The bedrock of GMO’s investment philosophy is reversion to the mean. We believe that capitalism should cause the return on capital to be in line with the cost of capital, and that assets that embody similar risks should offer similar long-term returns. These beliefs, in turn, guide our assumptions that equities should trade at replacement cost, that the long-term return to equities should be approximately the same as their normalized earnings yield, and that assets without long return histories should have similar valuations and equilibrium returns as related assets with longer histories.

These beliefs have allowed us to sleep reasonably easy even at times, such as the late 1990s or 2006-7, when valuations and returns were doing things we thought were irrational. And they have also allowed us to take the leap into assets such as emerging equity and debt, REITs, and TIPS even when we did not have a lot of historical data to confirm the apparent cheapness of those asset classes.

But our sleep is not always altogether easy. There are times when the markets do not seem to be following the script properly, and we are left wondering whether we are dealing with a temporary anomaly or a more permanent problem. Today we are faced with one of these problems: the persistently high profit margins of U.S. corporations. High profit margins should not persist in a mean-reverting world, and yet profitability in the U.S. has been higher than long-term averages for most of the last 20 years, oddly pretty close to the same length of time that the U.S. market has been trading above replacement cost.

At first thought, it may not seem that odd that high profitability is associated with an expensive stock market – after all, shouldn’t investors be willing to pay more for assets that achieve a high return? But high valuations imply a low cost of equity capital, which should encourage corporations to issue more equity, and a high return on capital should encourage corporations to do more investing. These pressures should gradually push the cost of capital up and the return on capital down. But in the period since the mid-1990s, stock issuance has been down and corporate investment has fallen as well, in apparent contravention of the basic rules of capitalism. A high return on capital that occurred simultaneously with a high cost of capital – that is a market selling below replacement cost – would make sense because there is no discrepancy to arbitrage. The current situation is not supposed to happen, which makes it tricky for us to understand exactly when it will end.

As investors, we believe that our first job for our clients is to try to avoid losing them money. Therefore, we have chosen the path of conservatism in our forecasts, assuming that profitability will revert. It is always possible we are wrong and we are doing a disservice to the U.S. stock market (and most other stock markets around the world, which also show elevated profit margins), but it does not seem prudent to assume a non-equilibrium situation will persist indefinitely, even if it has gone on for a surprising length of time. Herb Stein’s Law states “If something cannot go onforever, it will stop.” History has been kind to Stein’s Law, but there should probably also be a related admonition: “If something that cannot go on forever has been going on for an inexplicable length of time, try to understand why it has been going on so long and whether your model might be the problem.” I admit it is nowhere near as pithy as Stein’s Law, but the rest of this paper will be an attempt to follow that admonition where it leads us. For those who don’t want to read through the gory details, the result is that there are ways for profits to stay high indefinitely, but it is far from obvious that society will be willing to put up with them.The Current Situation

I do not want to give the false impression that today’s profitability is fundamentally inexplicable. Today’s profitability makes perfect sense in light of the current conditions in the economy. As my colleague James Montier pointed out in his paper “What Goes Up Must Come Down,” we can use the Kalecki equation to understand the level of profitability from a macroeconomic perspective. Unlike our beliefs about equilibrium in a capitalist system, the Kalecki equation holds at all times, being an economic identity. The equation, for anyone who has not committed James’s piece to memory, states:

|

Profi ts |

= |

Investment |

+ |

|

Dividends |

- |

||

|

Household Savings |

- |

||

|

Government Savings |

- |

||

|

Foreign Savings |

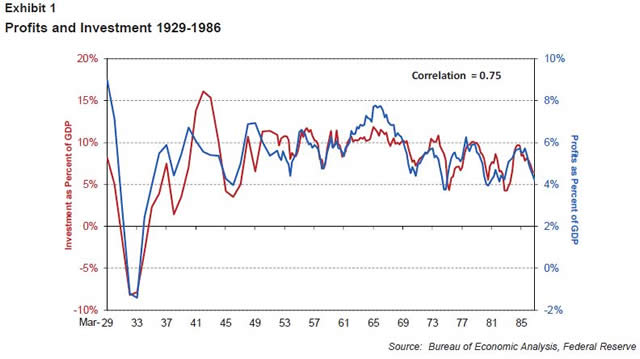

Historically, the major driver of the ebb and flow of profits has been the ebb and flow of investment, as we can see in Exhibit 1.

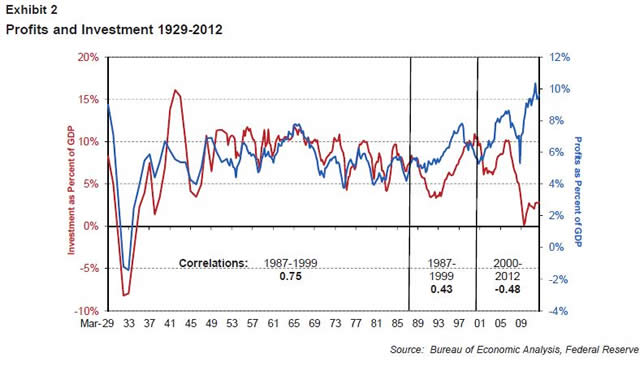

Up until 1987, this was a very tight relationship, with a correlation of 0.75 between investment and profits. However, in recent years, the situation has changed, as we can see in Exhibit 2.

From 1987-99, we saw a marked deterioration in the correlation between the two series, and since 2000 the relationship has been positively perverse, with a correlation of -0.48. As the Kalecki equation states that, all else equal, lower investment should lead to lower profitability, it must be the case that all else has not been equal. And sure enough, very few things have been equal since 2000.

In the 1990s, the investment associated with the internet bubble did indeed lead to high profitability – and perhaps we can forgive the relationship for not being even stronger than it was because the major factor driving down profits in the last few years of the 20th century was the lost profits associated with the extraordinary wealth transfer to some lucky workers in the form of stock options on technology companies. From a national income account perspective, the money that employees received from the exercise of their options is counted as a cost to corporations. It’s easy to have sympathy for this accounting, as the losers in the exchange were shareholders who wound up giving away untold billions to the option holders. But thanks to the power of the technology companies’ lobbying efforts, stock options are not properly expensed under GAAP accounting even today, except in a footnote.

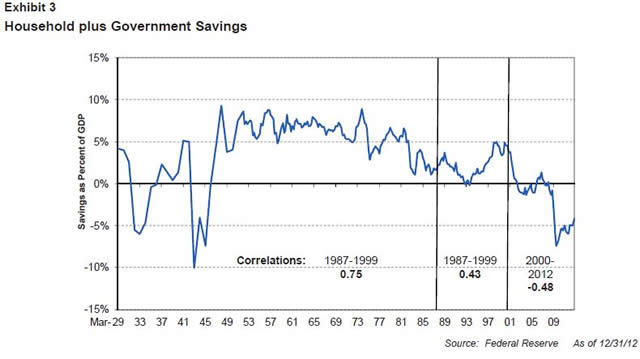

Since 2000, investment has fallen off to levels lower than we have ever seen apart from the Great Depression, and yet profitability has risen to an all-time peak. This has been possible because other pieces from the Kalecki equation have kicked in in a way we haven’t seen before. Exhibit 3 shows the sum of household and government savings as a percent of GDP.

Apart from the Great Depression and the latter part of World War II, the combination of the household and government sectors has saved around 3-7% of GDP. From 2001 to 2007, the sum hovered around zero, and since the financial crisis, we have been bouncing around somewhere near -5%. This means that relative to the last 60 years of U.S. history, household and government savings are responsible for profits being about 10% of GDP higher than they would otherwise be. As profits are approximately 10% of GDP, one could say that this burst of profligacy has been responsible for more or less all of corporate profitability since the financial crisis.

We could chalk this up as a fine example of Stein’s Law – profit margins are high because savings rates are unsustainably low, savings rates must eventually come up, and therefore profits will eventually come down – except for two problems. The first is that profit margins have generally been high since the mid-1990s, long before savings went negative. And the second is that there is no guarantee that all else will be equal. Perhaps other pieces of the Kalecki equation will help keep profits high.

Dis-equilibrium in the System

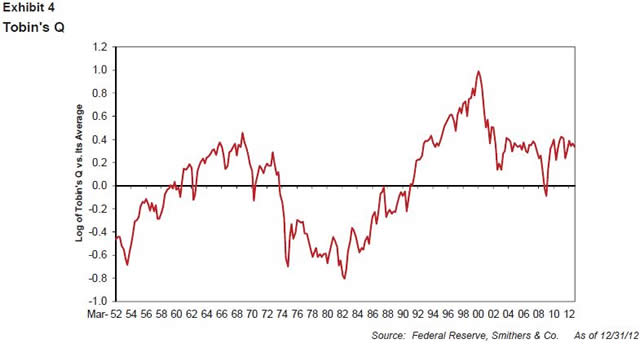

Returning to the equilibrium arguments I started the paper with, the odd thing about this period from the perspective of a profit maximizing capitalist is that we’ve had an extended period of time with a high return on capital and a low cost of capital without having the expected response of increased equity issuance and increased corporate investment. Exhibit 4 shows the price to replacement cost of the U.S. stock market over time.

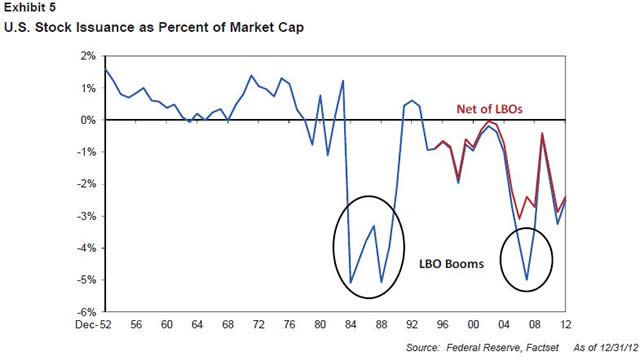

Apart from about 5 months from late 2008 to early 2009, we have traded above the long-term average continually for 20 years. This should have been an inducement to issue stock, but this has definitely not shown up on an aggregate basis, as we can see in Exhibit 5.

One factor that has confused the situation since the mid-1980s is the existence of LBOs, which count as stock buybacks. In principle, this should even out in the end because the goal of private equity firms is to eventually sell the companies they buy back into the public markets, either through an IPO or selling to another public company. As it happens, the size of the portfolios of private equity firms has ballooned over time, so we have net had more companies taken out of the public markets than put back. We don’t have good data on LBOs before 1995, but we’ve also shown the series net of LBO activity since then, and the basic pattern persists. The period since the mid-1990s, which seems like it should have shown a long wave of issuance, has instead shown the longest period of net buybacks we have ever seen.

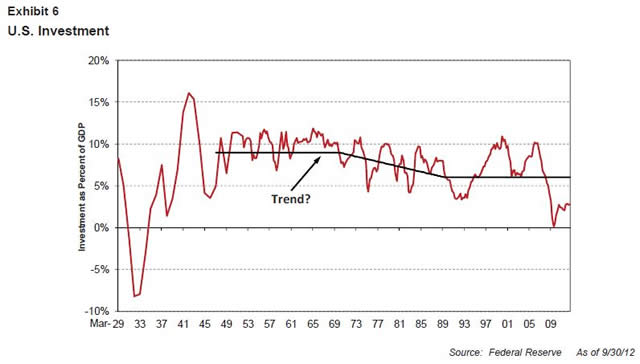

We have talked about the investment fall-off in the U.S., but it’s worth showing again, without the profit series superimposed, in Exhibit 6.

The fall-off in investment has really been just since the financial crisis. Before that, overall investment looked about normal. Admittedly, it did not really push above the levels of the 50s, 60s, or 70s. On the other hand, it does look as if the series has had a declining trend since the 1960s, which would have put “normal” for the 1990s and 2000s at around 5-6% of GDP, down from 8-10% in the immediate post-WWII period. Relative to that possible trend, we did see a couple of bursts of investment that coincided with the internet and housing booms, but the current period is truly an anomaly. Corporations are making plenty of money – profits are just off their all-time high relative to GDP – but investing less than at any point since the Great Depression.

It is as if corporations view their current profitability as a windfall rather than a permanent condition. Viewing the profits as a windfall certainly isn’t irrational, but it is surprising for corporations that have been living in a world of high profitability for close to two decades to be so cautious. Andrew Smithers of Smithers & Co. has argued that U.S. corporations’ unwillingness to invest is a symptom of the “bonus culture” in which CEOs who realize their tenure may not be all that long focus their attention on activities that can bring stock prices up in the short term so they can get rich quickly, and ignore the long run as it is unlikely to come about on their watch. He may well be right, but the fall-off in investment has occurred more recently than the rise of bonuses, stock options, and revolving-door CEOs, so even if “bonus culture” is the answer today, that doesn’t mean investment rates will remain low indefinitely.

And if investment were to rise from here, we know from the Kalecki equation that in the near term it would be a plus for profits, even though I argued early on that investment should, in the longer run, compete down high profitability. From a macro-economic perspective, it is easy to see why high investment generally equals high profits. Investment can be redefined as “that which is depreciated over time.” It is this, after all, that separates investment from consumption. The trouble with consumption is that one entity’s revenues are another entity’s costs – if an automaker buys steel, it is revenue for the steelmaker and a cost for the automaker. But if the automaker buys a stamping machine to turn that steel into a car door, it is revenue for the producer of the machine, but not officially a cost for the automaker. It is “investment” and so does not get subtracted from the income of the automaker. This is true even if the automaker never actually uses the machine, or uses it to make car doors that no one ever buys. In those circumstances, the automaker will eventually have to write off the investment, reducing future profits, but the original investment increases profi ts in the period it is bought regardless of the usefulness of that investment in theend. So in the short run, were we to get a burst of investment today, it would cause profits to go up, holding all else equal. In the longer run, it would increase industrial capacity and put pressure on margins.

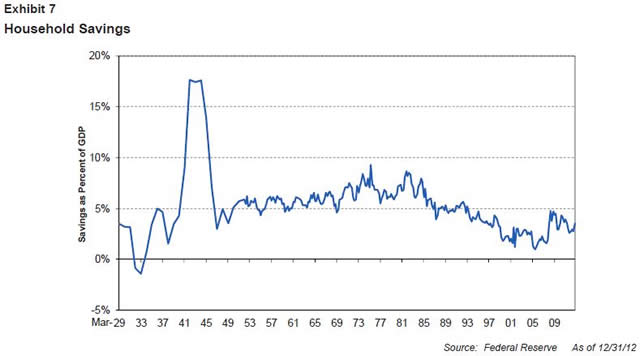

But what if we never get that increase in investment? What if investment stays low and that pressure on profits does not materialize? Could profits stay high forever? They could, but there would be implications that might not be sustainable. If profits are to stay high while the government deficit shrinks, we would need other pieces of the equation to pick up the slack. We would need to see some combination of a shrinking current account deficit, falling household savings, and rising dividends. The U.S. current account deficit could improve from here, particularly insofar as rising oil and gas output allows us to cut back petroleum imports. But given the generally weak economic environment outside the U.S. and a U.S. dollar that has been strengthening versus trading partners, it seems unlikely that this will be a large effect. We could see a falling household savings rate. The current rate looks to be on the low side, as we can see in Exhibit 7, and that does make a falling rate seem implausible at first.

But perhaps this series is a bit misleading. We saw from Exhibit 5 that net stock buybacks have been running at high levels for a long time now. A stock buyback is really the same thing as a one-off dividend payment from the standpoint of shareholders, and the household sector in one way or another holds a large fraction of the stock market. Perhaps we need to adjust savings rates upward since the mid-1990s for buybacks. This wouldn’t be enough to bring savings rates up to long-term averages – some of the buybacks accrue to the benefit of foreign shareholders and this income is not properly captured as a negative in the current account balance – but it does mean that savings rates might not need to rise much as the long-term trend suggests. And if corporations are not investing, they can pay out more profits as dividends, which is also a plus via the Kalecki equation. High profits with high dividends – either “true” dividends or “effective” dividends through stock buybacks – is a sustainable situation according to the Kalecki equation.

But while households do hold much of the stock market, those holdings are not spread equally. In fact, as unequal as the income distribution is in the U.S., the wealth distribution is far more unequal still. Furthermore, the predominant stores of wealth for the middle class are home equity and savings in the bank, so dividends accrue overwhelmingly to the rich. The rich have been doing very well in the past 30 years, even in terms of their share of labor income. Giving them a permanently large slug of income from capital as well will probably eventually cause a backlash even among the impressively stolid U.S. electorate. The belief in social mobility in the U.S. has been a strongly enduring one, but as copious research has shown in the past few years, it is increasingly a myth.1 An increasingly permanent upper class, which not only does far better in terms of labor income than the rest but further accumulates a further chunk of GDP in the form of persistently high dividends and stock buybacks, is likely to accumulate enemies.

Even if the rich avoid this problem, it is essential that they actually spend their income in order for profits to stay high. The very wealthy tend to save a large chunk of their income, so if the distribution of income is skewed ever more in their favor, the need will arise for the less well-off to spend more than 100% of their income to stop the savings rate from rising. And rising savings, all else equal, hurts profits. Negative savings rates for the bulk of households actually seem to have been the case in the 1990s as people spent on the assumption that the stock market would always go up, and they occurred again in the 2000s as people spent on the assumption that home prices would always go up. More recently, the un- and under-employed have been spending more than their income because their incomes have fallen yet they still need to live. But with the possible exception of those lending to governments, there eventually comes a time when lenders stop lending to those who want to spend more than their income. If the rest of households stop dis-saving, it will require the rich to really up their spending to keep the system going. There may not actually be enough goods and services for the rich to buy to make this work, but even if it were possible, it would almost certainly increase the resentment of the have-nots until they took it out on them through the ballot box, if nothing else.

Conclusion

The image of a dystopian future in which the rich gate themselves off from the rest of society for protection while buying off politicians to ensure their continued privilege2 doesn’t help us at all in understanding when the current situation will end. And the reality is that we really don’t know when it will. All else equal, falling budget deficits will hurt profitability, but if we do finally get the much-delayed recovery in investment or continued strong buyback activity, it is possible falling deficits could be absorbed without margins falling back toward historical averages. Rising investment would, in all likelihood, sow the seed of falling profits in time through increased competition, as would buybacks and dividends through rising savings or a societal response. But as for when, it is impossible to know.

For us at GMO, the timing matters, but it is only of secondary importance. Given the very long duration of equities, even another decade of above-normal profits would serve only to increase the fair value of the stock market by perhaps 10 percentage points. It is only if profits are truly permanently higher that the impact is a really big deal. Can we swear that such a permanent increase is truly impossible? No. But it seems to us entirely imprudent to assume that such a permanent increase is in the cards, when the implications of being wrong would be quite damaging to our clients’ portfolios.

1Among other studies, see “U.S. Economic Mobility: The Dream and the Data,” by Leila Bengali and Mary Day, Federal Reserve Bank of San Francisco, March 2013.

2Admittedly, how dystopian this looks probably depends a lot on which side of the gate you are on.

Appendix: Global Return on Equity Capital

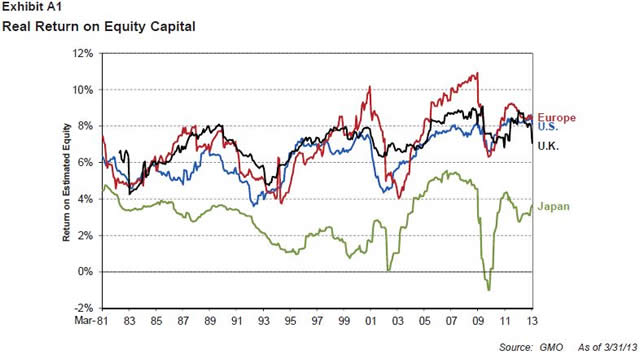

There have been a number of commentators who have complained that a focus on U.S. profits as a percent of GDP is misleading, because in a global economy it is world GDP that should be in the denominator, not U.S. GDP. We think this is unlikely to explain currently high U.S. profitability because profit margins seem to be elevated in most places around the world. Surprisingly few countries provide their corporate profitability data as conveniently as the U.S. does, but for publically listed companies across the developed world, we can look instead at their real return on equity capital. This is a bit trickier than it sounds, but Martin Tarlie of our Global Equity team has led a group focused on putting together our best estimate for a true return on equity capital. The result of their efforts to date is presented in Exhibit A1.

Continental Europe and the U.K. have a surprisingly similar pattern of return on capital to the U.S. While Japan has clearly lagged behind, relative to its rather miserable historical standards, it, too, has had pretty good profitability over the last eight or nine years. This kind of analysis actually takes a good deal of historical data to come up with a good estimate of equity capital. We don’t have a long enough history on the emerging equity markets to do the same analysis, but we can look at return on stated book value as an imperfect proxy, as seen in Exhibit A2. On this basis, emerging profitability is less far above normal, but we see the same basic pattern of high profitability over the past eight or nine years with a dip for the financial crisis.

If U.S. corporations are not as anomalously profitable as they seem because we should be measuring U.S. profits against U.S. and not global GDP, then we should see them benefitting at the expense of foreign competitors. Profitability that is high around the world cannot be due to one group of companies disproportionately benefitting from global trade. Global profits are almost certainly near all-time highs as a percent of global GDP, which means any rationalization cannot rely on a local explanation or a problem properly calculating the profitability of a particular group of stocks.

Mr. Inker is the co-head of asset allocation.

Disclaimer: The views expressed herein are those of Ben Inker as of April 26, 2013 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

Copyright © 2013 by GMO LLC. All rights reserved.

© GMO