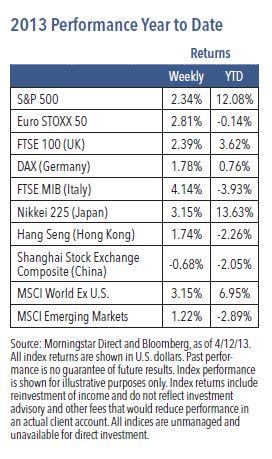

We wrote Part I of this theme on February 11 during the first quarter rally, when the S&P 500 closed the week at 1518. This past week the S&P ended at 1589, after increasing 2.3%.1 Global stock prices continue to push to new highs and thus provide support for a pro-equity bias. One nuance is that the composition of the equity rally has been abnormally defensive.

The Ongoing Question: What Can Be Sustained?

Defensive equity sectors have led cyclical sectors in recent months, and tradition- ally this has only occurred as global stock prices were falling. The unusual leadership is likely due to an increased number of lower conviction buyers facing uncertainty about a global recovery. We do expect earnings in cyclical sectors to outperform eventually and thus attract new investments.

There are many imbalances around the world: debt deflation pressures remain intense, and the authorities have been forced to counter with unorthodox easing. Choppy economic data and recent political backsliding in Europe have added to the anxiety. Therefore, the migration into assets with higher risk exposure has been quite slow. The U.S. has struggled with the lack of job generation, and job growth has been concentrated in a few lower-paying segments.

The good news is that the global economy is strengthening, a soft landing for China is already in place, the U.S. recovery is broadening and contagion from the Euro area should remain limited. Importantly, nearly all central banks are determined to pro- vide reflationary conditions. We believe this backdrop will support a progressively encouraging environment for equities and cyclical investments in particular.

Weekly Top Themes

- The U.S. earnings reporting season is mixed so far:2 The S&P 500 earnings have been in a $25 to $26 quarterly range since the third quarter of 2011, while S&P performance has been up 35% since then. Breaking above this level is prob- ably needed to sustain recent equity gains.

- March retail sales were weak:3 Sales fell 0.4% versus flat consensus expecta- tions. There is some evidence that the fiscal drag is taking a toll, especially on discretionary spending. Soft March retail sales provide further evidence of slower consumer momentum, and may suggest weak spending in the second quarter.

- The budget released by President Obama does not reach compromise: In our opinion, the budget does not help advance a grand bargain or tax reform. The plan did include provisions that will please Republicans, such as the Chained CPI social security reform and revenue neutral corporate tax reform. Debate over a grand bargain could be reignited when Congress turns its attention to the debt limit, which is not likely to be breeched until August.

- On Friday, gold broke below the bottom of its two-year trading range:4 Gold’s strong gains from 2008-2011 were largely due to credit crisis fears of global financial system collapse, unprecedented central bank balance sheet expansion and inflation concerns. These fears have since receded. We think it is unlikely gold will resume its previous upward trend without a new catalyst.

Trying to Avoid a Repeat

In each of the last three years there have been mid-year equity market corrections – and recurring unpleasant themes have resurfaced:

- European policy makers have taken another step back in their treatment of Cyprus

- The Citigroup economic surprise index for the U.S. showed that data has begun to mildly disappoint5

- However, a few positive developments may help limit these concerns:

- The European Central Bank (ECB) has committed to providing liquidity to the banking sector, which is important for sovereign risk problems in Europe

- After the political damage during debt ceiling negotiations in 2011, Republicans seem much less willing to engage in that battle again

- We believe that headwinds to U.S. growth appear less onerous: home prices are rising at an impressive rate and central bank policy is accommodative

1 Source: Morningstar Direct, as of 4/12/13. 2 Source: U.S. News & World Report, “Stocks edge higher as earnings reports begin,” 4/8/13, http://www.usnews.com/news/business/articles/2013/04/08/ stocks-open-lower-ahead-of-earnings-season. 3 Source: Bloomberg, “Retail Sales in U.S. Decline by Most in Nine Months,” 4/12/13, http://www.bloomberg.com/news/2013-04-12/retail-sales-in-u-

s-dropped-in-march-by-most-in-nine-months.html. 4 Source: Bloomberg, “Gold Tumbles to Lowest Since May 2011 After Entering Bear Market,” 4/14/13, http://www.bloomberg.com/news/2013- 04-14/gold-tumbles-to-lowest-since-may-2011-after-entering-bear-market.html 5 Source: Bloomberg, “Stocks Rise After China Inflation Slows; Yen, Euro Gain,” 4/9/13, http://www.bloomberg.com/ news/2013-04-09/japan-stocks-gain-to-4-1-2-year-high-as-asia-shares-metals-rise.html.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock

Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, includ- ing currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

![]() Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

GPE-BDCOMM3-0413P

© Nuveen Asset Management