Pithy sound bites aren’t our forte. So when we came up with the “Twin Peaks” idea (last decade’s S&P 500 highs of 1527 and 1565) a few months back, we hoped we’d stumbled on a market theme that might last a while. That wish was dashed on March 28th, when the S&P 500 exceeded its October 2007 peak of 1565.15.

In the bull market’s earlier days, we occasionally published a “Target Practice” exercise in which various fundamental and technical S&P 500 price objectives were identified with the aim of providing shell-shocked investors (including us) something to consider above and beyond the daily fear mongering of the financial media. The techniques ran the gamut from peak Normal P/E targets to the “Lehman Collapse Vacuum” to varied “measured moves” off massive technical patterns formed as the stock market carved out a bottom in 2008-09. These were intended more to provide perspective and guidance; not the placement of sell stops (a good thing, since the S&P 500 blew past all those objectives).

-

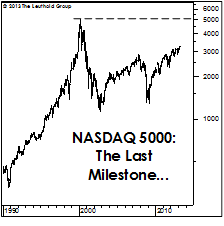

What’s left? Stronger-stomached seers will soon train their sights on the last man standing: NASDAQ 5048, reached on March 10, 2000. But at this point, we find it best to abstain from price targets, focusing instead on the macroeconomic, liquidity and technical conditions captured by the MTI—which remains bullish at 1.22.

What’s left? Stronger-stomached seers will soon train their sights on the last man standing: NASDAQ 5048, reached on March 10, 2000. But at this point, we find it best to abstain from price targets, focusing instead on the macroeconomic, liquidity and technical conditions captured by the MTI—which remains bullish at 1.22. - We can’t help it if we sound a bit reluctant. The best bull markets eventually wear out even the bulls.

What’s left? Stronger-stomached seers will soon train their sights on the last man standing: NASDAQ 5048, reached on March 10, 2000. But at this point, we find it best to abstain from price targets, focusing instead on the macroeconomic, liquidity and technical conditions captured by the MTI—which remains bullish at 1.22.

What’s left? Stronger-stomached seers will soon train their sights on the last man standing: NASDAQ 5048, reached on March 10, 2000. But at this point, we find it best to abstain from price targets, focusing instead on the macroeconomic, liquidity and technical conditions captured by the MTI—which remains bullish at 1.22. Nothing But Clear Blue Skies Ahead? We’re Not So Sure

By many measures, the U.S. market rally off the mid-November lows has been the broadest and most “egalitarian” leg of this bull market since the initial push off the great March 2009 low. The late March highs found virtually every important market measure at fresh bull market highs (and in most cases, all-time highs), including Mid Caps, Small Caps, cyclical and defensive stock composites, and every imaginable version of the advance/decline line we follow. Cyclical bull markets—even ones taking place within the context of secular bear markets—rarely peak out while exhibiting such uniform “external” and “internal” strength (measured, respectively, by cap-weighted indexes and various breadth measures). One has to look back almost 70 years - to 1946 - to find a bull market top that wasn’t foreshadowed by weakness in market breadth measures or leading cyclical market sectors. Then again, one had to look back more than 70 years to find anything to compare with the Great Recession and bear market of 2007-2009.

With the October 2007 S&P 500 peak having finally been bettered, there’s clearly no obvious technical resistance left for the U.S. stock market to encounter. Oddly enough, though, it is the fundamental strategists who’ve reacted as though there’s nothing but clear blue skies ahead for the market. I’ve heard the phrase “secular bull market” more often in the last six weeks than at any time in my market memory.

The forecasting window which forecasters are comfortable with seems to suddenly have lengthened from a few months to 3-4 years. The attending argument is that, with key cyclical areas of spending still relatively depressed (housing, business investment), the economic expansion could last for several more years. Why, they argue, shouldn’t the U.S. stock market come along for the ride?

We’re skeptical of this “long cycle” view, but not because our economic lens is any sharper than these long-term optimists’. We suspect the difference between us and this cheery camp is simply stock market valuation—specifically, the way we calculate valuations relative to much of the herd (i.e., we prefer to normalize fundamentals over the length of an average business cycle—five years).

The longest-dated and most reliable of our U.S. stock market valuation measures generally find stocks trading at historical percentile readings of 75-80%. Unfortunately, it is at precisely these types of elevated valuations which “long cycle” optimism among economists has tended to erupt. There’s no cure for this—it’s simply human nature… and perhaps a bit of peer pressure. (To have correctly exhibited such optimism four years ago was regarded as madness.)

The longest-dated and most reliable of our U.S. stock market valuation measures generally find stocks trading at historical percentile readings of 75-80%. Unfortunately, it is at precisely these types of elevated valuations which “long cycle” optimism among economists has tended to erupt. There’s no cure for this—it’s simply human nature… and perhaps a bit of peer pressure. (To have correctly exhibited such optimism four years ago was regarded as madness.)

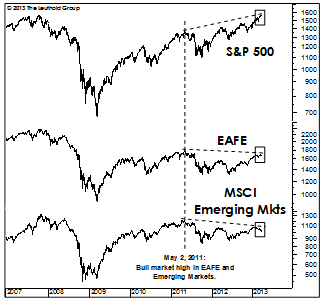

Finally, we fear the long-term bulls are basing their case on excessively “provincial” data points. For example, while the NYSE “tape” is certainly in gear, the same can’t be said for stock markets around the rest of the world. EAFE is up only 3.4% through April 4th, and the MSCI Emerging Markets Index is down 3.6%. Neither index has been able to better its May 2, 2011 bull market high, let alone their all-time highs recorded in the fall of 2007. Internally, global market action is even more fractured than at the highs of two years ago which preceded 25-30% declines in major foreign stock market indexes (but losses of only -19.4% in the S&P and -16.8% in the DJIA). These global disparities haven't been enough to drag the MTI’s “weight of the evidence” into neutral or bearish territory, but they certainly could in the weeks or months ahead.

Visit www.leutholdfunds.com for further information and research.

© The Leuthold Group 2013

© Leuthold Weeden Capital Management