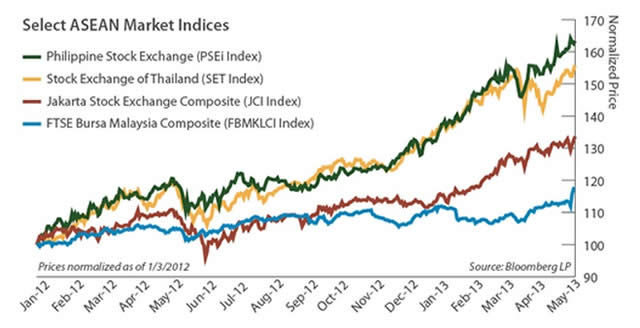

Earlier this year we identified ASEAN as the most attractive region within the emerging markets universe. That prediction has proved accurate. Market indices (USD returns) year-to-date through April in the Philippines, Thailand, and Indonesia are 23%, 22%, and 16%, respectively. Singapore (which we do not consider an emerging market) gained 6%, while Malaysia rose only 3.9%. So what’s the outlook for Malaysia?

In the United States, politics do influence economic and stock market performance, but in emerging markets the outcome of a national election often has a profound effect on a country’s investment climate and outlook. There are several recent examples. Last March, the Philippines was assigned an investment grade rating by Fitch with Standard & Poor’s following suit in late April.1 In anticipation, the Philippine peso has been strengthening versus the US dollar and the Philippine stock exchange has soared 214% since the beginning of 2012. Arguably, the most significant catalyst was the 2010 election of Benigno Aquino III as president. Aquino is the son of Filipino politician Benigno Aquino Jr. whose assassination in 1983 sparked protests that eventually led to the fall of Ferdinand Marcos. President Aquino’s election has ended a long period of incompetence and corruption at the top of Philippine politics.

Thailand has experienced multiple military coups with the most recent in 2006 when Prime Minister Thaksin Shinawatra was ousted. Several years of political instability followed, which were finally settled when Thaksin’s sister Yingluk led her party to victory in the 2011 elections and assumed the premiership. Numerous incarnations of Thaksin’s party have been dissolved and reconstituted, and every version has achieved a decisive victory at the ballot box. The Bangkok-centric political, military, and economic elite that opposed Thaksin’s movement appears to have been cowed into accepting the will of the electorate. In response, the Stock Exchange of Thailand (SET ) Index has jumped 160% (in Thai baht) since the beginning of 2012 and, at 1,601.15 on May 7th, is approaching its all-time of high of 1,789.16 THB achieved intraday nearly 20 years ago on January 4, 1994.

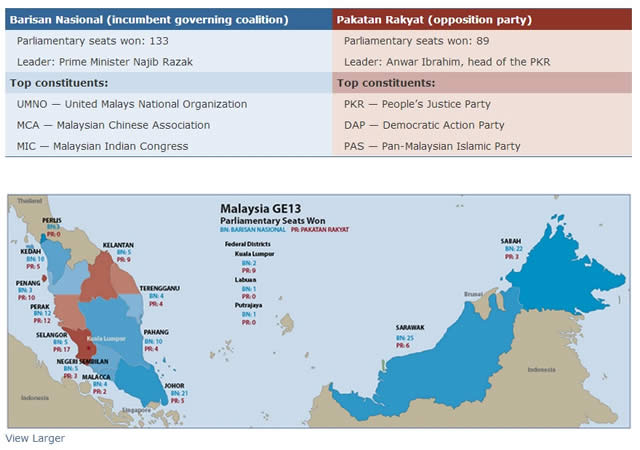

![]() What of Malaysia? The governing coalition is the Barisan Nasional (National Front), a

What of Malaysia? The governing coalition is the Barisan Nasional (National Front), a ![]() group of parties led by the United Malays National Organization (UMNO) and headed by Prime Minister Najib Razak. Just as President Aquino is the son of a politician and PM Yingluk Shinwatra is the sister of a former prime minister, PM Najib’s father was Malaysia’s second prime minister. Included in the governing coalition are the Malaysian Chinese Association (MCA) and the Malaysian Indian Congress (MIC). Ethnic identity is a significant factor in Malaysian politics.

group of parties led by the United Malays National Organization (UMNO) and headed by Prime Minister Najib Razak. Just as President Aquino is the son of a politician and PM Yingluk Shinwatra is the sister of a former prime minister, PM Najib’s father was Malaysia’s second prime minister. Included in the governing coalition are the Malaysian Chinese Association (MCA) and the Malaysian Indian Congress (MIC). Ethnic identity is a significant factor in Malaysian politics.

The opposition, Pakatan Rakyat, is an informal grouping of parties composed of the People’s Justice Party (PKR); the Democratic Action Party (DAP), an ethnic Chinese party; and the Pan-Malaysian Islamic Party (PAS). The face of the opposition is Anwar Ibrahim, leader of the PKR, as well as a former member of UMNO and deputy PM who had a falling out with the leadership.

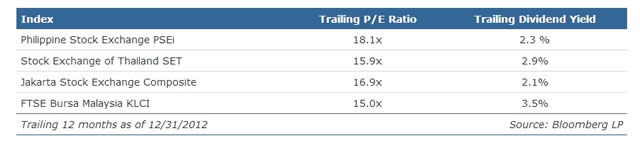

Anticipation of the elections has weighed on investors and stock market performance has lagged. From the start of 2012 through the end of April this year, the Kuala Lumpur Composite Index gained 72% — respectable, but well below the achievements of some of its ASEAN cohorts. Economically, Malaysia has performed well with GDP growth of 5.6% in 2012, while the Bank Negara forecasts GDP growth north of 5% in the current year.2 Regardless, investors have been concerned that a change in government could have significant negative consequences. Such concerns were exacerbated by polls showing a tight race. Investor relief became clear when the government victory caused the KLCI to jump 4.9% in two days, while the Malaysian ringgit strengthened 1.8% against the US dollar.

In terms of parliamentary position, the government scored a solid win, taking 133 of the 222 available seats. Still, the coalition’s overall seat count declined, and for the second consecutive time, UMNO failed to achieve a two-thirds majority in parliament. Of ![]() greater concern to the government is that while Barisan Nasional won the electoral vote, it polled only 46% of popular votes cast, with record high voter turnout above 80%.

greater concern to the government is that while Barisan Nasional won the electoral vote, it polled only 46% of popular votes cast, with record high voter turnout above 80%.

Investor relief at the government’s victory may set the stage for a market rally. Malaysia’s economic performance has been comparable to Thailand, Indonesia, and the Philippines, while, as noted above, its stock market returns have trailed (see chart at right). As a result, the FTSE Bursa Malaysia Composite Index trades at a discount to its ASEAN counterparts. As is the case in much of ASEAN, domestic investment supports economic expansion and ![]() the government’s win means that several large infrastructure projects will continue as planned.

the government’s win means that several large infrastructure projects will continue as planned.

Which isn’t to say that challenges don’t remain. Malaysia boasts most of the advantages seen in other countries around the region, including favorable demographics, growing domestic consumption, a strong agricultural sector, a solid national balance sheet, and an opportunity to drive productivity sharply higher through investments in infrastructure. That being said, identity politics have hindered the country for decades and may continue to do so. Deadly race riots in 1969 led to the establishment of the New Economic Policy (NEP), which provided preferential economic treatment to ethnic Malays, or Bumiputera (Sons of the Soil), in an effort to level the economic playing field between the Malay and Chinese communities. Over the years the NEP has been watered down but numerous preferential policies remain. These policies have undoubtedly had a deleterious effect on Malaysian economic development, although they can also fairly be claimed to have prevented renewed outbursts of violence.

Still, with the riots more than 40 years in the past, many Malaysians question the continuation of the NEP. The ethnic Chinese question it for obvious reasons, but even within the Malay community we see diminished support for the NEP among middle to upper income voters. For confirmation, we need only turn to the election results. While the Barisan Nasional promised gradual reform, the opposition vowed to scrap the remaining elements of the NEP. As a result, the government-affiliated Malaysian Chinese Association garnered so few votes that its leaders have withdrawn from![]()

![]() consideration for cabinet posts. Meanwhile the DAP saw its seats jump from 28 to 38. In areas with a greater concentration of Chinese residents (e.g., Penang, Selangor, W.P. Kuala Lumpur) the Pakatan Rakyat did very well, not only because of the contribution of seats by the DAP but also because these areas tend to be wealthier and more urbanized, where the NEP does not resonate as strongly among Malay voters. In Selangor, the state surrounding the national capital, Kuala Lumpur, the opposition won 17 of 22 seats, with the DAP and PAS each claiming four, and the Malay PKR winning nine. Conversely, in Sabah and Sarawak, the large, rural, Bumiputera- dominated states of Eastern Malaysia, the government grabbed 84% of the available seats. Finally, in the more religiously conservative northeastern states of Kelantan and Terengganu the PAS continued its strong showing, especially in the former where it easily won nine of the 14 available seats.

consideration for cabinet posts. Meanwhile the DAP saw its seats jump from 28 to 38. In areas with a greater concentration of Chinese residents (e.g., Penang, Selangor, W.P. Kuala Lumpur) the Pakatan Rakyat did very well, not only because of the contribution of seats by the DAP but also because these areas tend to be wealthier and more urbanized, where the NEP does not resonate as strongly among Malay voters. In Selangor, the state surrounding the national capital, Kuala Lumpur, the opposition won 17 of 22 seats, with the DAP and PAS each claiming four, and the Malay PKR winning nine. Conversely, in Sabah and Sarawak, the large, rural, Bumiputera- dominated states of Eastern Malaysia, the government grabbed 84% of the available seats. Finally, in the more religiously conservative northeastern states of Kelantan and Terengganu the PAS continued its strong showing, especially in the former where it easily won nine of the 14 available seats.

![]() In the wake of an election, policy differences can be magnified, and Malaysia clearly has some soul-searching ahead as it contemplates the widening ethnic and economic divide within its electorate. The effort was not helped when PM Najib called for national reconciliation at the same time he blamed a “Chinese tsunami” for the coalition’s poor showing. But one should view Malaysia in context. Unlike Thailand, it has not endured multiple coups. Unlike the Philippines and Indonesia, it has not suffered through popular uprisings that ousted long-term authoritarian leaders followed by a succession of elected leaders with varying levels of (in)competence. Today there are few countries not struggling with income inequality, ethnic strife, moribund economic activity, or debt-challenged governments. Many countries face several of these issues concurrently. When one tallies the ills affecting wide swaths of the globe, Malaysia looks quite attractive with its young and growing population,

In the wake of an election, policy differences can be magnified, and Malaysia clearly has some soul-searching ahead as it contemplates the widening ethnic and economic divide within its electorate. The effort was not helped when PM Najib called for national reconciliation at the same time he blamed a “Chinese tsunami” for the coalition’s poor showing. But one should view Malaysia in context. Unlike Thailand, it has not endured multiple coups. Unlike the Philippines and Indonesia, it has not suffered through popular uprisings that ousted long-term authoritarian leaders followed by a succession of elected leaders with varying levels of (in)competence. Today there are few countries not struggling with income inequality, ethnic strife, moribund economic activity, or debt-challenged governments. Many countries face several of these issues concurrently. When one tallies the ills affecting wide swaths of the globe, Malaysia looks quite attractive with its young and growing population,

![]() stable finances, steady economic expansion, and ready markets as it finds itself in the middle of arguably the world’s most dynamic economic region.

stable finances, steady economic expansion, and ready markets as it finds itself in the middle of arguably the world’s most dynamic economic region.

Footnotes

![]() 1 Malinao, A.“NewsAnalysis: Philippines gets second credit rating upgrade but unemployment continues to rise,” May 4, 2013. http://news.xinhuanet.com/english/

1 Malinao, A.“NewsAnalysis: Philippines gets second credit rating upgrade but unemployment continues to rise,” May 4, 2013. http://news.xinhuanet.com/english/

indepth/2013-05/04/c_132359236.htm

Important Disclaimers and Disclosures

This report is intended only for the information of the reader, and is not to be used for or considered as an offer or the solicitation of an offer to sellor buy any securities or other financial instruments of any kind, including without limitation, any mutual fund or other product offered, sponsored, created, or managed by Saturna Capital Corporation or its subsidiariesor affiliates (“Saturna”). This report is not intended for distribution to, or use by, any person or entity who is a citizen or resident of, or located in, any locality, state, country, or other jurisdiction in which such distribution, publication, availability, or use would be contrary to law or regulation or which would subject Saturna to any registration or licensing requirement within such jurisdiction.

This document should not be considered as providing investment advice or services, or any service offered by Saturna. Saturna may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the report.

Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to a particular investor’s circumstances or otherwise constitutes a personal recommendation to any investor. Saturna does not offer advice on the tax consequences of any investment.

All material presented in this report, unless specifically indicated otherwise, is under copyright to Saturna. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of Saturna. Unless otherwise indicated, all trademarks, service marks and logos used in this report are trademarks or service marks of Saturna.

The information in this report was obtained from sources Saturna believes to be reliable and Saturna believes the information and opinions in the material are accurate and complete as of the date of this material. However, information and opinions contained herein will changeover time and without notice. Saturna has no obligation to update or amend any information or opinions at any time. Saturna makes no representations as to the accuracy or completeness of this material, nor does it have any responsibility to ensure that any other materials,

including any containing materially different information, are brought to the attention of any recipient of this report.

![]() Under no circumstances shall Saturna, its employees, or any affiliate, be responsible for any investment decision by any recipient. This material is distributed on condition that it will not form the sole basis or a sufficient basis for any investment decision by any recipient. Any recipient who is not a market professional or institutional investor should seek the advice of an independent financial adviser prior to taking any investment based on this report or for any necessary explanation of its contents.

Under no circumstances shall Saturna, its employees, or any affiliate, be responsible for any investment decision by any recipient. This material is distributed on condition that it will not form the sole basis or a sufficient basis for any investment decision by any recipient. Any recipient who is not a market professional or institutional investor should seek the advice of an independent financial adviser prior to taking any investment based on this report or for any necessary explanation of its contents.

Saturna does not provide tax, legal or accounting advice. Investors should consult their own tax, legal and accounting advisers before engaging in any transaction. In compliance with IRS requirements, recipients are notified that any discussion of U.S. federal tax issues contained or referred to herein is not intended or written to be used for the purpose of (A) avoiding penalties that may be imposed under the Internal Revenue Code; nor (B) promoting, marketing or recommending to another party any transaction or matter discussed herein.

The FTSE Bursa Malaysia Kuala Lumpur Composite Index (FBMKLCI) is an index composed of the 30 largest companies, measured by full market capitalization, on the Bursa Malaysia (the Malaysian stock exchange). The Jakarta Composite Index (JCI) is a capitalization-weighted indexof all stocks listed on the Indonesia Stock Exchange. The PhilippineStock Exchange Index (PSEi) is a capitalization-weighted index of stocks on Philippine Stock Exchange, representing the industrial, properties, services, holding firms, financial, and mining and oil sectors. The Stock Exchange of Thailand Index (SET) is a capitalization-weighted index of stocks traded on the Stock Exchange of Thailand. All indices shown are widely recognized unmanaged indices of common stock prices which reflect no deductions for fees, expenses or taxes. Investors can not invest directly in the indices.

Past performance does not imply or guarantee future performance, and no representation or warranty, express or implied, is made regarding future performance. The price, and value of, and income from, any of the securities or financial instruments mentioned inthis report can fall as well as rise. The value of foreign securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Investors in securities such as ADRs – the values of which are influenced by currency volatility – effectively assume this risk.

© Saturna Capital