Deflation Is OverPlease Come Out

A blooper reel of 20th century history would likely include a feature on Japanese soldier Hiro Onoda. Posted to a small island in the Philippines during the waning days of World War II, when Onoda’s mission proved unsuccessful he was ultimately forced to flee into the woods, where he survived on a steady diet of coconuts and bananas…for almost 30 years after the end of the war.

Why the multi-decade furlough? In keeping his word to never surrender unless instructed to do so by his superior officer, the dutiful Onoda considered every indication that the coast was clear to be nothing but Allied propaganda designed to lure him into a trap. While his commitment cannot be questioned, the poor guy ended up wasting almost three decades on an island of fruitless idealism until his superior finally let him know that it was really time to come out of the woods.

So how should one react to the newly appointed Bank of Japan (BOJ) governor’s recent attempt to draw the country’s economy out of the deflationary woods by pumping in unprecedented levels of stimulus through the end of 2014? BOJ governors past, hidebound by traditional sound-money ideals, would likely suggest that this — and similar “recovery” programs engineered by the U.S. Fed and European Central Bank — is nothing more than propaganda designed to lure Japan into a currency war that temporarily steals economic growth from other countries while doing little to end Japan’s entrenched deflationary problems, such as its aging demographics and high domestic savings rate.

Of course, it’s rumored that those who cannot learn from history are doomed to repeat it. Staying in the woods — as Japan has for the last 30 years — requires ignoring the nascent signs of real economic recovery in the U.S. that central bank activity and ingenuity engendered. For example, multiple rounds of quantitative easing and a prolonged period of low interest rates post-2008 have bought time for U.S. households to repair their balance sheets as the housing market recovers while also enabling the U.S. government to manage its large budget deficit at a low cost. Low interest rates in the U.S. have also suppressed the dollar, to the benefit of U.S. exporters and manufacturers.

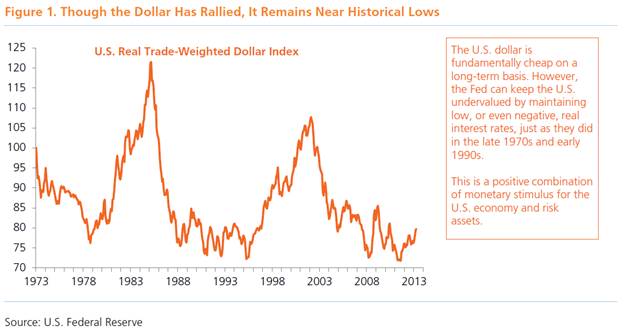

Investors have caught onto this economic recovery story, pouring money into U.S. equities in hopes of tapping into the country’s growth prospects, which are especially attractive in contrast to most of Europe and Japan. Appreciating 5% year to date, the U.S. dollar reflects this uptrend, though it remains cheap on a long-term basis in large part due to U.S. central bank activity. Of course, dollar cheapness today does not mean that a long-run bull market in the dollar is imminent; as we witnessed in the late 1970s and early 1990s, holding U.S. interest rates below the rate of inflation can keep the U.S. dollar undervalued for several years (see Figure 1). To put it another way, while the Fed plays a large role in determining the short-term value of the dollar, its long-run fortunes ultimately depend on the health of the economy and our prognosis for sustained economic rebound thanks in part to an increase in productivity.

Long-run productivity more than doubled during the 1980s and around the turn of the century — times when the dollar was cheap but showing signs of an uptrend, similar to what we are seeing today. As we discussed in the April edition of F.I.R.S.T., another such productivity revival is currently underway in the U.S., the long-term strength of which will be determined by the pace of American innovation and ingenuity rather than by a cheap currency influenced by a proactive central bank.

The transmission effects of the Fed’s bond-buying strategy that kick-started the U.S. recovery story is now being emulated by Japan, where the new BOJ governor, Hiroki Kuroda, recently announced a massive expansion of its asset-purchase program. The BOJ will buy $75 billion worth of Japanese government bonds per month until the end of 2014, nearly matching the Fed’s commitment on an absolute basis and far exceeding it relative to the countries’ respective GDPs. While Japan has not explicitly targeted its currency as part of this new monetary easing, global investors have gotten the message, aggressively pushing the yen down to the lowest levels since 2009. China, meanwhile, has stepped up its buying of U.S. Treasuries and other foreign assets in response to upward pressure on the renminbi.

To summarize, the U.S. and Japan are going to be buying $1.4 trillion worth of their own bonds over the balance of 2013, while China may scoop up another $400 billion of Treasuries. If, as some suggest, these global central bank activities represent a currency war (see the March edition of F.I.R.S.T.), then Europe stands to suffer the greatest collateral damage, as the European Central Bank cannot print money to buy its own government bonds like its counterparts in D.C. and Tokyo (see Figure 2).

It remains to be seen whether this flood of money will translate into an all-clear sign that the war against global deflationary forces is over, or if it will prove to have been central bank propaganda engineered to see who could steal the most short-term growth via a weaker currency. For now at least, central bank accommodation does not appear to be a ruse — as evidenced by the U.S. recovery story — and continues to buy time for prudent fiscal deleveraging in the U.S., for structural reform in Europe and for Japan to finally find its way out of the woods after a 30-year deflationary furlough.

In the meantime, it would be wise to heed historical precedent by not fighting the central banks. The global liquidity dynamic has never been more significant and should continue to keep interest rates grounded here and abroad for the foreseeable future. While exercising some caution in your asset allocation is appropriate should growth expectations continue to sputter and headline risks re-emerge from time to time, we expect the net effect of central bank accommodation will continue to be fruitful for equity and fixed income markets for the balance of 2013.

As global investors search for attractive currency-hedged yields, our bias is to ride the liquidity wave in favor of global credit risk — specifically domestically focused credit markets that will continue to benefit from a combination of a stronger U.S. growth picture relative to Europe and the historically cheap U.S. dollar. This includes sectors such as investment grade corporate debt, U.S. non-agency residential mortgage-backed securities and commercial mortgage-backed securities.

This commentary has been prepared by ING Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors. Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 6365