Equities Slip From Record Highs

Stocks fell for the first time in five weeks, as markets eased from record highs. Investors were troubled by indications from the Federal Reserve that its quantitative easing program was nearing an end. The S&P 500 lost 1.1%, while the Dow Jones Industrial Average declined 0.3%.

On Wednesday, Chairman Ben Bernanke made remarks that the Fed could potentially reduce the scope of its quantitative easing program before Labor Day, reversing a rally that had persisted through the first half of the week. Later in the day, the decline deepened following the release of minutes from the Fed’s April 30-May 1 FOMC meeting. Transcripts from the meeting suggested that Fed officials were becoming increasingly concerned about market participants’ dependence on asset purchases.

In a limited week of economic data, a handful of housing metrics revealed a sector of the economy that continues to progress.

Existing home sales bounced back following a modest dip in March, rising to a seasonally adjusted annual rate of 4.97 million in April. This is the fastest pace since November 2009, which occurred in the midst of the government’s homebuyer tax credit. More encouragingly, this month’s figure was driven by robust growth in single-family unit sales. Single-family home sales are a far more reliable measure of the health of the housing market, as multi-family unit sales tend to be much more volatile.

The level of distressed home sales continued to contract, as sales of foreclosures and short sales fell to 18% of transactions in April. This was reflected in transaction prices, which continue to improve. The median national price for existing home sales was $192,800, 11% higher than 12 months prior. According to the National Association of Realtors, which composes the report, this is the first streak of 14 consecutive months of year-over-year price increases since April 2005 to May 2006.

More good news on the housing front came in the form of new home sales. The measure increased to a seasonally adjusted annual rate of 454,000 sales, well above the consensus estimate of 425,000. While the month-over-month increase was only 2.3%, April’s increase was diluted by a strong upward revision in March – from 417,000 to 444,000. February was also revised higher by 18,000 sales.

Similar to the existing home series, prices continue to climb sharply. The median sales price for new homes in April was $271,600. This was 8.3% higher than just one month prior, and represents a record high level for the series. Supply remains tight at 4.1 months, contributing to the price increase.

The other significant release of the week was durable goods orders, which rebounded from a very poor March. New orders rose 3.3% during the month, which followed a 5.9% contraction in March. The less volatile core measure, which strips out the transportation component, increased 1.3% following a 1.7% decline.

As we have noted before, durable goods is a notoriously volatile measure, making any month-to-month inferences difficult. On a year-over-year basis, however, durable goods have slowly trended down over the past few years, and is currently bumping close to flat levels. This slowdown mirrors softness in other manufacturing readings such as the ISM and regional Fed surveys. The sector’s sensitivity to non-US economic weakness appears to be filtering through to a number of metrics.

Is the Fed in the home stretch?

Global equity markets stammered through a choppy environment last week following increased fears that certain central banks were considering the possibility of pulling stimulus sooner than anticipated. Markets have long been dependent on central banks, but the notion that policymakers could head for the exits leaves investors unsure how to react.

While it has been a long time in the works, markets were rattled when Fed Chairman Ben Bernanke testified before Congress recently. Treasury markets sold off quickly after Bernanke said the Fed could reduce its bond-buying program in the “next few meetings.” The comment was intriguing, but largely old news. Several Fed officials openly discussed the possibility of “tapering” purchases through year-end.

Perhaps most interesting is that tapering is simply a way for the central bank to wean market participants off much-desired stimulus, rather than yanking it all away at once. If tapering did occur and the Fed went from $85 billion a month in asset purchases to $65 billion per month, the Fed would still cross $3.5 trillion of securities on its balance sheet by the end of the year. Such changes are hardly going to break the market at this point.

Source: SoberLook

The problem could lie in a mismatch between expected policy and actual policy. According to the Wall Street Journal, a recent survey from the Federal Reserve Bank of New York showed that most market participants thought purchases would continue unchanged through year-end before the program ends in the second quarter of 2014. Treasury markets quickly reacted to Bernanke’s comments, with yields moving higher by 8-10 basis points from the five through 30-year portion of the curve.

Source: Econoday

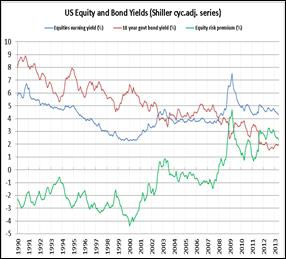

As the Fed’s policies have driven down interest rates, investors are gradually being forced out of bonds and into other assets. This raises the specter of bubbles forming, but so far, that does not seem to be the case. Government bond yields are down considerably in the past several years, but the yield on equities has been stable since the crisis.

Source: FT Alphaville

The Federal Reserve is in a delicate position, attempting to manage market expectations as it steps away from asset purchases. There will be periods of volatility as the Fed backs away and investors would be well served to pay close attention to every word coming from Fed officials in the months ahead.

The Week Ahead

Economic data picks back up this week, with important readings on GDP and personal spending. The Case-Shiller Home Price index is also due on Tuesday morning.

Central banks meeting this week include Israel, Hungary, Brazil, Thailand, Canada, and Colombia. Hungary and Thailand are expected to cut rates, while Brazil is forecasted to raise its overnight SELIC rate.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

For more information, please visit our website at http://www.Fortigent.com.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent