Sell Off Continues

Equity markets sold off for the fourth time in the past five weeks, after experiencing only four negative weeks through the first four months of the year. Losses were concentrated on a Thursday in which almost every asset class sold off. Equity markets lost approximately 2.5% on the day alone. For the week, the S&P 500 and Dow Jones Industrial Average lost 2.1% and 1.8%, respectively. The Barclays Aggregate Bond Index shed 1.8% - the seventh negative week in the past eight.

Markets reacted unfavorably to the regularly scheduled Federal Open Market Committee (FOMC) meeting that ended Wednesday. Although Fed policy was unchanged, Chairman Ben Bernanke noted that the

committee would look to ease its level of asset purchases later this year and into 2014 assuming economic data continued to improve. He noted that “the unemployment rate would likely be in the vicinity of seven percent” at the point when asset purchases come to an end. Interest rates are expected to be held near zero for the foreseeable future.

Generally, the FOMC’s economic assessment was unchanged, although they noted softer inflation readings in recent weeks. FOMC member James Bullard actually dissented from the committee’s policy decision (joining Esther George), but not due to a hawkish stance. Given falling inflation levels, Bullard believes the Fed should actually be more aggressive in supporting asset price levels.

The Fed’s exit plan will likely dominate market sentiment in the weeks and months ahead. Interest rates are backing up significantly since Bernanke’s comments: the 10-year reached 2.52% by week end, up from 2.14% the previous Friday.

Amid the noise surrounding the FOMC, a few important economic data points were released last week.

Supporting Mr. Bullard’s concerns was the consumer price index, released on Tuesday, which indicated inflation remains tamed. The headline rate increased 0.1% in May, and 1.4% year-over-year. From a core perspective, which strips out the impacts of volatile food and energy components, inflation increased 0.2% during the month and 1.7% year-over-year.

On Tuesday, the Census released May housing start data, which rose 6.8% from April to reach a seasonally adjusted annual rate of 914,000. This was below expectations for a 955,000 reading, however, as single-family home construction rose just 0.3%. The more volatile multi-family component increased by 21.6% in the month.

Permits slowed modestly from a very strong rate in April, with a pace of 974,000 issued in the May. Strength in this measure provides reassurance that new home building should remain robust through the summer months.

In other housing news, existing home sales ramped up to a rate of 5.18 million in May. Prices continued to firm, increasing 8.4% during the month and 15.4% over the prior 12 months. The share of distressed sales was unchanged from April, at 18%. According to the National Association of Realtors, this is the lowest percentage rate observed since they began tracking data in October 2008.

In aggregate, last week’s housing data indicates that sector of the US economy continues to be a source of strength. Pick-ups in sales, prices, and construction levels illustrate a housing market on the mend.

Given the importance of housing to growth and labor markets, investors should continue to be encouraged by these trends.

Is Fixed Income The New Equity?

After several decades of positive returns, fixed income investors are being treated to a rude awakening in the last six weeks. Recent comments from Federal Reserve officials suggest a sooner than anticipated exit from quantitative easing, raising the prospect of higher interest rates. Throughout the universe of fixed income assets, investors are questioning the future return potential, leading many to wonder, what now?

Most surprising to investors was the speed and severity of the move in Treasury markets, where yields on the 10-year went from 1.6% to more than 2.5%.

10-Year Treasury:

Source: Wall Street Journal

That translated into unexpected losses across the fixed income spectrum, including corporate bonds, mortgage-backed securities, municipal bonds, and emerging market debt.

Source: SoberLook

Exchange-traded funds (ETFs) are being hit even harder. The iShares iBoxx $ High Yield Bond ETF (ticker: HYG) is down 5.4% in the 30 days through June 21. That is relative to a 3.7% decline in the BofA/ML HY Master II Index. According to Dave Lutz, Head of ETF Trading and Strategy at Stifel, Nicolaus & Co. “high yield (products) recorded their biggest outflows on record last week…one third of that was straight from ETFs.”

Source: Business Insider

Volatility is also seeping into interest rate sensitive equity sectors. Utilities are down 8.2% and the Dow Jones US Select REIT Index is off nearly 14%.

In previous periods since 2008, when equity markets were selling off, investors could rely on fixed income for a modicum of stability. Lately, that relationship is changing. Correlations between treasuries and the S&P 500 moved into positive territory for the first time since late 2010.

Source: Business Insider

The one group benefitting during this episode is banks. Banks hold the ability to borrow at short-term rates that are still near zero, and lend at the now rising longer-term rate. Since mid-April, banks are outperforming the S&P 500 Index by 6.0%, based on analysis from the blog SoberLook.

Source: SoberLook

The question now is where we go next. The possibility certainly exists that interest rates push even higher in the months ahead, but that reality is unlikely just yet. That is due in large part because the Fed will react if it sees economic deterioration occurring due to higher interest costs.

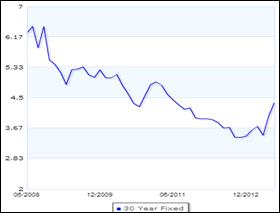

Higher rates are already beginning to bleed into some segments of the economy. The Wall Street Journal reports the average rate on a 30-year mortgage is now 4.4%, compared to 3.4% in early May.

Source: Wall Street Journal

Over the short-term, fixed income assets are likely to be pressured by the inevitable end of quantitative easing and the subsequent rise in interest rates. It is important to remember that rising rates are not entirely bad for fixed income assets, though. Investors are able to collect yield, partially offsetting price depreciation, and eventually coupon and principal payments are reinvested into higher yielding assets.

From mid-1941 through late 1981, as interest rates moved successively higher, intermediate-term government bonds generated a 3.3% annualized return. That is decidedly lower than the post-1981 secularly declining rate environment, but not as disastrous as investors might be led to believe.

Regardless of where rates go from here, the path will not be exact. The Bank for International Settlements issued a new report and in it addressed the exit policies for global central banks. They concluded, “central banks are mindful of the fact that the size and scope of the exit will be unprecedented. This magnifies the uncertainties involved and the risk that it will not be smooth.” As central banks grapple with the appropriate exit path, investors need to be mindful of the potential for much higher forward-looking volatility in fixed income assets.

The Week Ahead

This week contains an array of important economic data for investors to digest.

On the housing front, new home sales and the Case-Shiller Home Price Index are released on Tuesday. Additionally, durable goods and personal spending data are on tap for Tuesday and Thursday, respectively.

Investors will also look to the final estimate of first quarter GDP on Wednesday. Economists do not anticipate any change from the 2.4% print from late May.

On Thursday and Friday, European leaders meet for an EU summit. The implementation of their banking union and other reforms will be discussed at the meeting.

Central banks meeting this week include Israel, Hungary, Taiwan, Czech Republic, and Colombia. Economists expect Hungary to cut rates by 25 bps.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent