“Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria. The time of maximum pessimism is the best time to buy, and the time of maximum optimism is the best time to sell.”

Sir John Templeton, 1912 – 2008 Investor and mutual fund pioneer Philanthropist and spiritualist Trustee of Princeton Theological Seminary for 42 years

Sir John Templeton was arguably one of the 20th century’s greatest investors. He was a pioneer when it came to international investing, building the hugely successful Templeton Funds. Following his mantra of buying at maximum pessimism, while Europe was at war in 1939, he borrowed money to buy 100 shares of 104 companies trading under a dollar a share. Only four turned out worthless, the rest earning him a considerable sum. Templeton’s wisdom stemmed from his open mindedness and lifelong pursuit of learning. He applied the tools of modern science in pursuit of spiritual enlightenment and an understanding of the world around him. Key to Sir John Templeton’s success was his mindset that uncertain times bring opportunity and inevitably give way to human progress.

We digress from Sir John and his quote to discuss the European debt crisis: the gift which keeps on giving (uncertainty). The country now in the news is tiny Cyprus, which received a bailout for its banks from the European Union (EU), but only after agreeing to steep losses for those banks’ large depositors. Hitting up bank deposits represents a new dimension to the European debt crisis and illustrates how in a crisis, leaders can and often will resort to whatever means are necessary. When the Cypriots first requested a bailout from the EU and were told their depositors had to suffer, they balked and said that was unacceptable… until a few days later when they realized they had no other choice and accepted an even harsher deal. Cyprus is a tiny country which has set a large precedent: all Euros are no longer created equal… those in Cyprus are now subject to capital controls and are subsequently worth less. The financial world was also reminded of a not-so-pleasant fact: bank depositors are creditors. What will happen when the next country starts to teeter? Will money, fearing the Cypriot treatment, flee the wavering country, hastening its downfall? Will the same thing happen with teetering banks? Why is Europe willing to set this precedent and risk the contagion of a country-wide banking run? Why the grab for heretofore sacrosanct bank deposits?

The key consideration is that through this strategy, creditors, as opposed to (German err, European) taxpayers help foot the bill, and a further increase in government debt levels is avoided. If one accepts our basic belief that a debt crisis is not over until there is less debt, the treatment of Cyprus becomes understandable… perhaps even a necessity… both there and elsewhere1. Over the past few years, we have seen a parade of bailouts that have only succeeded in transferring debts: small bank to big bank, big bank to government, government to a group of governments (EU bailout fund). Did these bailouts solve the problem? What in fact is needed is not for the debt to be moved, but eliminated.

For previous crisis sufferers, it’s too late to impose any losses on depositors, the debt lies with the governments. Now, the governments might eliminate this debt by paying it back, but “austerity” is not a vote winner and economic growth is running insufficient to dent debt levels. Hence, so far, moving debt from banks to governments has in no way been a successful recipe for eventually paying it off… so far it has just been sitting there, building. In the same way that Hemmingway wrote about going broke gradually, then suddenly, European states are not at the moment going broke suddenly (i.e. bond yields are not spiking)… but they are still going broke gradually (running deficits and increasing debt). The European debt crisis will not be over until either 1) the debt goes away (read: default or substantial inflation) or 2) these governments start producing actual surpluses with which to pay the debt down. The dam is holding up for now, but the water level is still rising and the pressure isbuilding amid the weakest economic readings outside of war-time that Europe has seen in over a century.

Source: JP Morgan

Back in the U.S., stocks were ablaze the first quarter, soaring over ten percent to reach new all-time highs. Calling to mind his advice, is Sir John Templeton cautioning us that euphoria stands ready to gore the bull? Perhaps… but perhaps not. Stocks are indeed up, but are we seeing signs of euphoria?

Observe the chart at the top of the next page, which shows the Dow (DJIA) and Consumer Confidence Index over time. Since the late 1960’s, meaningful stock market peaks have not been reached while at the currently depressed level of confidence. In fact, the DJIA has advanced at its best rate (14.7% annualized) when confidence readings were below 66… which is the case now.

Source: Ned Davis Research

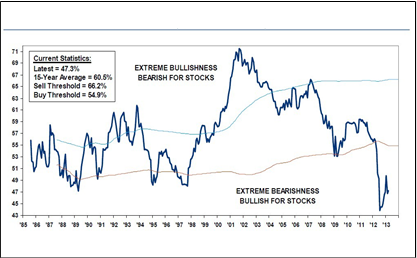

Likewise, the consensus of Wall Street strategists, the so- called “Sell Side” (shouldn’t the name alone bear warning) is more negative on stocks than it has been in decades and recommends portfolios receive equity allocations below 50%. Given that peak equity exposure was recommended at two not-so-propitious peak market moments (the internet bubble in 2000 and the housing bubble in 2007), we consider this lack of euphoric feeling to be positive for stocks.

Sell Side Consensus Indicator (as of March 31, 2013)

Source: Bank of America/Merrill Lynch

Institutional investors too have given up on stocks. A 2012 study indicates pension fund bond (fixed income) allocations have grown to 41.4%, rising past their 38.1% allocation to stocks (equities).

Source: Strategas Research Partners

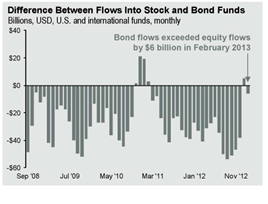

In January, inflows to equity funds exceeded inflows to bond funds for the first time in two years, and produced breathless talk of a “great rotation” from stocks to bonds that was supposedly getting underway. As this chart demonstrates, the excess of equity over bond fund flows was a veritable drop in the bucket and was reversed the very next month. In fact, amid diminishing signs of world economic growth and confiscation of bank deposits in Cyprus, investor sentiment during April contracted to the point that only 19% of those surveyed by the American Association of Individual Investors (AAII) confessed to being bullish. We note that the last such reading in March of 2009 unleashed the beginning of the current bull market. We can identify ten other times AAII bullishness was found below 20% during the last 25 years. In all but one case, the S&P 500 Index was higher six months later, with an average increase of 10%.

Source: JP Morgan

Source: Strategas Research Partners

Corporations have also piled on the cautionary bandwagon, issuing negative earnings preannouncements with a frequency well above the ten year average. Historically, above average equity performance has followed elevated negative preannouncement levels.

Source: JP Morgan

Further examples of low expectation for equity appreciation are the strong preference for dividend paying stocks and the leadership of “defensive” sectors (health care, consumer staples and utilities). These sectors are responsible for the majority of the S&P 500 Index gains so far this year. Investors are paying a premium for potential safety, as this chart highlighting the difference in price to earnings (P/E) ratios between “cyclical” and “defensive” stocks demonstrates.

Source: JP Morgan

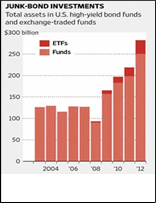

So if stocks aren’t bathing in sunshine, what might be? Well, $780 billion of “high yield” debt (junk bonds) was issued over the last three years, more than during any other three-year period in history. And yet, despite this abundant supply, junk bonds have never yielded less than they do today, indicating demand for these bonds (which promise less than they ever have before) is still quite healthy. We’ll stop short of saying we’ve reached euphoria, but we call lending money to risky businesses with historically little promised return optimistic.

Source: The Wall Street Journal

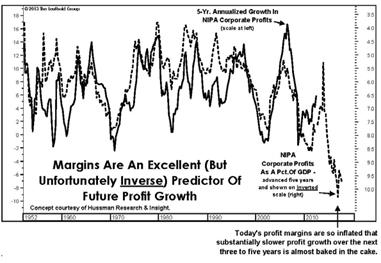

Moving from current attitudes to current affairs, another continuing area of concern is the future for corporate profits given that current margins are at generational highs. The following chart shows the five-year trajectory of U.S. corporate profits (the solid line) based upon starting profit margins (profits as a percent of GDP - the dashed line, inverted and advanced five years). The margin trend line is inverted meaning high margins have historically led to low profit growth over the subsequent five years. Hence profit growth in coming years could be minimal or even negative… which would certainly represent a headwind for stocks.

Source: Leuthold Group

And what of the North American debt crisis? Well, they’re not calling it that yet, but the U.S. isn’t so different from Europe. We just haven't had a true bout of going broke suddenly (yet). It may not be in the headlines, but we continue to pile on the debt. The U.S. is living outside reality, spending in excess of what the economy can contribute. Reality is that the U.S. economy is expected to produce roughly 2% real GDP growth this year, marking the eighth consecutive year of real growth below 3%. As perspective, the next longest string of real GDP growth below 3% was a four-year streak back in the 1930s.

In the U.S., given the resistance to and difficulty of collecting higher taxes, we believe the eventual fiscal solution will likely involve substantial movement on health care of some sort, because of how much of the budget it consumes. Social security, Medicare, and Medicaid are very popular and thus, incredibly, were not part of recent budget sequester, but mathematical reality will eventually require otherwise. Suffice it to say, we expect there is another crisis coming, in both the U.S. and Europe.

Source: Strategas Research Partners

So what do we do with this information? What does the intelligent investor do when he knows the pressure for a crisis is building? The answer might surprise you: not much. Do we sell stocks and head for the hills? No. Despite rising pressure, it’s far too difficult to tell when the dam might break. Even if one knew the tech bubble was coming in 1997, you probably would have fared better by riding it up and down than sitting out the whole thing in cash. It could be years, or maybe a decade, before any crisis occurs… or corrective action could be taken in time and no crisis ever occurs at all. Anyone who thinks they know the future is fooling themselves. Meanwhile, while waiting for the 15% crash, the bigger underlying trend of progress and prosperity may have moved stocks up 20%. That’s not to say awareness of potential problems is wholly useless. We can benefit in two ways: First, we know not to get carried away by optimism, and can attempt to build stability in the portfolio to keep fragility out. Second, we can carefully monitor the situation for signs of a breaking point, and then when spotted, forearmed with our knowledge that the crack is likely to widen and burst, anticipate the imminent crisis and shield ourselves from the brunt. It is through this prism that we think about the brewing problems of the world.

For the time being, however, and as we pointed out earlier in this letter, we believe the more immediate and impactful driver for investments is the sufficient pessimism and skepticism necessary to sustain markets upward overall. In a somewhat perverse way, in fact, one might even say that the stock market is compelling because of these valid but well-known fears and therefore will actually return more because of these probable but well-publicized follies. We’ll end this letter by allowing Sir John Templeton to re-state this paradox, probably in better fashion, through his 1993 words:

“Do not be fearful or negative too often. For 100 years optimists have carried the day in U.S. stocks. Even in the dark ’70s, many professional money managers—and many individual investors too— made money in stocks, especially those of smaller companies.

There will, of course, be corrections, perhaps even crashes. But, over time… stocks do go up… and up… and up.

By the time the 21st century begins - it’s just around the corner, you know - I think there is at least an even chance that the Dow Jones Industrials may have reached 6,000, perhaps more.

Chances are that certain other indexes will have grown even more. Despite all the current gloom about the economy, and about the future, more people will have more money than ever before in history. And much of it will be invested in stocks.

And throughout this wonderful time, the basic rules of building wealth by investing in stocks will hold true. In this century or the next it’s still “Buy low, sell high”.”

We thank our loyal clients for tolerating an uncertain world which we believe offers compelling investment value at this time.

Very Truly Yours,

John G. Prichard, CFA

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

© Knightsbridge Asset Management