build new Starbucks using Caterpillar equipment on streets accessible to the next generation of latte lovers driving Fords and Buicks.

Can equity markets prosper with Europe contracting but the U.S. expanding? Well, with the most pronounced central bank stimulus since the dawn of civilization it sure seems that way — at least for now.

Market Fundamentals Remain Encouraging

Regardless of location, geography or stage of economic development, we recommend an in-depth exploration of any market’s underlying fundamentals prior to investment. Accordingly, we turn our attention to the ABCDs of market fundamentals.

Advancing earnings growth. After a negative print in the third quarter, corporate America returned to year-over-year earnings growth in the fourth quarter; with nearly all of the S&P 500 having reported fourth quarter results, growth came in at 4%. Earnings tend to trend; though it is unusual to reverse course like this, it is not without precedent. Does the fourth quarter represent a pause in a longer-term negative trend? Or was the negative third quarter, in fact, the aberration?

Broadening manufacturing. The energy revolution bolstered by inexpensive natural gas is not coming — it is already here. Cheap natural gas provides a distinct competitive advantage to onshore U.S. companies and continues to fuel the U.S. manufacturing renaissance.

- Manufacturing expanded for the third consecutive month in February, posting a strong reading of 54.2%. March results were a little less robust at 51.2% but firmly expansionary.

- The U.S. is the largest gas producer and has the second cheapest natural gas prices in the world next to Canada. Cheap natural gas additionally translates into cheap electricity, benefitting U.S. factories across the board.

- IHS Global Insights estimates that in 2012 the shale gas revolution, including exploration and extraction, accounted for $238 billion in economic activity, 1.7 million jobs and $62 billion in taxes.

- Unconventional oil and gas production is expected to spur more than $5 trillion in capital investment over the next two decades, also according to IHS Global Insight, potentially creating more than 3.5 million jobs.

- While certain transportation companies have been experimenting with a switch from diesel to natural gas to fuel their fleets, the transportation industry is not alone in potentially benefiting from cheap fuel. Industries that use natural gas as a raw material and energy source — such as chemical, plastics and fertilizer companies — stand to gain significantly as well.

Consumer as the game changer. Consumers took the end of the payroll tax holiday in stride and continued to push the economy forward. Despite GDP growth of only 0.4% in the fourth quarter, it sure feels like a good economy at the consumer level.

- Retail sales reached an all-time high of $421 billion in February.

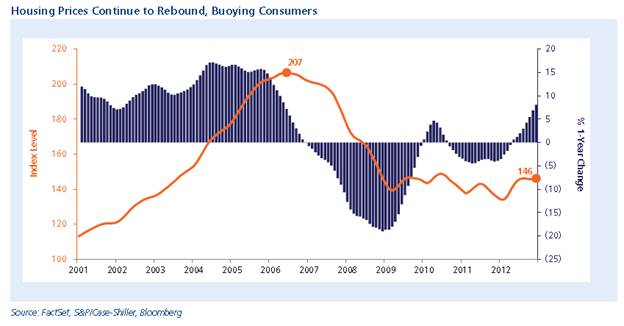

- Housing prices, as registered by the S&P/Case-Shiller Index, posted an 8.1% year-over-year increase in January — the strongest growth rate since June 2006 — to reach the highest level since September 2010.

- Although sales of new U.S. homes fell 4.6% in February from January, the level of new-home sales is 12.1% higher than one year ago.

- Existing-home sales rose 0.8% in February and are 10.2% higher than a year ago.

Developing markets. Last month we highlighted the PIVOT countries (Peru, Indonesia, Vietnam, Oman and Turkey) as future catalysts for growth, potentially complementing the BRIC (Brazil, Russia, India and China) economies that have been “emerging” for over 20 years at this point. Little-noticed Oman signed a free-trade agreement with the U.S. in 2009; should the U.S. begin exporting natural gas, Oman will be one of only 18 countries that could participate in this trade under current regulations. The U.S. currently exports items like machinery, vehicles, aircraft and agricultural products to Oman while importing crude oil, fertilizers and iron and steel products.

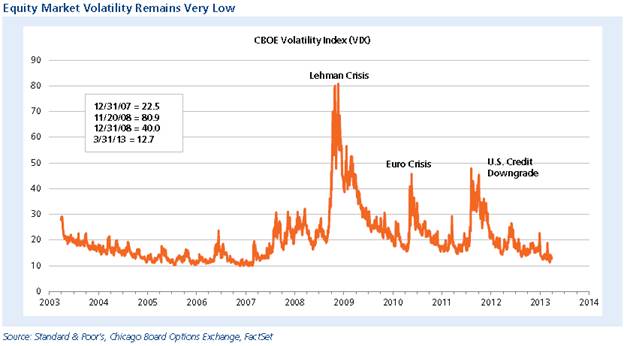

Broad Global Diversification Is Always Key

Broad Global Diversification Is Always Key

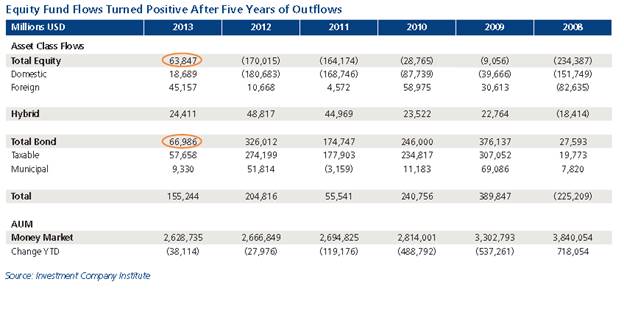

As part of its $85 billion per month quantitative easing program, the Fed purchased about $255 billion of U.S. Treasury and mortgage-backed bonds during the first quarter. All that new money has helped drive investors toward riskier assets; notably, fund flows into equities, which had been negative for five years, turned significantly positive in first quarter 2013.

Without any doubt, the Fed is intentionally promoting asset inflation for the housing and equity markets in order to support economic growth. Investors, especially those who remained on the sidelines as markets have rushed forward, would be well advised to recognize this and embrace a healthier risk appetite. But beware of taking risks that are excessive and/or not properly compensated — the “gaming diversification” that we have warned about for years. Fed Governor Jeremy Stein recently expressed his concern about overheating markets “when households extrapolate current good times into the future and neglect low-probability risks”.

U.S. economic growth appears on track — if somewhat tepid — while Europe is clearly in contraction and remains exposed to periodic negative surprises like Cyprus that send shockwaves into the global economy. So, how can investors both participate in a surging market and inoculate themselves from negative market surprises? The solution, of course, is a portfolio diversified both globally and broadly across equities and fixed income; when markets are prone to periods of low volatility followed by extreme and unpredictable bouts of instability, this is the most practical approach to protecting assets while also being positioned for growth.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 6074