Stocks Fall on Earnings Data

Equity markets bounced around wildly, finishing the week down slightly more than 2%.

Earnings were the primary market driver over the last week, but economic data in the U.S. and abroad was weaker than anticipated. There was some good news on the domestic front as housing markets displayed another bout of strength and industrial production remained positive.

In the housing sector, starts jumped from an annualized rate of 968,000 in February to 1,036,000 in March. The February figure increased from an initial report of 917,000. Housing starts are back near early 2008 levels and consistently trending higher. In the most recent report, though, most of the strength came from multi-family starts, rather than single-family homes. Multi-family units are notoriously volatile, generating a big asterisk next to March’s results.

Industrial production also showed strength in the month of March, rising 0.4%. Unfortunately, the gain was the result of increased utilities output and not manufacturing output. Cold weather across the country in March led to higher demand for utilities.

Consumers received favorable news last week in the form of the Consumer Price Index (CPI), which posted a 0.2% decline for March. That followed a 0.7% jump in February. Energy costs fell more than 2% as prices for gas were down sharply. Website gasbuddy.com reports that the average cost for a regular gallon of gas costs $3.50 today, compared to nearly $3.75 in late February.

Source: Gasbuddy.com

On an aggregate basis, economic data in the U.S. has been increasingly weaker in the last few months, as evidenced by the Citigroup Economic Surprise Index (CESI). The CESI measures the differential between reported economic data and expectations. The index retreated to negative territory recently, suggesting more economic data was coming in below expectations than above. This will be important to watch going forward, particularly as we enter a seasonally more difficult period for economic data.

The latest iteration of the Federal Reserve’s Beige Book confirms the CESI assessment. According to the Fed, the economy is expanding at a “moderate” pace with retail sales increasing, real estate markets improving and manufacturing activity picking up. That was offset by fiscal restraint in defense spending and headwinds associated with the expiration of the payroll tax cut.

Q1 Earnings Leave Much To Be Desired

Following the strongest first quarter in 15 years, it is not surprising to see equity markets faltering in April. Last week’s decline of 2.1%, however, may reflect deeper concerns about corporate fundamentals amid a mixed earnings season.

With approximately 20% of the S&P 500 reporting, 72% of companies beat consensus

estimates. This is slightly above recent averages, but is largely reflective of sharp downward revisions heading into the earnings season. Indeed, the blended earnings growth for the S&P is just 0.1% up to this point.

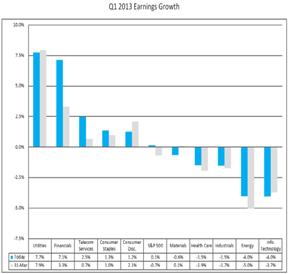

Source: J.P. Morgan

This weakness is broad-based, as four of the 10 S&P sectors are displaying negative year-over-year growth. Earnings growth is being propped up by utilities and financials, with aggregate growth rates of 7.7% and 7.1%, respectively. According to FactSet, however, just four companies are behind the entirety of the utility sector’s growth: Duke Energy, NRG Energy, Northeast Utilities, and Edison International. FactSet notes that mergers completed by two of the companies during the past twelve months distorted the year-over-year comparisons. Excluding these four companies, utilities’ earnings growth is actually negative in the first quarter.

Source: FactSet Research

Weakness in top line growth is more readily apparent, as just 45% of companies beat their consensus estimates. This is well below the 64% rate last quarter, and the blended growth rate of -0.2% is a stark reminder of the tepid economic environment.

This trend is evident in higher profile results such as J.P. Morgan and Wells Fargo. While companies are posting better than expected earnings results from lower loan loss reserves, revenues are trailing off as mortgage-refinancing volumes declined. With clear interest margin compression occurring in the industry, many market participants are questioning the momentum of the second highest source of growth for the S&P 500 index.

More troubling may be the continued insistence by analysts of double-digit growth in the back half of the year. Consensus expects 10% growth in the third quarter and 14% growth in the fourth quarter of this year. Revenue during that period remains tepid, at best, bringing into question the validity of those estimates. With margins already at all-time highs, it stands to reason that such substantial earnings growth is not possible without material top line improvement.

This pattern of overly optimistic projections is a familiar pattern in recent quarters. At this point one year ago, analysts expected earnings growth to jump to 16.3% in Q4 2012 and 12.1% in Q1 2013. Clearly first quarter results will finish nowhere near that estimate, and Q4 growth of approximately 4% finished well short of that mark as well.

Forward 12-month earnings per share (EPS) currently stands at $114.72; based on Friday’s closing price of 1555, that suggest the index is modestly valued at 13.6x, potentially giving markets further room to run. Based on recent history, however, it is more than fair to question those assumptions.

Source: Yardeni Research

2013 EPS estimates provided by Standard & Poor’s have already fallen to $109 from $117

12 months ago. Meanwhile, calendar year 2012 EPS came in at $96.82, down from an index peak of $98.69 (trailing four quarters) in Q2 2012. It would be a big surprise, indeed, if earnings can climb more than 11% above their historical high by the end of the year. Even if the Q1 target of $25.40 per share were reached, that would only equate to a trailing four quarter EPS of $97.98 – valuing the market at approximately 15.9x.

How earnings evolve over the next few quarters will go a long way in determining the direction of equity markets from here. Estimates for substantial earnings pick up may be farfetched, leaving any further run in stocks to multiple expansion. That may be a plausible outcome, given renewed risk appetites by investors, but deterioration in fundamentals is not the key to a sustainable bull market.

The Week Ahead

Earnings will remain front and center this week, with a wide range of companies reporting, including Caterpillar, Halliburton, Apple, DuPont, Boeing, Daimler, Amazon, and Chevron.

Economic data will contain a mix of important releases, from existing home sales and durable goods orders to first quarter GDP.

Several central banks are meeting this week, with a focus on those in Mexico, Colombia, New Zealand, Hungary and Japan.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

For more information, please visit our website at http://www.Fortigent.com.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent