Overview

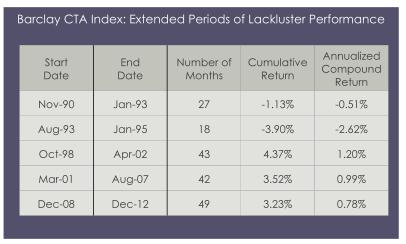

Many investors have begun to question the efficacy of an investment in managed futures given the most recent two years of negative performance for the industry as a whole at a time when U.S. equity prices have been achieving multi‐year highs. The concern is not so much the magnitude of the losses incurred by the managed futures industry during this period; in many cases they are relatively small in comparison to the size of the drawdowns experienced by many other asset classes such as equities, real estate, fixed income, etc., during peak periods of market stress. Rather, the question is spurred by the length of the drawdown and the lackluster to negative returns that have accumulated since 2008. Historically, there have been other such periods when performance has been essentially flat or slightly down; the most notable of which are summarized in the table below:

The real question is whether or not the dramatic economic events of the past two years and a very low interest rate environment resulted in a systemic change in how markets behave which, in turn, could adversely impact managed futures returns in the future.

Given our over forty years of experience in all phases of the managed futures industry, we believe the market events and the performance of managed futures over the past several years are an aberration. While myriad market shocks have significantly impacted market behavior and, as a result, managed futures returns, we cannot identify any systemic change that would prevent markets from responding to the long‐term forces of supply and demand and producing trends upon which the managed futures industry has historically profited. Quite the contrary, we believe that the events of the past several years have set the stage for some significant opportunities in managed futures.

The Challenges for Managed Futures Investing in 2011 and 2012

The amount of economic uncertainty and the numerous threats to economic stability in the U.S., Europe and emerging nations over the past two years has been unprecedented. If these issues had not been addressed by the world’s leaders and central bankers, the likely outcome could have been the economic collapse of Europe and a global economic recession or, in the extreme, a depression. Given the severity of the situation, the numerous and far‐reaching economic policies and interventions that have been announced over the past two years have had significant market impact. At times, the news was perceived as being “good” and markets rallied or the news was thought to have inadequately addressed the problem of that particular day and markets declined. It was either “risk‐on” or “risk‐off.” In many cases, there appeared to be no continuum from one day or month to the next. Markets often responded to the current news of the day without regard to long‐term, fundamental economic issues. The end result of this type of market behavior included periods of high correlations among many disparate and unrelated markets, significant increases in non‐directional volatility, i.e., choppiness, and the disruption of what few market trends existed. These factors made trading conditions very difficult for the vast majority of the strategies employed by managed futures advisors.

Historically, the source of returns produced by managed futures advisors has come from capturing major changes in prices, i.e., trends. As a result, most managed futures advisors employ some type of methodology to participate in these trends, whether their strategy is mathematically based or determined by the economic fundamentals of supply and demand, coupled with stringent control of risk. There have been a few sustained trends over the past several years, most notably the decline in interest rates, but the profits generated by these price moves have been more than offset by losses incurred in many markets in which trends were absent. Moreover, many price changes, which in retrospect might have qualified as trends, were very difficult to trade. The extreme non‐directional volatility within some of these price movements made it very hard for most strategies to capture these opportunities and still control risk and volatility.

Has There Been a Systematic Change in Market Behavior Patterns?

Opportunities in most of the markets traded in managed futures portfolios are created by the cyclical nature of free markets, whether they are financially related or the traditional raw agricultural and industrial commodity markets. In the financial complex, markets are impacted by changes in economic policies which in turn influence equity prices, fixed income values, foreign exchange rates and international asset flows. Once these policies are set in place, the price reaction usually unfolds gradually over a period of time. In the commodity sector, this price cyclicality is based on the laws of supply and demand. As demand increases or supply is reduced, prices rise. High prices then curtail demand and encourage production which cause prices to decline. This cyclicality which is evident in both the financial and commodity markets was interrupted many times over the past several years as the magnitude of the global economic problem and its potential outcome had the ability to turn shortage into surplus and surplus into an even greater surplus and vice‐versa.

In our view, the magnitude, both in terms of number and significance, of the market events and dislocations over the past two years created a market environment and price behavior patterns that were highly unusual from a historical perspective and not likely to persist for a sustained period of time. Much has changed over the past two years. Major economic stimulus programs have been undertaken in the U.S., China, India, Japan and Brazil. The Chinese economy is growing again. The European Central Bank and European leaders have taken dramatic steps to restore confidence in the Euro. The U.S. avoided the dreaded “fiscal cliff” and the U.S. economy continues to recover. All of these events have resulted in growing confidence by investors that some semblance of economic stability has returned and that the risks and magnitude of potential market shocks have been significantly reduced.

Some major uncertainties still exist, however, such as the looming U.S. debt ceiling and budget negotiations, problems emanating out of Europe as the solidification of the financial and banking systems move forward and the unrest in the mid‐East. However, the severity of these factors is far less than markets have had to cope with over the past few years or, as is the case in the mid‐East, factors that the markets have dealt with for many years.

Without the disruptive effect of new “headline” risk and the resulting fear and uncertainty that have plagued the markets, we envision a return to more normal and rational market conditions and price behavior that responds to the economics of supply and demand as they impact individual markets. We believe the question is not “if” market conditions return to normal, but only “when.”

The Opportunities: Where Are the Trends Likely?

One of the great attractions of futures trading is the ability to take advantage of both bull and bear markets because it is just as easy to sell short as it is to buy long. The vast majority of managed futures strategies are agnostic as to whether the price goes up or down; their Achilles heel is sideways price movements, i.e., non‐directional volatility. As we look to 2013 and beyond, two scenarios exist. While each scenario is quite different from the other, each is conducive to the development of some sustained trends, both in the financially related markets and in the traditional commodity markets.

We believe that the world will embark upon a period of sustained, economic growth, but the rate of that growth and the degree of investor confidence in the world’s economic structure and stability will determine the impact on the marketplace. If confidence returns (and the recent new all‐time highs in the Dow Jones Industrial Index suggests that it may have) and the rate of growth steadily increases, we can envision a scenario in which the stalled bull markets in many commodities would resume and potentially profitable opportunities could arise in the financial markets.

Specifically, increased demand for corn and soybeans coupled with extremely low inventories could set the stage for much higher prices, particularly given the drought conditions that persist in the U.S. The vagaries of Mother Nature, which seem to have become more severe in the past several years, could turn surplus into shortage in a number of other agricultural markets such as coffee, sugar, cotton and, in particular, wheat given the recent bout of extreme heat in Australia. Growing infrastructure needs in China, Brazil, India and other emerging economies will likely put pressure on prices of many industrial commodities, such as copper and lumber. Improved economic activity would also boost the demand for energy. In the financial complex, the large amount of monetary reserves added to the world‐wide banking system over the past several years have long‐term inflationary ramifications which could benefit gold and silver prices, aided over the short run by extremely low interest rates. The interest rate cycle can also be expected to change as the improved economic activity will eventually lead to higher interest rates and a stronger U.S. dollar. Finally, a growing world economy would be expected to be bullish for world‐wide equity prices. All in all, we envision the potential for some normal price trends to develop which have historically provided the potential for significant profit opportunity in managed futures.

On the other hand, there is another scenario in which the world’s economies recover, but do so very slowly, and Mother Nature brings forth ideal growing conditions with no earthquakes, hurricanes, tsunamis or other catastrophic events. If that were to happen, once the initial euphoria that the crisis is over and that risks have normalized ends, many markets are going to be void of incentive. The upward trend in equity prices could stall; interest rates could be confined to a narrow range, but still low; foreign exchange prices could be choppy depending upon which country is doing better at the moment than the other. In the commodity sector, the relatively high prices, in many cases significantly above the cost of production, which most commodities have attained in the past several years will undoubtedly spur increased production and could lead to lower prices for many agricultural commodities. The industrial commodities may also not be immune to some downward pressure. For example, the increase in copper production which is projected to result in a global surplus this year after three years of supply/demand deficits could exacerbate the impact of a very slow economic recovery and China’s effort to curtail what some would call a “housing bubble.” In this rather deflationary scenario, prices for many commodities could drop sharply while the financial markets might be in essence stagnant.

While there are at least two very different scenarios with two diametrically opposite results, the opportunities that each present for managed futures advisors are in many respects equal. While there is certainly more profit that can be made in a bull market as the “sky is the limit” versus a bear market in which the opportunity is limited by the cost of production, there remains considerable opportunity for profit in both scenarios. More importantly, should the “slow growth” scenario come to pass and prices decline in the interim, the “broad recovery scenario” would eventually come into play, providing further opportunities.

In our opinion, whether markets go up or down is immaterial. What is important now, however, is that with the absence of world‐altering events, markets can get back to responding to the forces of supply and demand as they unfold and trend accordingly. In the final analysis, we envision some normal price trends to develop, the nature of which will potentially provide for significant profit opportunity in managed futures.

The Risk of Timing Managed Futures Investments

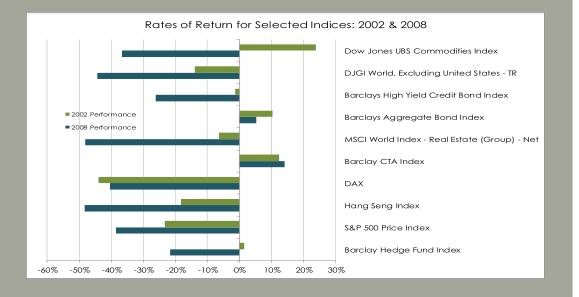

Prior to 2008 (and even after the market downturn of 2000/2002), despite proven and significant benefits that an investment in managed futures would bring to a traditional investment portfolio in terms of return, lack of correlation and reduction in volatility, not many investors included managed futures in their investment portfolios. In essence, why invest in managed futures when other investment mediums had performed very well from 2003 to 2006 and were expected to continue to do so? In 2008, a multitude of adverse world‐wide events, the depth and scope of which was not in the historical lexicon of investing, conspired to cause equity prices to stage one of the biggest declines in history with the S&P 500 Price Index down over 35% for the year. Emerging markets plummeted; credit markets dried up; and real estate suffered one of the biggest declines in history. Confidence in all investment sectors eroded dramatically and virtually no investment was left unscathed as most all investment strategies became very highly correlated. The only exception, of course, was managed futures which posted on average double digit returns, some in the 15% ‐ 25% range. The absolute return and diversification benefits of managed futures were now proven beyond a shadow of a doubt and we would think that those who did n0t have managed futures in their portfolios in 2002 or 2008 wished they had.

Very few investors had the foresight to anticipate what would happen in 2008 and it is virtually impossible to anticipate with any certainty what the next few years will bring. Although our managed futures experience spans over 40 years, we have yet to figure out how to effectively “time” an investment in managed futures. Moreover, history has shown that the timing of any investment is fraught with pitfalls. That being said, there are several aspects of a managed futures investment that we believe argue against timing.

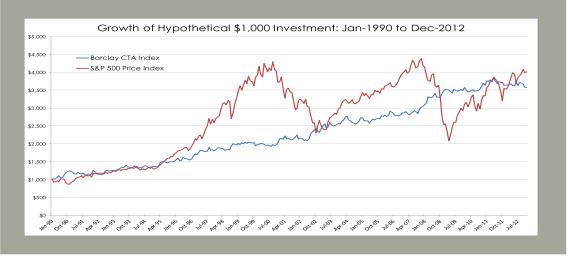

- Based upon the Barclay CTA Index, the industry has produced positive absolute returns over a long period of time with less risk than most other asset classes making it valuable as a long‐ term, stand‐alone investment.

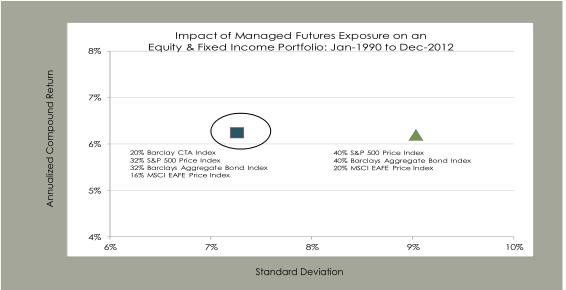

22% while providing a slightly higher overall rate of return.

- The lack of correlation of managed futures (as represented by the Barclay CTA Index) relative to more traditional investment mediums such as the S&P 500 Price Index (‐.11) and the Barclays Aggregate Bond Index (.17) makes managed futures a valuable strategic allocation within a diversified investment portfolio, reducing both volatility and risk. For example, during the period from 1990 through 2012, adding a 20% allocation of managed futures to an equity/bond portfolio as outlined in the chart below reduced the volatility or risk of the portfolio as measured by the standard deviation by almost 20% and increased the Sharpe Ratio by almost

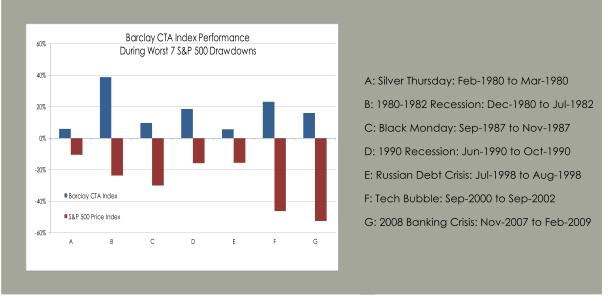

- Managed futures investments have generated positive performance during the large number of peak periods of stress in the equity markets such as that produced by the Russian Debt Crisis, the Long Term Capital debacle, the Crash of 1987, the Tech Bubble in early 2000 and, of course, the Recession of 2008, just to name a few.

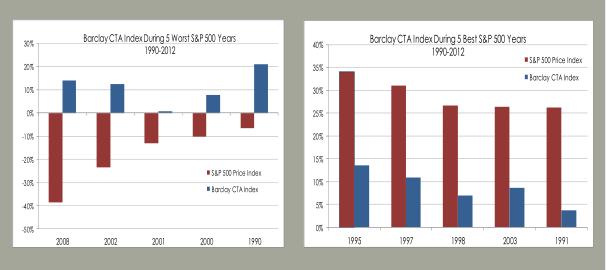

- Moreover, while managed futures produced positive returns during the five worst years for the S&P 500 Price Index from 1990 through 2012, managed futures also produced positive returns in each of the five best performing years of the S&P 500 Price Index during that period. This further demonstrates the lack of correlation of managed futures to more traditional investments.

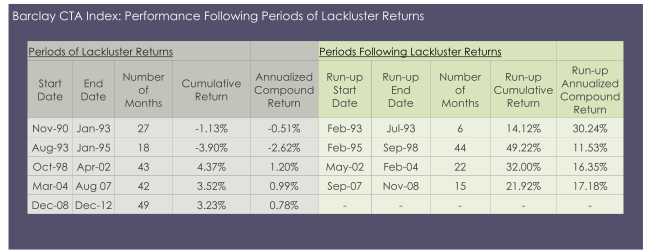

- Managed futures returns are not linear or consistent, but are rather lumpy, often occurring in clusters, and most importantly, very unpredictable. Periods of poor or mediocre returns are often followed by periods of relative out‐performance and vice‐versa as markets respond to the changes in the fundamental economics of supply and demand.

Benefiting from Managed Futures

Historically, many investors jump on the bandwagon when performance is strong instead of following the old adage of “buying low and selling high.” We believe that managed futures will continue to provide the correlation, volatility and return benefits and would view the current drawdown as an opportunity to initiate or add to a managed futures investment. The proven benefits of adding and maintaining exposure to managed futures in an investment portfolio are very compelling. It is our opinion that those investors who remain committed to managed futures will reap those benefits through many market cycles yet to come.

© 6800 Capital