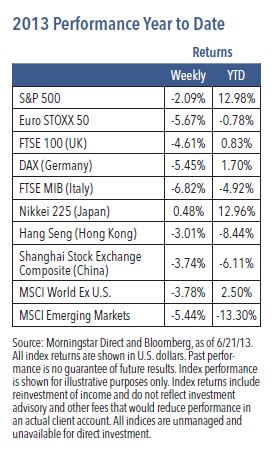

U.S. equities declined last week as the S&P 500 ended down 2.09%.1 The S&P suffered the first back-to-back one-day declines of more than 1% since last November. Global equities and bonds were also hit hard, with large sell-offs in emerging market assets, commodities and commodity currencies. Concerns about the fallout from dampened Fed policy accommodation are driving the weakness.

The Clock is Ticking

At the FOMC meeting, the policy language did not change. However, the FOMC made an important change to the outlook, noting that downside risks have diminished since last fall. The Fed is not in any immediate hurry to begin reducing the size of its monthly asset purchases, but it has begun to lay the groundwork. Fed Chairman Ben Bernanke stated if economic conditions improve as expected, it would be appropriate to begin reducing the Fed’s monthly purchases later this year and have them completed by mid-2014, when the unemployment rate is expected to be close to 7%. The Fed’s new forecast suggests that the first rate hike could come earlier in 2015 than previously thought. Rising U.S. Treasury yields do not appear to make sense in light of low inflation and the lack of acceleration in job growth. The Fed is either trying to discipline the market from over-reliance on the “Bernanke put,” or as we believe may be the case, it is ratifying the global backup in government yields that has been driven by the reduction of systemic threats.

In our opinion, a decrease in the Fed’s quantitative easing is not an economic hurdle. A diminished QE3 program should be expected, given slower growth of the federal budget deficit and the decrease in issuance of Treasury debt. The spike in U.S. Treasury yields has caused huge ripples across interest-rate sensitive investments. Investors are now rotating aggressively out of bonds and bond-like investments into cash, rather than moving along the risk spectrum to equities. Many have focused on the end of the great monetary experiment rather than the Fed’s message about its policy being data dependent. Potential outcomes may be either: 1) the economy will stabilize and allow investors to gain confidence in corporate earnings, or 2) soft and choppy data will persist, and QE will be extended. While growth will remain subdued by historical standards, the recovery should solidify and broaden as we wait for private sector deleveraging pressures to gradually abate in the U.S. and developed markets, the drag from fiscal austerity to wane, and monetary and credit conditions to gradually improve. We would expect that even a moderate upturn in growth should translate into better corporate earnings.

The Big Picture

We remain bullish over a cyclical horizon. However, following this year’s impressive rally, current conditions leave us cautious in the near term. The equity market has benefitted from decent economic growth, moderating tail risk, depressed interest rates and low bond volatility. The bond sell-off may have moved ahead of itself in the short term, but an inflection point in the Fed’s loose monetary policy is drawing closer. Corrective forces remain the dominant market theme. A consolidation is necessary to absorb the sharp valuation expansion, especially within the context of the nascent adjustment in the U.S. Treasury market and the unwinding of carry trades associated with previous weakness in the Japanese yen and Japan’s QE program. Treasury yields did not decline with the softer equity market, and this resilience reinforces expectations for a Fed policy shift. It appears equity weakness is a reflection of position pairing rather than a darkening in the economic and profit outlook.

We maintain our positive views on equities cyclically, as bond yields remain well below nominal GDP growth, and profit growth should continue to be moderately positive. We expect overvalued, defensive sectors and bond proxies to bear the brunt of the position squaring. Conversely, we believe cyclical sectors are under- valued and earnings expectations are acceptable. We conclude with a few positive thoughts: a dovish Fed and the federal funds rate essentially at zero, an astonishing decline in the federal budget deficit, no signs of inflation, the U.S. heading toward energy independence, an American manufacturing renaissance and strong corporate balance sheets.

1 Source: Morningstar Direct, as of 6/21/13.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock

Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

GPE-BDCOMM3-0613P

© Nuveen Asset Management