The following is a research study that provides compelling data on a more efficient way to invest in broad markets. Many people have called the equity market of the last 10 years the “lost decade” due to its lack of net change. Madrona Funds research shows that it would have been possible to have profited by over 200% over the last decade by using their forward looking methodology, which is based on future expected earnings, not past performance.

PREFACE

It has been 35 years since the first broad market index funds were introduced to investors. At the time, they were a cutting edge strategy for core equity allocation to investment portfolio’s. Prior to index funds, investors were unable to purchase broad baskets of equities due to the high trading costs associated with individual stock selection strategies. However, these index strategies were never designed for the purpose of selecting the most undervalued equities within the market.

The following is a Madrona Funds research study that provides compelling data on a more efficient way to invest in broad markets. Many people have called the equity market of the last 10 years the “lost decade” due to its lack of net change.

In this paper, we will:

- Provide Investment Advisors with a unique value-add proposition for their broad market equity investment allocation.

- Challenge the notion that we should blindly place our faith in overweighting mega-cap companies, following the “herd mentality” and buying stocks at the peak of a run-up.

- Challenge the notion of allocating our investments based upon a single component of a statement of income or a balance sheet.

- Challenge the practice of allocating investment dollars based upon historical measures without regard to the value of the underlying equities.

In our experience, most successful investment advisors would not suggest that individual stock selection should be done using any of the methodologies currently used in broad-market index strategies. Investment advisors would instead work to find indications of future company-by-company performance relative to the current price paid for a given equity. Up to this point, there has never been a strategy for investing in a broad basket of equities using the same methodology of valuation that we use for individual investment selections. In the pages that follow, we offer a common-sense approach challenging the current state of broad market equity indices. It is our hope that this paper will equip advisors to change how they (or their clients) will invest in the core equity markets.

OVERVIEW OF BROAD-MARKET INVESTING

Before embarking on the specifics of the study, it is important to summarize some of the current broad-market or index strategies currently available to investors.

Managed Mutual Funds – Prior to the index option, mutual funds were the first products to allow individual investors access to the broad markets. There are good fund managers, especially among particular sectors. There can also be a case made for mutual funds when an investor is seeking to overweight a particular area of the market. However, when it comes to broad market investing, mutual funds have had limited success as a whole when compared to their indexed counterparts. In a 2009 Morningstar report titled, The Morningstar Box Score Report, the conclusion was that “After accounting for risk, size, and style, only 37% of active funds beat the respective Morningstar Style Index over the past three years”. When it came to the Large Cap Core style box, less than 23% of managed mutual funds outperformed their respective Morningstar Style Index for the 5-year period ended June 30, 2009.

Index Funds

Market-Capitalization Weighted Index – This is the oldest and most widely used of all indices, and perhaps the least logical of all index methodologies. In relation to the above mentioned Morningstar study that indicated how broad-market indexing is typically better than using managed mutual funds, let us examine the market-capitalization methodology.

This methodology relies overwhelmingly on one factor to determine its allocation to equities: size. There are many flaws in market-capitalization index investing, including the assumptions that:

- A mega-cap stock is always a better investment option than any mid-cap stock.

- It is desirable to allocate more than 60% of your total investment in the first quartile of the 500 largest U.S. companies. Similarly, it makes sense to only allocate less than 40% of your total investment to the next three quartiles combined.

- It is better to buy more of a given company in an index after it increases in value and sell it after the price drops.

- It is better to make the largest allocation to overvalued sectors and conversely, divest the highly profitable, but unpopular sectors. For example, in February 2000, the technology and telecommunications sectors represented more than 50% of the total value of the entire equity market. At that point in time, these sectors were arguably the most overvalued sectors in the modern history of the stock market, and market-capitalization weighted investors were heavily weighted in these sectors.

- No equities within the population of the index should be excluded. The option to have any active management should be eliminated.

These equity indices suffer a built-in bias to buy equities when overvalued and sell them when undervalued without focusing on valuation. Early in their history, market-capitalization indices had an important role in allowing the common investor access to the markets, but their usefulness as a “best-practices” strategy for widely traded broad-market investing has, in our opinion, become outdated.

Dividend or Revenue-Weighted Index – Due to the built-in flaw of using market-capitalization weights, new products arrived using other simple measures to allocate investments by using dividends paid or revenues earned. In many cases, these measures are an improvement on the market-capitalization method simply because they have less built-in bias to buy equities when they are high and sell them when they are low. The problem with these methodologies is that they replace one bias with another, neither of which is concentrated on valuation.

With dividend weighting, the bias is toward any sector with historically high payouts, such as established banks, utilities, pharmaceuticals and real estate. By their very nature, dividend weighted indices shy away from companies investing in growth and new market agendas. Additionally, if one were to look at the top holdings of such an index, it looks like a replication of the top holdings of market-capitalization indices. The highest allocation is not to the companies that are paying the highest percentage dividends. Rather, it is to the companies with the highest total dollars of dividends paid. Hence, these indices have a dramatic overweight to the mega-cap equities.

Similarly, revenue weighting is designed to invest based upon a single line item of a statement of revenues and expenses. Like the previously discussed index methodologies, it virtually ignores costs of revenue and has no valuation analysis. A review of the top holdings reveals a common theme of dramatic overweighting of mega-cap companies. The reason? This methodology is not based upon revenue relative to market value, but is instead based upon the company’s total gross revenue.

Equal Weighted Index – There are now broad market investment options of simply purchasing equal percentages of all stocks within an index. This has the desired effect of eliminating the built-in bias towards mega-cap stocks present in the other index strategies. A review of the one-, three- and five-year returns indicates that this method outperforms when compared to the aforementioned strategies.

The financial community can now access vast amounts of company data on the Internet. We have access to the most widely followed equity research companies in the world. However, the best solution of the above methodologies essentially concludes that, “We don’t have any idea which companies make the best investment, so let’s just make an equal investment in all of them.”

Historical-Based Fundamental Index – We think this methodology was a step in the direction of providing a proper broad-market vehicle to the investment community. Investment allocations in these indices are based on a combination of historical accounting measures such as historical net cash flow, accounting book value, dividends paid, revenues and historical return on assets. While this represents some progress, it is also steeped in flaws. First, there is still the bias towards overweighting mega-cap companies that is prevalent in most index strategies. Again, this is due to the fact that the historical accounting figures are taken in gross rather than on a percentage basis. There is also no real valuation analysis done on a company-by-company basis. As with the other index methodologies, an investor would not likely use this method when analyzing an individual equity for purchase or sale, so why build an entire broad-market index and select equities based on this approach?

HOW ARE COMPANIES VALUED?

The following is taken from “Understanding Business Valuation”, an American Institute of Certified Public Accountants (AICPA) publication, copyright 2010.

The principle of future benefits states that “economic value reflects anticipated future benefits.” This appraisal principle can best be illustrated by assuming that you want to buy a particular business. Would historic earnings be as important as prospective earnings in determining value? Probably not. You would not care what the business did for the prior owner as much as what it can do for you, the purchaser.

It should always be remembered that valuation is based on the future outlook of the business. If you really stop to think about it, this is the foundation for making a financial investment. The bottom line is that regardless of how you go about it, economic value should be determined based on the anticipated future cash flow that is expected for an investment. It is virtually unheard of for a comprehensive business valuation to conclude that the ultimate value of a business is based solely on revenue, size of the company, dividends paid or balance sheet items. Companies are in business to earn a profit.

HOW TO DETERMINE PRESENT VALUE OF FUTURE EXPECTED NET PROFITS

There are hundreds of data points used in determining the expectation of profits by analysts. There are also dozens of very reputable firms covering all the primary companies comprising the major indices.

While analysts do look at historical measures, they also look at issues such as competition, sector direction, global events, commodity prices, demographic trends, legislative changes, capital investment, product trends, tax legislation, etc. These analysts take into account all available information to calculate expected net profits and the growth of profits for the foreseeable future.

Prior to the proliferation of the Internet, calculations of expected profits were basically kept in the “secret vaults” of the companies doing the research. But today, we can produce a report using the Madrona Forward Valuation Model to determine the present value of future expected net profits of well over 500 equities on a company-by-company basis. No analyst is perfect, which is why it is important to use the consensus of all qualified estimates available. Once this information is obtained, we can then compute our ultimate goal.

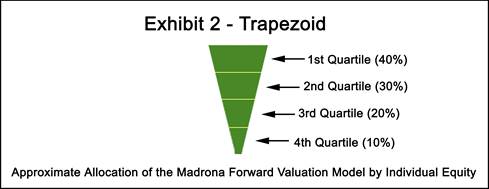

The Madrona Forward Valuation Model essentially begins by computing the projected net profits for all of the 500 largest U.S. companies, while factoring the projected growth of these profits as provided by the leading research companies in the country. Once we have these figures, we put all 500 companies in order from the highest projected profit per dollar invested, down to the lowest. Next, we eliminate companies which have no projected profits or have decreasing projected profits. Finally, we then allocate the percentage invested to each company based upon the “trapezoid” as discussed later and shown in Exhibit 2.

THE PRESENT VALUE OF FUTURE EXPECTED NET PROFITS RELATIVE TO WHAT WE ARE PAYING FOR THESE PROFITS

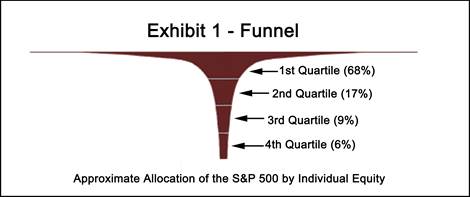

The Funnel

In the case of market-capitalization weighted indices, the S&P 500 looks much like a funnel due to the overweight of the mega-cap stocks. As previously mentioned, when using an index with a market-capitalization bias, more than 60% of the dollars are allocated to only one quartile of holdings. A recent snapshot of the index indicates the great disparity between investments in the largest and smallest companies within the index. For every $1 million invested, more than $38,000 would be invested in the largest holding and less than $100 in the smallest holding. To gain perspective of this issue, the following graph, Exhibit 1, was prepared using 2010 market capitalization data of the largest 500 U.S. companies.

The Trapezoid

Since this is a paper on broad-market diversification, it is appropriate to design a system of allocation consistent with this goal. It is our assessment that any broad-market investment strategy should, at a minimum, have a material investment allocation to all of the equities in the population. For purposes of our research, we decided to allocate 40% to the first quartile, and 30%, 20% and 10% respectively to the next three quartiles. Our “common sense” version of this is best summarized by the trapezoid graph in Exhibit 2.

THE RESULTS OF THE STUDY

As we mentioned previously, gathering the data necessary to perform comprehensive company-by-company valuations of the broad market was virtually impossible before the proliferation of the Internet. Thanks to technology, we are able to look back in time to determine what the analyst estimates were at prior dates. We were able to test our strategy by determining what the baskets of stocks would have been at prior dates and how they performed after adjusting for stock splits. In addition, we were able to rebalance our basket on a quarterly basis.

As we were performing our study, we were able to put the equities in order based on valuation. However, there were always a number of equities that could not be ranked due to a lack of projected profits, and/or a loss of market share that created a negative growth rate of earnings for all future years in our projection model. We decided to exclude these equities from our investment model. Excluding equities is not something that is allowed when “indexing”. However, this is not a paper on indexing—rather, it is a paper on the best way to invest in the broad market.

To summarize, we were able to collect the analysts’ consensus present value of future expected profits relative to stock prices on a quarter-by-quarter basis for the prior 44 quarters. Once we converted this data into our valuation matrix, we were then able to put these equities in the proper order and eliminate equities that did not meet our valuation criteria. The total return is calculated using split-adjusted close prices, plus any dividends reinvested on the ex-date.

CONCLUSION

Broad market asset allocation is a cornerstone to building an equity-based asset allocation plan. There are many methodologies of indices available on the market. A case can be made that each of these methods contains serious flaws. Up to this point in time, no method of allocation within an index has applied the same methodology most investors would use when choosing to invest in an individual equity.

The most important and widely used valuation measure used by CPAs and valuation specialists is the determination of the present value of future expected net profits.

With the exception of equal weight indices, index funds commonly allocate most of the investment dollars to a fraction of the total holdings within the index. Broad-market strategies should not virtually eliminate holdings that have smaller market capitalization. Rather, broad market investing should instead allocate a material investment percentage to all quartiles of the equities selected.

Unlike an index, an active management strategy can allow for the elimination of investments from equities that do not meet the criteria of the manager. The elimination of investments in these unqualified companies can have a positive effect on the return of an investment portfolio over time.

Major equity indices currently have a high degree of correlation to one another, making it difficult to build asset allocation models that can significantly outperform the market indices. However, there are always undervalued and overvalued equities in all markets, at all times. Valuation does matter and vast amounts of information on valuation is available via the Internet. We believe investors seeking to outperform indices should be seeking a broad market product that invests in the proper way: The present value of future expected profits relative to the price of those profits.

© AdvisorShares