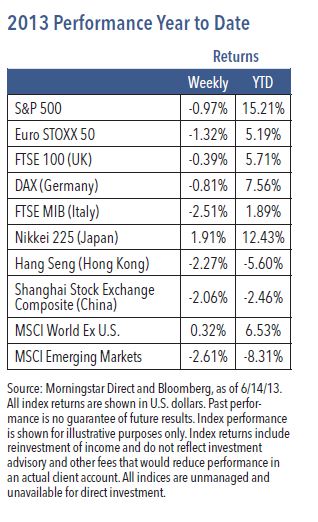

Last week the S&P 500 declined 0.97%,1 while many global equity averages fell for the fourth week in a row. Early in the week, discussion of tapering by the Federal Reserve was a big headwind, as discomfort over a slower pace of policy accommodationrippled through global markets. Thursday’s rally was driven by thoughts that tapering fears may beoverdone. Markets were also helped by better employment and consumption data.

Mixed Signals

Two weeks ago, we mentioned that the market seemed due for a rest. We cited the potential for a 7 to 10% correction for the S&P 500 to approximately 1550, or a consolidation in the 1600s, both more likely than continued strong markets with new record highs before July 4. In our view, the upcoming decision to taper Fed pur- chases as a result of stronger real growth should be seen as a welcome and necessary step toward recovery, rather than something to be feared.

The sell-off in bonds over the last month may have reached a short-term pause. Real yields are positive for the first time in almost two years,2 while inflation expectations continue to fall. U.S. fundamentals remain mixed, with steady labor markets in May despite the drag from sequestration and global economic softness. The underlying U.S. story remains positive — a combination of the wealth effect, strong corporate balance sheets and pent-up demand as measured by aging capital stock.

Weekly Top Themes

- Retail sales increased 0.6% in May, which was slightly better than expected:3 Consumer metrics look reasonably healthy, as spending growth has been modest but steady, even while fiscal headwinds challenged house- hold incomes.

- The average inflation in advanced economies fell to only 1.3% in April, the lowest rate since 2009:4 With the recent decline in commodity prices, further inflation declines could happen.

- Rising equity prices and housing price gains raised the value of household assets to a record high in the first quarter:5 Through the wealth effect, rising equity and house prices have kept consumption reasonably strong.

- The federal budget deficit decline prompted S&P to upgrade its outlook for U.S. debt:6 Complacency in Washington, D.C. may have closed the window for significant entitlement reform, making the task more difficult to address later this decade.

The Big Picture

The recent equity sell-off was likely triggered by Fed dialogue about an earlier slowing of its large-scale asset purchases. All eyes are now on this week’s FOMC meeting and Fed Chairman Ben Bernanke’s press conference. Our guess is that Bernanke will try to avoid committing to the timing of tapering, emphasizing that the decision remains dependent on data, and tapering is not the same as hiking interest rates. It is possible the Fed will lower its growth and inflation forecast. The Fed’s trial balloon about a potential reduction in quantitative easing has many challenges.

Inflection points in monetary policy often have the potential to trigger a rise in financial market volatility. This exists today, especially with fixed income prices distorted by Fed policy. Rising U.S. Treasury yields should not have a lasting impact on the equity market, to the extent that the rise reflects brightening of the economic outlook rather than inflationary pressure. We remain cyclically bullish on equities, but near-term caution is warranted. The modest pullback has been insufficient to unwind technical conditions. The two main catalysts for a correction are early tapering and weak growth around the world. The U.S. economy is steadily expanding, Japan continues to fight inflation, Europe remains in recession and China is experiencing softer growth than usual. A grinding government bond bear market is finally underway and should help trigger an eventual change in equity leadership. As Treasuries sell-off, safe haven and higher-yielding investments may lose appeal. We believe investors may begin looking for economic-sensitive risk assets with solid underlying fundamentals. We prefer stocks focused on business spending, including technology and capital goods producers.

1 Source: Morningstar Direct, as of 6/14/13. 2 Source: Business Insider, “There’s One Chart Responsible For The Tectonic Shift In Global Markets,” June 12, 2013, http://www.businessinsider.com/us-real-rates-rise-central-to-world-markets-2013-6 3 Source: U.S. Census Bureau, “Advance Monthly Sales for Retail and Food Services, May 2013,” June 13, 2013, http://www.census.gov/retail/.

4 Source: Bureau of Labor Statistics, “Consumer Price Index – April 2013,” May 16, 2013, http://www.bls.gov/news.release/cpi.nr0.htm. 5 Source: Reuters, “U.S. household wealth increases by $3 trillion in first quarter,” June 6, 2013, http://www.reuters.com/article/2013/06/06/usa-economy-debt-idUSW1N0DP00J20130606. 6 Source: cnbc.com, “S&P Revises US Credit Outlook to ‘Stable’ From ‘Negative’,” June 10, 2013, http://www.cnbc.com/id/100791461.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

GPE-BDCOMM2-0613P

© Nuveen Asset Management