We have all witnessed a major move in Treasury rates over the last couple months, causing concern for many that we may well be in the early stages of a rising interest rate environment. The traditional thought is that as interest rates rise, bond prices fall. But looking at history, the high yield market has defied this widely held notion. Let’s examine the four main reasons why high yield bonds have historically performed well during times of rising interest rates.

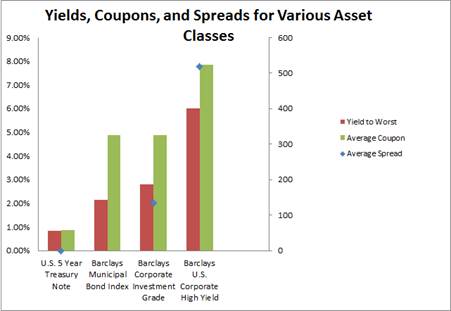

1) Higher coupons and yields in the high yield space help cushion the impact of rising interest rates. High yield bonds, as the name would suggest, have traditionally offered among the highest coupons/yields of various fixed income instruments. The following chart graphically depicts yields, coupons, and the spread over Treasuries for several fixed income products.1

So, let’s think about this intuitively for a minute. If you own a bond with a yield of 2.5% and interest rates move up 1% that would obviously have a meaningful impact, as we are talking about move equivalent to 40% of your total yield. However, if you are at a yield of over 6.0% on a bond and interest rates move that same 1%, that impact is significantly less. So the higher the yield, the less the interest rate sensitive the bond.

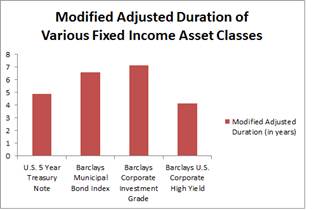

2) High yield bonds have shorter durations than other asset classes in the fixed income space. Duration is a measure of sensitivity to changes in interest rates that incorporates the coupon rate, maturity date, and call features of a bond. The fact that high yield bonds are typically issued with five to ten year maturities and are generally callable after the first few years, as well as that they offer higher coupon rates, provides the high yield sector with a shorter duration versus other asset classes. We’ve profiled some duration comps below:2

3) The prices of high yield bonds have historically been much more linked to credit quality than to interest rates. Historically interest rates are increasing during a strengthening economy and a strong economy is generally favorable for corporate credit and equities alike. Due to the nature of the high yield bond market, the major risk on the minds of investors is default risk (not interest rate risk), causing them to be much more concerned with the company’s financials and credit quality than interest rates. When the economy is expanding, profitability, financial strength, and credit metrics often improve as well. So a stronger economy, if we were to get there, would undoubtedly be a positive from a credit perspective and would indicate lower default rates, meaning improved prospects for the high yield market.

4) High yield bonds are negatively correlated with Treasuries. High yield bonds have a zero to negative correlation with Treasuries, meaning that as Treasury prices go down due to yields (interest rates) increasing, high yield would theoretically experience no change or the opposite change (increase) in pricing. Additionally, while high yield is still positively correlated to investment grade, it is a fairly low correlation; yet, we see a strong correlation between investment grade and Treasuries. As a recent J.P. Morgan report explained, “Over the past 15 years, high-yield bonds exhibit correlations to movements in the 10-year Treasury bond of -0.3 versus a far higher correlation of +0.5 for high-grade bonds.” Looking over just the last five years, we see a similar takeaway.3

Given these low or negative correlation rates versus other asset classes, especially the more interest rate sensitive asset classes such as investment grade, an allocation to high yield bonds can help serve to improve portfolio diversification and potentially lower risk.

Those are nice thoughts, but let’s look at some hard data as to how high yield has actually performed in a rising rate environment. Since 1980, Treasury yields have increased (i.e., interest rates rose), in 14 of those years. A J.P. Morgan piece concluded that “in each of those 14 years, high yield has outperformed its higher rated counterpart.”4 The actual numbers show that over those 14 years, high yield had an average return of 14.1% (or 10.6% if you exclude the massive performance in 2009).5 This compares to only a 4.9% average return (or 3.9% excluding 2009) for investment grade bonds over the same period.

|

Year |

J.P. Morgan High Yield Bond Index Return |

J.P. Morgan Investment Grade Corp Bond Index Return |

5- year Treasury |

Change in 5 Yr Treasury Yield |

|

1980 |

4.3% |

0.5% |

3.9% |

2.21% |

|

1981 |

10.4% |

2.3% |

9.5% |

1.38% |

|

1982 |

36.3% |

35.5% |

29.1% |

-3.82% |

|

1983 |

20.3% |

9.3% |

7.4% |

1.38% |

|

1984 |

9.4% |

16.2% |

14.0% |

-0.46% |

|

1985 |

28.7% |

25.4% |

20.3% |

-2.58% |

|

1986 |

15.6% |

16.3% |

15.1% |

-1.68% |

|

1987 |

6.5% |

1.8% |

2.9% |

1.59% |

|

1988 |

11.4% |

9.8% |

6.1% |

0.73% |

|

1989 |

0.4% |

14.1% |

13.3% |

-1.30% |

|

1990 |

-6.4% |

7.4% |

9.7% |

-0.15% |

|

1991 |

43.8% |

18.2% |

15.5% |

-1.75% |

|

Year |

J.P. Morgan High Yield Bond Index Return |

J.P. Morgan Investment Grade Corp Bond Index Return |

5- year Treasury |

Change in 5 Yr Treasury Yield |

|

1992 |

16.7% |

9.1% |

7.2% |

0.06% |

|

1993 |

18.9% |

12.4% |

11.2% |

-0.79% |

|

1994 |

-1.6% |

-3.3% |

-5.1% |

2.62% |

|

1995 |

19.6% |

21.2% |

16.8% |

-2.45% |

|

1996 |

13.0% |

3.7% |

2.1% |

0.83% |

|

1997 |

12.5% |

10.4% |

8.4% |

-0.50% |

|

1998 |

1.0% |

8.7% |

10.2% |

-1.17% |

|

1999 |

3.4% |

-1.9% |

-1.8% |

1.80% |

|

2000 |

-5.8% |

9.9% |

12.6% |

-1.37% |

|

2001 |

5.5% |

10.7% |

7.6% |

-0.67% |

|

2002 |

2.1% |

11.0% |

12.7% |

-1.57% |

|

2003 |

27.5% |

7.9% |

2.2% |

0.51% |

|

2004 |

11.5% |

5.3% |

2.3% |

0.36% |

|

2005 |

3.1% |

1.7% |

0.1% |

0.71% |

|

2006 |

11.5% |

4.3% |

2.6% |

0.38% |

|

2007 |

2.9% |

5.3% |

10.4% |

-1.26% |

|

2008 |

-26.8% |

-1.8% |

-1.8% |

-1.89% |

|

2009 |

58.9% |

17.5% |

17.5% |

1.13% |

|

2010 |

15.1% |

8.9% |

8.9% |

-0.67% |

|

2011 |

5.7% |

8.5% |

8.5% |

-1.17% |

|

2012 |

16.2% |

9.9% |

9.9% |

-0.11% |

So if your belief is that rates will rise, it seems probable that high yield could outperform other fixed income asset classes, as this data shows it has historically. While no one has the crystal ball to accurately predict whether rates will go up further or stabilize at current levels, we see high yield as an attractive alternative in the current environment. Because of its lower sensitivity to interest rates than other fixed income alternatives and the seemingly attractive yield currently being offered, we believe an allocation into the high yield asset class could provide stand alone returns, as well as potential diversification benefits and risk reduction within a portfolio.

Peritus I Asset Management Disclosure:

Although information and analysis contained herein has been obtained from sources Peritus I Asset Management, LLC believes to be reliable, its accuracy and completeness cannot be guaranteed. This report is for informational purposes only. Any recommendation made in this report may not be suitable for all investors. As with all investments, investing in high yield corporate bonds and other fixed income securities involves various risks and uncertainties, as well as the potential for loss. Past performance is not an indication or guarantee of future results.

1Barclays Capital U.S. High Yield Index covers the universe of fixed rate, non-investment grade debt (source Barclays Capital). U.S. 5 Year Treasury Note is the on-the-run Treasury (source Bloomberg). Barclays Corporate Investment Grade Index consists of publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and the quality requirements (source Barclays Capital). Barclays Municipal Bond Index covers the long-term, tax-exempt bond market (source Barclays Capital). All data as of 2/8/13. The yield to worst is the lowest potential yield that can be received on a bond, without the issuer actually defaulting, and includes the various prepayment options such as call or sinking fund. The spread is the spread to worst based on the yield to worst less the yield on Treasuries. The coupon is the annual interest rate on a bond.

2Barclays Capital U.S. High Yield Index covers the universe of fixed rate, non-investment grade debt (source Barclays Capital). U.S. 5 Year Treasury Note is the on-the-run Treasury (source Bloomberg). Barclays Corporate Investment Grade Index consists of publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and the quality requirements (source Barclays Capital). Barclays Municipal Bond Index covers the long-term, tax-exempt bond market (source Barclays Capital). All data as of 2/8/13. The Modified Adjusted Duration is a measure of interest rate sensitivity based on the Yield to Maturity date.

3Acciavatti, Peter, Tony Linares, Nelson R. Jantzen, and Rahul Sharma. “2012 High Yield-Annual Review,” J.P. Morgan North American High Yield Research, December 2012, p. 26, 97.

4Acciavatti, Peter, Tony Linares, Nelson R. Jantzen, and Alisa Meyers. “2010 High Yield-Annual Review.” J.P. Morgan North American High Yield Research. December 2010, p. 105. Emphasis added.

5Data sourced from: Acciavatti, Peter, Tony Linares, and Nelson R. Jantzen. “2008 High Yield-Annual Review,” J.P. Morgan North American High Yield Research, December 2008, p. 113. “High-Yield Market Monitor,” J.P. Morgan, January 5, 2009, January 5, 2010, January 3, 2011, January 3, 2012, and January 2, 2013. 2008-2012 Treasury data sourced from Bloomberg (US Generic Govt 5 Yr). The J.P. Morgan High Yield bond index is designed to mirror the investible universe of US dollar high-yield corporate debt market, including domestic and international issues. The J.P. Morgan Investment Grade Corporate bond index represents the investment grade US dollar denominated corporate bond market, focusing on bullet maturities paying a non-zero coupon.