You ever watch Night of the Living Dead,I Am Legend, or any of the other fictional accounts of the breakdown of civilization? Personally, I never watch horror movies or anything that has evil at its core. The last scary movie I watched was The Fly when I was 7 years old. It gave me nightmares for weeks on end, and I swore off horror films. However, I have lately been exposed to zombies, thanks to my youngest son (now 17), who can drive me nuts with his Xbox killing of zombies for endless hours while his English paper due tomorrow must wait.

Our undead-obsessed culture has embraced zombification in a big way, with action games (Resident Evil, House of the Dead), novels (The Zombie Survival Guide), television (The Walking Dead), action movies (World War Z), and the newest phenomenon, Zombie Walks. In October 2010, 4,000 undead creatures participated in the New Jersey Zombie Walk, lurching mindlessly through the streets. You might think of a Zombie Walk as a Flash Mob in slow motion. Zombies (in case you haven't been exposed) are corpses raised from the dead who relish human flesh. Their dietary preference eventually leads to Zombie Apocalypse, whereby the ruling elite of the world – the (savory) fat cats – are all consumed, and the world is completely taken over by the undead (who then presumably go hungry).

The enthusiasm of our culture for Zombies is estimated to contribute a tidy $5 billion dollar a year to GDP, and that doesn’t even include the too-big-to-die zombie banks. In my opinion, the acute interest in zombies and horror (and escapism in general) says something about our country’s mental health.

It may say something about our economic health as well. In a world where 99% feel disempowered, the average American’s financial net worth has declined nearly 40% in the wake of the economic crisis of 2008-09; real wages have been declining for 30 years; and our government is now breaking a generational promise to the Baby Boomers, the Gen X’s, and the Gen Y’s with regard to retirement and health care. So is it any wonder that playing dead or watching a movie in which the 1% is served up for lunch is entertaining to the vast majority of Americans, who can’t get ahead?

And now our investment markets, too, are starting to zombify, as the number of believers flocking to the Bernanke Church of QE to Infinity swells and we experience a disconnect between unreal stock market performance and the underlying numbers that tell of anemic GDP growth, continued high unemployment, ongoing troubles in the Eurozone, and the onset of the Bank of Japan’s most reckless monetary experiment ever.

Grant Williams, author of the inimitable newsletter Things That Make You Go Hmmm…, made a presentation called “Do the Math” to the CFA conference in Singapore on May 21, 2013. His presentation can be seen by clickinghere, and it is worth 48 minutes of your time to watch. Grant’s proposition is that QE policies on a global scale have created an artificial environment of inflated stock prices, particularly in the US, which is viewed as the safest of markets. As in the game of musical chairs, all investors playing the QE momentum game think they are smart enough to anticipate Bernanke & Company’s actions regarding tapering of QE and to hurriedly exit stage left before the decline in stock prices sets in. Really? Let me remind you of the confidence everyone had in 2007 regarding real estate:

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We are still dancing.”

– Chuck Prince, former CEO of Citi Group, describing the bank’s mortgage lending and CDO practices in July of 2007. Oooooh, I feel David Bowie's “Let’s Dance” start humming in my head as I watch investors do the Global QE Shuffle.

Ride ‘Em Cowboy

Central bank practices and continued QE stimulus have disconnected equity asset prices from their historical perspectives and valuations. Ever since the establishment of bailouts and QE policies, the equity markets have responded positively to the Keynesian cocaine stimuli of the Fed, Bank of England, Bank of Japan, and ECB, with a jolt upward of more than 100%, as shown in the following graph.

At the beginning of each quarter, we develop a series of forecasted returns. After the number crunching that is our discipline, Troy and I always look at each other and ask, “Are you ready to bet against a man who owns a money-printing press in his basement?” Given an 89% positive correlation to rising stock prices when the Fed is printing, we always answer "No."

- First Non-QE Period – March 31, 2010, to August 27, 2010 (down -8.97%)

- QE 2 – August 27, 2010, to June 30, 2011 (up 22.81%)

- Second Non-QE Period – June 30, 2011, to August 26, 2011 (down -9.99%)

- Operation Twist – August 26, 2011, to April 4, 2012 (up 18.88%)

- Hilsenrath Says QE to End with Twist’s End – April 4, 2012, to June 6, 2012 (down -5.99%)

- Hilsenrath Backtracks on QE’s End – June 6, 2012, to August 17, 2012 (up 7.83%)

- QE 3 – August 17, 2012, to November 29, 2012 (down -0.16%)

- QE 3 Expanded - November 29, 2012, to May 22, 2013 (up 16.91%)

- Bernanke introduces TaperMania – May 22, 2013, to June 12, 2013 (down -2.59% and counting)

Taper, Taper, Taper – To Taper or Not to Taper, That Is the Question.

As asset managers we understand the artificial nature of current market prices and the fickleness of traders as the Fed debates whether and when to taper. Since Bernanke’s speech on May 22nd introduced the possibility that the Fed could decide to reduce QE over the next two FOMC meetings, the Dow Jones Industrial Average has experienced 100-point swings in 7 of the last 10 trading sessions. From Bob Pisani’s Twitter feed for June 12th: “Volatility is up since Bernanke’s May 22 testimony. DOW’s average daily trading range from Jan. 2 - May 21: 109 points; since May 22: 184 points.”

I borrow the following from Chris Low at FTN Financial:

There are three problems with tapering:

- Bernanke does not like “tapering” because tapering implies reduction only. The Fed is still considering changes to the program which could involve decreasing or increasing the size of purchases, or a change in the mix of mortgages and Treasuries. The Fed also reserves the right to reverse course midstream. In other words, they continue to insist they might upsize QE.

- Also, tapering implies a steady progression, with reductions in purchases in even increments until it is finished. The Fed believes predictable schedules are disruptive. Bernanke has repeatedly said the Fed wants to move away from predictable schedules of policy changes to avoid this disruption.

- The Fed may change its plans if it thinks the market has gotten ahead of itself and the Fed WILL change its plans if economic conditions support a change. That might mean inflation remaining as low as it is now, especially if inflation expectations drop further. Or, it might mean a change in policy if home sales show or employment stall.

The Fed has assumed a dual mandate of reducing unemployment and stimulating GDP growth that is, in our opinion, impossible. Why impossible? The problems that exist in our economy are structural and cannot be solved by the continued printing of money. From our friend Dr. Jason Hsu at Research Affiliates:

The ability to print money gives the government an ex post option to renegotiate (write down) its debt in real terms. If the government spending and/or investments prove wasteful or unwise, it can allocate the pain to bondholders by printing more money instead of facing the wrath of the electorate by raising taxes in a slumping economy. This option to renegotiate debt without legislative procedure enables irresponsible spending by the government, perpetually, or at least until rampant inflation ensues…. The government’s willingness to borrow rather than tax is a statement about its ability to allocate pain. Higher taxation today allocates pain to wage earners now. Borrowing is a tax on future wage earners.

The continued monetization of debt by the printing of more and more money allows our leaders (if there are any) in Washington, DC, to postpone legislation that would promote growth in our country. We have a fiscal problem of deficit spending, with a President and Congress who refuse to address the issues related to reducing government outlays. Their recalcitrance has been aided and abetted by the Federal Reserve’s willingness to simply keep printing more money.

Structural issues that need to be addressed before our economy will grow again are fourfold:

- meaningful tax reform, both corporate and individual

- immigration reform to create a broader and more robust demographic that will contribute both to the labor pool and to domestic consumption

- reform of the regulatory environment that is choking businesses’ willingness to invest in capital projects (We must admit that Dodd-Frank did nothing to correct the problem of too-big-to-die zombie banks, and we must revise its complicated provisions and regain the ability to write the rules as we go.)

- repeal of Obamacare, which will otherwise unleash a landslide of destructive unintended consequences.

If you think Obamacare is not affecting employment, then consider the following. Employers with more than 50 full-time employees will be subject to the employer mandate in the Affordable Care Act, whereby they will either pay for health insurance for their employees or pay a fine beginning in 2014. Rather than opting to grow by hiring, small businesses are seeking ways to reduce their full-time employee count, and thus we now have the term job splitting. Although unemployment is declining due to the hiring of more part-time workers, wages are declining in the aggregate. The reduction of wages translates to weaker consumption.

This is but one example of a structural problem that cannot be cured by Federal Reserve monetary policy. Consider one of our clients, who employs over 300 full-time workers and currently provides them with what Obamacare terms a “Cadillac insurance plan,” which will be penalized under the Affordable Care Act. Rather than continue their plan, the company will terminate health insurance for its employees at the end of this year and simply pay the per-person Affordable Care Act penalty.

I see nothing in the Affordable Care Act that addresses the runaway government spending associated with Medicare and Medicaid. However, these structural issues can be fixed. Our country still has choices – we are not yet in Europe's or Japan’s shoes – but the solutions will require federal government leadership. And this is the real problem our economy has: in a time when we critically need leadership, we have a President and Congress content to do nothing as long as the Fed keeps the stock market moving up. NY Times columnist Maureen Dowd, in her column dated April 21, 2013, sizes up this failure of leadership:

President Obama has watched the blood-dimmed tide drowning the ceremony of innocence, as Yeats wrote, and he has learned how to emotionally connect with Americans in searing moments, as he did from the White House late Friday night after the second bombing suspect was apprehended in Boston.

Unfortunately, he still has not learned how to govern.

How is it that the president won the argument on gun safety with the public and lost the vote in the Senate? It’s because he doesn’t know how to work the system. And it’s clear now that he doesn’t want to learn, or to even hire some clever people who can tell him how to do it or do it for him.

It’s unbelievable that with 90 percent of Americans on his side, he could get only 54 votes in the Senate. It was a glaring example of his weakness in using leverage to get what he wants.

(my underlining)

This editorial is from one of the more liberal supporters of President Obama! The message here is that there will be zero structural changes until 2015 or later, depending on election results in 2014. Without structural reform, the only game in town is to buy time and prevent short-term catastrophe, which is the main purpose of the Ben Bernanke printing press. And remember, political time is very different from market time. Politicians know what the problems are, and they know the solutions; they just can’t figure out how to get re-elected when they do the right thing.

A democracy cannot exist as a permanent form of government. It can only exist until the voters discover they can vote themselves largesse from the public treasury. From that moment on, the majority always votes for the candidates promising them the most benefits from the public treasury, with the result that a democracy always collapses over a loss of fiscal responsibility, always followed by a dictatorship. The average of the world's great civilizations before they decline has been 200 years. These nations have progressed in this sequence: From bondage to spiritual faith; from spiritual faith to great courage; from courage to liberty; from liberty to abundance; from abundance to selfishness; from selfishness to complacency; from complacency to apathy; from apathy to dependency; from dependency back again to bondage.

– commonly but not verifiably attributed to Alexander Tytler, 1776

Therefore our conclusion is that Bernanke & Company will not begin tapering anytime soon, as nothing has changed with regard to unemployment or GDP growth or our legislative process in the last five months. Congress and the President will do nothing, in part because the Fed facilitates the fiscal irresponsibility. We see a continuation of anemic growth at the 1-2% level without any significant gain in employment. Furthermore, we opine that Helicopter Ben will ride the printing press until he retires as Fed chairman in January of 2014 – effectively kicking the can and handing off the issues of inflated monetary stimulus to the next Fed chairman. The end result of the glut of fiat currencies dumped on the world by the global central bank fraternity will be inflation; and it's not a question of if, but when. As my friend John Mauldin says, the US will come to its own Bang! moment of the End Game, but at a later date, and after Japan does.

Abenomics (Yen) versus Draghism (Euro): Currency War

We are living today in a three-speed world:

- “Pedal to the metal” economies – emerging economies and frontier economies

- “Stuck in park” economies – the US and other select advanced economies

- “Looking in the rear view mirror and backing up” economies – Japan, France, Italy, Greece, Ireland

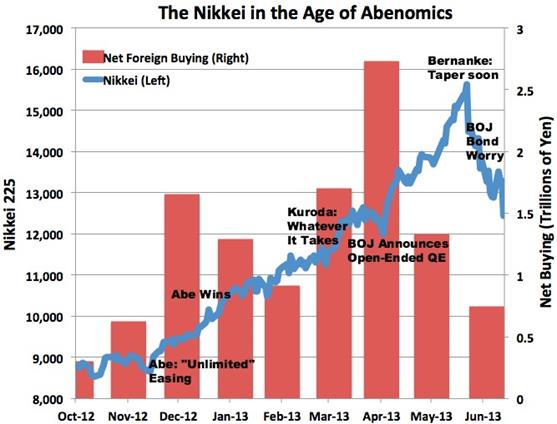

In my commentary this past March, I presented the case that Europe was our biggest risk factor for investing in 2013. Although I still think there are large European risk factors, I don't want to underestimate the market earthquakes Prime Minister Abe is setting off in Japan. In January, the Japanese adopted Abe’s plan for huge monetary easing and government spending as the fuel with which to attain escape velocity from 20 years of zero growth and errant government policies. The sheer size of the monetary stimulus is astounding: three times the monetization efforts of our Federal Reserve, in relative terms. When Abe's program was launched in November 2012, the Japanese markets responded with an 80% appreciation in six months and a 4.1% growth rate for the first quarter of 2013. But now the doubts are creeping in as to whether doubling Japan's debt level in an effort to significantly devalue the yen versus other currencies will pay off – or backfire in a big way.

As John Mauldin and Kyle Bass have so adeptly reasoned, Japan is a bug destined for a windshield. The country has an aging population and almost no net immigration, natural resources supply-chain issues, twenty-plus years of zero growth coupled with misguided government spending that has resulted in a debt-to-GDP level of 285% (the US is at 90%), and a government that must now resort to desperate measures to try to restore growth and fiscal balance.

Japan has an export economy, and the only way for it to grow is to take market share from Germany, China, Korea, Taiwan, and other countries. Abe’s goal, in my opinion, is to gain market share, not through innovation and superior products, but the old-fashioned way: by means of a currency war. Let's make the price of a Lexus in the US the same as the price of a Hyundai, he reasons. But does Japan really think the Germans, Chinese, and Koreans will sit idly by and allow the unilateral devaluation of the yen?

And bear in mind, this is the first time a currency war would occur in which all the currencies involved are fiat currencies – no one has any hard-asset-backed money: it's all paper.

Abe’s second objective is to create inflation of 3% in Japan, as he desperately needs to inflate away the massive amounts of government debt. Where will his policies finally take him? No one knows, including him: we have never been here before, and anyone who attempts to depict precisely how and when the End Game will play out is simply guessing. However, at Excelsia we have made a strategic decision to maintain gold and hard-asset mining companies as a part of our portfolio. We are probably early, and we all know what early means in the investment business: you’re wrong in the short term. But the massive amounts of new money the fraternity of central bankers is pumping into the global financial system will have consequences, intended and unintended. Our best guess is that one of the consequences will be inflation – perhaps not the hyperinflation we have written about in the past, but inflation nonetheless.

Gold and Gold Stocks

Contrarian: a person who takes acontraryposition or attitude; specifically an investor who buys shares of stock when most others are selling and sells when others are buying. (Merriam-Webster Online)

Between April 12 and April 15 of 2013, gold declined 14.9% in two days. In terms of statistical probability, this represented a 3-standard-deviation move from its mean average. Bloomberg News reported on April 16th that rather than panic, the world’s most avid consumers of gold, the citizens of India, flocked to the jewelry and coins shops in a buying frenzy. As we evaluated the carnage and looked at mining stocks down over 40% since November and the price of gold down 20%, we were reminded of health-care stocks in 2010. Recall that the passage of Obamacare that year resulted in Johnson & Johnson, Merck, Pfizer, Eli Lilly, and other health-care stocks sinking to new lows in July, 2010. Nationalized health care was here; government price controls were going to make big pharma unprofitable; and all of health care was shunned. During that year we began to buy those companies for one reason: value! They paid 4-5% dividends, were still growing (if not by double digits), and their balance sheets were strong. When gold stocks sold off at an unprecedented pace, we had the same thought again: value! The chart below depicts what we think of as value:

|

2013 EPS Est. |

2014 EPS Est. |

2013 P/E |

2014 P/E |

Indicated Dividend |

Yield |

2013 Payout Ratio |

|

|

BHP |

4.31 |

5.19 |

14.6 |

12.1 |

2.28 |

3.63 |

53% |

|

RIO |

5.63 |

6.16 |

7.7 |

7.0 |

1.83 |

4.23 |

33% |

|

FCX |

3.43 |

4.01 |

8.6 |

7.4 |

1.25 |

4.23 |

36% |

|

NEM |

2.68 |

3.33 |

12.4 |

9.9 |

1.40 |

4.23 |

52% |

|

ABX |

3.07 |

3.24 |

6.4 |

6.0 |

0.80 |

4.10 |

26% |

|

Source: S&P |

|||||||

How Do You Invest?

US Trust conducted a survey at the beginning of this year, questioning how the wealthiest 1% in this country, who own 40% of an estimated $54 trillion of the nation's total wealth, were investing in today’s market. Everyone in the survey was worth a minimum of $3 million, and one third of the respondents had $10 million or more. The survey showed that:

… 88 percent of respondents feel financially secure today and 70 percent feel confident about their financial security in the future.… However – and this is where the dual personality comes in – the wealthy are still holding mountains of cash. The survey found that 56 percent have a “substantial” amount of cash. Only 16 percent of them plan to invest that cash in the next couple of months. And only 40 percent plan to invest it over the next two years.

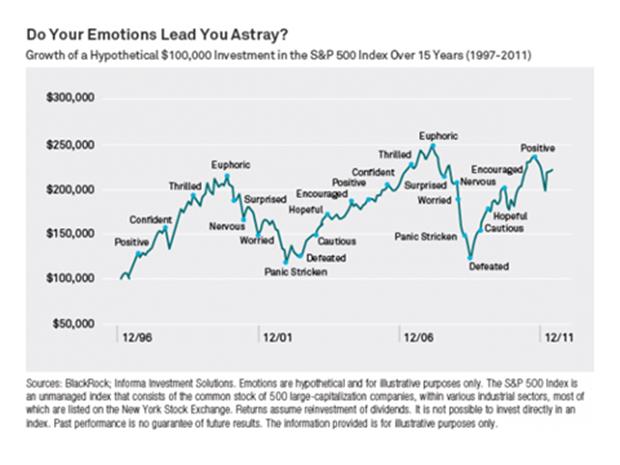

In my opinion, most individual investors have not participated in the market appreciation that has occurred since March, 2009. The market has been driven by institutions, high-frequency traders, and hedge funds. Most individual investors lack investment discipline and are led more by their emotions than by careful analysis.

Unbelievable

From the Wall Street Journal of May 24, 2013:

All trades in American Electric Power Inc (AEP.N) andNextEra Energy Inc(NEE.N) in a crash that happened in the first minute of trading on Thursday will stand, the New York Stock Exchange said, following the latest in a flurry of unexplained sharp drops in the market.

The stockseach dropped more than 50 percent in the first minute of trading, though they ended just down slightly. Individual stock moves of 10 percent or more in a five-minute period usually trigger a trading halt, based on SEC rules, but the rules do not apply to the first 15 minutes of trading or the last 30 minutes of a session. The exchanges are able to cancel trades in the event of irregular or erroneous activity.

(my underlining)

On May 6, 2010, the stock market experienced what has come to be know as a “flash crash,” in which the Dow plunged 1,010 points, only to recover in a matter of minutes. To date, no one knows what happened. On Thursday, May 23, the market experienced a similar occurrence that involved two utility stocks, AEP and NEE. The key diffference between the two events proved to be a stunner: the exchange nullified trades that occurred in the flash crash but let stand the trades of AEP and NEE. What this means is that an investor who had a stop loss and sold his shares in the opening at $20, only to have the stock recover to $42, was abused. And the NYSE honored the trades as good trades. Unbelievable! Do you think the high-frequency traders are smart enough to exploit such a market? Furthermore, the NYSE said they will be marked with an “aberrant report indicator”. While those trades are still valid, NYSE said they “will be excluded from the high and low data” disseminated by the Consolidated Tape Association, which oversees the dissemination of real-time trade and quote information in NYSE-listed securities. FactSet data shows that hundreds of trades in both stocks were priced below those prices (the LOW of the day).

So the bottom line is the plunge in these shares were wiped off the tape, but NOT from investors’ portfolios. In fact, if you pull up an historical chart on both tickers, it never happened!A solution to prevent this kind of abuse is for the exchanges and the SEC to restore the “uptick rule.”

And you thought utility stocks were for grandmas, widows, and orphans.

Good Luck Out There!

Cliff

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Excelsia, Inc.), or any non-investment-related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Excelsia, Inc. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Excelsia, Inc. is neither a law firm nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Excelsia, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.

© Excelsia Investment Advisors